Размер видео: 1280 X 720853 X 480640 X 360

Показать панель управления

Автовоспроизведение

Автоповтор

Very helpful, thanks!

how would you apply this for loans? for example mortgage or personal loans?

what empirical distribution is used in KMV? Gamma or Poison?

I have an Excel sheet of Merton model but I don't know the input data i am supposed to use. Can anyone please help me

3155 Padberg Street

Thanks! Great video!

Thank you ! :)

4683 Yost Pines

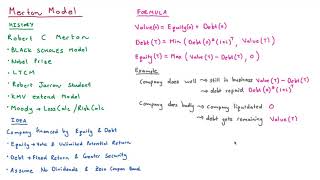

What does KMV stand for?

KMV is the abbreviation for Kealhofer, McQuown and Vasicek, who were the founders of the KMV company (that was later acquired by Moody's). You can read more about the history of KMV here: www.moodysanalytics.com/about-us/history/kmv-history

Very helpful, thanks!

how would you apply this for loans? for example mortgage or personal loans?

what empirical distribution is used in KMV? Gamma or Poison?

I have an Excel sheet of Merton model but I don't know the input data i am supposed to use. Can anyone please help me

3155 Padberg Street

Thanks! Great video!

Thank you ! :)

4683 Yost Pines

What does KMV stand for?

KMV is the abbreviation for Kealhofer, McQuown and Vasicek, who were the founders of the KMV company (that was later acquired by Moody's). You can read more about the history of KMV here: www.moodysanalytics.com/about-us/history/kmv-history