Размер видео: 1280 X 720853 X 480640 X 360

Показать панель управления

Автовоспроизведение

Автоповтор

Thank you useful for FRM Part 2

I love your videos.

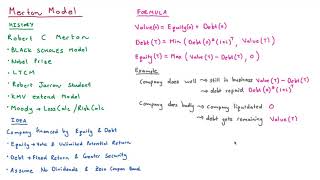

Great videos. Two small things. You forgot the negative sign while discounting strike in option pricing equity formula. Also in calculating d1 it’s mean - sigma^2/2. You mistakenly added them

Can someone please explain when to calculate the drift rate? Why is that not used to calculate probability of default?

in 36:52 the shares should be 323.6 cr sir, please tell why we took 3236 cr ? are we considering shares outstanding or paid up share capital?

sir at 30:53 you missed subtracting 1 while calculating returns.

Sir please compute default probability by method used by vassolu and xing 2004 and lofr and posch

Thank you useful for FRM Part 2

I love your videos.

Great videos. Two small things.

You forgot the negative sign while discounting strike in option pricing equity formula. Also in calculating d1 it’s mean - sigma^2/2. You mistakenly added them

Can someone please explain when to calculate the drift rate? Why is that not used to calculate probability of default?

in 36:52 the shares should be 323.6 cr sir, please tell why we took 3236 cr ? are we considering shares outstanding or paid up share capital?

sir at 30:53 you missed subtracting 1 while calculating returns.

Sir please compute default probability by method used by vassolu and xing 2004 and lofr and posch