Brother can you make a video on derivation of ARMA model, difference equation in time Series Econometrics derivation and it's solutions and numericals also,Ardl Bound test derivation and differential equation in time Series Econometrics derivation.

So this equality is only valid outside of the framework of the classical lineal regression model, where we are modeling the conditional expectation and thus conditioning on X, which is here being treated as variable

The cool thing lies exactly here: Var(Y^) == Var(Y) - Var(Y-Y^) == Var Explained. Imagine the distribution along the line corresponding to the the Xs from the sample. That's what Var(Y^) really is!

@@easynomics880 Yeah. R2= 1-ESS/TSS or R2= RSS/TSS it is the proprotion of the variance of the Y that is explained by the regression model Y^. and in the video, i think it was a typo where ESS stands for the variance of erro.

![Eminem - Temporary (feat. Skylar Grey) [Official Music Video]](http://i.ytimg.com/vi/ZaK9Wi5ho0o/mqdefault.jpg)

Thanks for the nice video! One Question Sir, your first equality, does Var(y-y_hat) =?= Var(y) - Var(y_hat) ? y and y_hat independent?

what about the multiple linear regression??

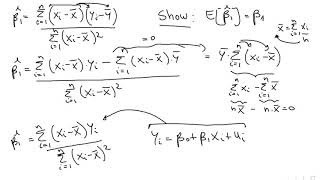

why did we get Beta square when taking it out ? coz variance ( a X ) = A^2 variance ( X)

woolridge book says that R=ey(hat)y. That means ey(hat)y=exy?? why???

Brother can you make a video on derivation of ARMA model, difference equation in time Series Econometrics derivation and it's solutions and numericals also,Ardl Bound test derivation and differential equation in time Series Econometrics derivation.

Thanks a lot !

why beta_0 is not a random variable?

So this equality is only valid outside of the framework of the classical lineal regression model, where we are modeling the conditional expectation and thus conditioning on X, which is here being treated as variable

thanks

Thanks

Thanks Bro!

Crazy video, but I am still confused after watching this...

Hi, R2=1-var(¨Y^)/var(Y)

Hi, that is not correct, remember that the R2 is the proportion of the variance of Y that is explained by the model: R2=var(Y^)/var(Y)

The cool thing lies exactly here: Var(Y^) == Var(Y) - Var(Y-Y^) == Var Explained. Imagine the distribution along the line corresponding to the the Xs from the sample. That's what Var(Y^) really is!

ESS: explained sum of squares = SSR: Residual sum of squares. Different notation.

@@easynomics880 Yeah. R2= 1-ESS/TSS or R2= RSS/TSS it is the proprotion of the variance of the Y that is explained by the regression model Y^. and in the video, i think it was a typo where ESS stands for the variance of erro.

RSS/TSS