You can find the spreadsheets for this video and some additional materials here: drive.google.com/drive/folders/1sP40IW0p0w5IETCgo464uhDFfdyR6rh7 Please consider supporting NEDL on Patreon: www.patreon.com/NEDLeducation

Hey! I have several questions/comments. Firstly, while the iterative procedure seems generally correct, we are using Merton's model in the end, which is not KMV's, as KMV's uses an empirical formula for the probability of default based on historical data (so it is more of an intensity model than a structural model). It is true that it is inspired in Merton's structural model, so it may be similar and for teaching purposes this is a accurate enough. Secondly, the DPT horizon is never used in your example, instead, we use the DPT extracted from the liabilities from 2021 and 2022. Why did compute it in the first place? Where should it be used? Speaking of fundamentals, the firm itself declares its assets to be around 3.5, while the market cap is around 14. Thus, estimating the value of assets departing from the market cap value seems to me a systematic overvaluation, as usually we have from 3x to 30x depending on the sector: market valuation is usually way higher than the liquid assets that can be used to pay debt. I would agree to make an average rescaling of the values to the assets declared by the company fundamentals, and then use the ''solver" to adjust the asset volatility. Or maybe this company in particular was underpriced compared to its assets, but then, why the assets declared in the fundamentals are so small compared to our estimation of the assets of the company? Thanks for your time! The video was helpful!

Hi, I believe that simplifying the value of assets as equal to the market cap during the iteration process may introduce distortions, especially for companies where the total asset value isn’t fully reflected in the market cap

Excellent video and great explanation of KMV model. However, I have one question - Why their is such material difference between Book value of asset at 2022 (3.49) and Market Value of asset at 2022 (9.52). Could this be explained by any theory?

Thank you for the video, to capture uncertainty (which makes options more valuable) how about if we use the VIX index? Would this be valuable and important to add it to your calculation in this video? Or Newton-iterative procedure is enough?

Hi, I found your video really helpful, thank you! I tried doing the same method by myself and encountered a weird issue. My mispricing calculated for daily market cap values was the exact same for all days in the sample. Is there any reason why this should happen?

You can find the spreadsheets for this video and some additional materials here: drive.google.com/drive/folders/1sP40IW0p0w5IETCgo464uhDFfdyR6rh7

Please consider supporting NEDL on Patreon: www.patreon.com/NEDLeducation

Hey! I have several questions/comments. Firstly, while the iterative procedure seems generally correct, we are using Merton's model in the end, which is not KMV's, as KMV's uses an empirical formula for the probability of default based on historical data (so it is more of an intensity model than a structural model). It is true that it is inspired in Merton's structural model, so it may be similar and for teaching purposes this is a accurate enough.

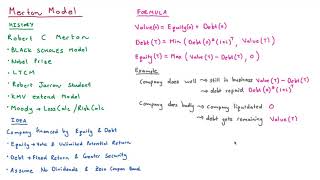

Secondly, the DPT horizon is never used in your example, instead, we use the DPT extracted from the liabilities from 2021 and 2022. Why did compute it in the first place? Where should it be used?

Speaking of fundamentals, the firm itself declares its assets to be around 3.5, while the market cap is around 14. Thus, estimating the value of assets departing from the market cap value seems to me a systematic overvaluation, as usually we have from 3x to 30x depending on the sector: market valuation is usually way higher than the liquid assets that can be used to pay debt. I would agree to make an average rescaling of the values to the assets declared by the company fundamentals, and then use the ''solver" to adjust the asset volatility. Or maybe this company in particular was underpriced compared to its assets, but then, why the assets declared in the fundamentals are so small compared to our estimation of the assets of the company?

Thanks for your time! The video was helpful!

Hi, I believe that simplifying the value of assets as equal to the market cap during the iteration process may introduce distortions, especially for companies where the total asset value isn’t fully reflected in the market cap

Where did you get the formulas from? Did you use any special paper?

Should we use KMV method to make a shadow rating? I mean make a rating results like Fitch, Moody's or S&P rating agency??

Your Teaching in Awsome. Excel is best platform forum for teaching of complex calcuation

Hello, sir. Can you tell how to get data for the model, say for example: SVB bank

Excellent video and great explanation of KMV model. However, I have one question - Why their is such material difference between Book value of asset at 2022 (3.49) and Market Value of asset at 2022 (9.52). Could this be explained by any theory?

Is there a way to do this when a company is not listed on the stock exchange?

Thank you for the video, to capture uncertainty (which makes options more valuable) how about if we use the VIX index? Would this be valuable and important to add it to your calculation in this video? Or Newton-iterative procedure is enough?

Kindly explain where did you get shares?

can you please explain what your doing with the solver by "fitting"

I am interesting to know what will be the corresponding approach / model on private companies that do not have available share prices

Hi Vasilis, and thanks for the question! This paper provides a good overview: www.econstor.eu/bitstream/10419/249533/1/WPS-32.pdf.

@@NEDLeducation Legend thanks

Hi, I found your video really helpful, thank you! I tried doing the same method by myself and encountered a weird issue. My mispricing calculated for daily market cap values was the exact same for all days in the sample. Is there any reason why this should happen?

Dear Sir, Can I use your spreadsheet to teach in the class

Thank you!

phenomenal... very appreciated it

Totally missed the opportunity for title - "Applying KMV to GameStop (GME)"

16918 Harvey Glens