Thanks Keyur! I am happy to hear that. Feel free to subscribe to my channel! more content is coming soon. Feel free to share it with those who you think may help them as well. Best Regards ,JD Econ

Hello Everyone! Thanks for watching! If you liked this video, please like and subscribe for more content! Your support helps me to create more video toturials. Please feel free to leave your comments and let me know if there is any topic you would like me to cover! ✅ Patreon: Support my channel for more content creation and get special deals and members bonus (such as help in your research and material downloads): www.patreon.com/JDEconomics ✅ Subscribe to my channel by clicking: ruclips.net/channel/UC5P21WGFO4WRUlAiGLcwymg Thanks a lot! JD Economics.

Thank you sir for this informative tutorial. Im just a newbie in Eviews. May I request sir? Can you include to your next tutorial how to do a stepwise multiple regresson. Thank you sir.

Thank you for this helpful video. I have some troubles in spurious regression so, Could you do the video about how to correct the autocorrelation and fix the model if it exists, please? Thank you so much.

Hi Thanks for your message. You can find the instructions here: Control Variables: www.eviews.com/help/helpintro.html#page/content%2Fcprogram-Program_Variables.html%23ww332 Instrumental Variable: www.eviews.com/help/helpintro.html#page/content%2Fcprogram-Program_Variables.html%23ww332 Kind Regards! JD Econ.

Congratulations for your channel, very useful . I would like do a garch- Midas model using accounting variables and volatility of stocks return from Brazil 🇧🇷. Do you have a tutorial in eviews for this? Thank you in advance

Hi Daiane, Thanks for your positive feedback! Unfortunately I didn't get yet to Garch Models, but it's something that many people has asked me about so I will be doing a video about it whenever I have some time! Feel free to susbcribe to the channel to receive the updates of my new videos. I wish you good luck! Regards, JD/

Hello! Very nice explanation! I have a question. I am doing a study in the timeframe of 16 years. It should be a time series so I converted the data from yearly to quarterly in Eviews. Is the analysis correct this way or is there another way to enter data that I have quarterly in Excel? Is there a problem if the kurtosis of the dependent variable is higher than 3 (6)? What modification can I do to get a correct one? Thank you if you respond.

Hello, I didn't really understand if the data you are using is yearly and transformed it to quarterly in Eviews. Kindly clarify that. If you convert yearly data to quarterly data, EViews will do like an average in split the yearly data into 4. I don't really recommend doing this as information is lost, there is no seasonality fluctuation. Finally, the kurthosis shouldn't be a problem. Feel free to subscribe to get notified of the coming videos! Regards, JD

@@JDEconomics Thank you very much! I have collected quarterly data (e.g. 2020 Q1 2020 Q2 etc.) in the excel file and I want to enter the file in Eviews. How can I do it? I just subscribed, really interested on your channel!

Thanks! And yes! Unfortunately that video (for some reason) recorded with low volume. The rest of the videos in my channel are ok. Have a great day! JD

@@JDEconomics Okay thank you for clarifying, I didn’t hear that part in the video. I have a question tho, currently studying for an exam :) When interpreting the coefficient of a time series data after differencing, do you interpret it the way you’d interpret a regular linear model or you make a reference to time in the interpretation. My question applies to both log and non-log models.

Many thanks 🙇

Ur welcome! Glad to hear you liked it! Good luck! JD

Good Contents with datasets

Thanks Keyur! I am happy to hear that. Feel free to subscribe to my channel! more content is coming soon. Feel free to share it with those who you think may help them as well.

Best Regards

,JD Econ

Hello Everyone! Thanks for watching! If you liked this video, please like and subscribe for more content! Your support helps me to create more video toturials. Please feel free to leave your comments and let me know if there is any topic you would like me to cover!

✅ Patreon: Support my channel for more content creation and get special deals and members bonus (such as help in your research and material downloads): www.patreon.com/JDEconomics

✅ Subscribe to my channel by clicking:

ruclips.net/channel/UC5P21WGFO4WRUlAiGLcwymg

Thanks a lot!

JD Economics.

Wonderful video! Look forward to learning GARCH with you by Eviews!

Thanks Will. Feel Free to check out my website for all the material available at jdeconomics.com

Regards!

Thank you sir for this informative tutorial. Im just a newbie in Eviews. May I request sir? Can you include to your next tutorial how to do a stepwise multiple regresson. Thank you sir.

Yes. I also invite you to check my website, where you will find all the tutorials and tips. Www.jdeconomics.com , kind regards!

thank you for this explanation! this really help a lot ^^

Thanks!

Very helpful, thank you

Great to hear!!

Could You make a video similar to this one for Stata versión? Thanks.

Sure! Thanks! JDEc.

Thank you for this helpful video. I have some troubles in spurious regression so, Could you do the video about how to correct the autocorrelation and fix the model if it exists, please? Thank you so much.

Hey! Nice explanation. How to accomodate for control variables and instrumental variables?

Hi Thanks for your message.

You can find the instructions here:

Control Variables: www.eviews.com/help/helpintro.html#page/content%2Fcprogram-Program_Variables.html%23ww332

Instrumental Variable: www.eviews.com/help/helpintro.html#page/content%2Fcprogram-Program_Variables.html%23ww332

Kind Regards!

JD Econ.

@@JDEconomics Thanks. :)

Congratulations for your channel, very useful . I would like do a garch- Midas model using accounting variables and volatility of stocks return from Brazil 🇧🇷. Do you have a tutorial in eviews for this? Thank you in advance

Hi Daiane, Thanks for your positive feedback! Unfortunately I didn't get yet to Garch Models, but it's something that many people has asked me about so I will be doing a video about it whenever I have some time! Feel free to susbcribe to the channel to receive the updates of my new videos. I wish you good luck! Regards, JD/

Hello! Very nice explanation!

I have a question. I am doing a study in the timeframe of 16 years. It should be a time series so I converted the data from yearly to quarterly in Eviews. Is the analysis correct this way or is there another way to enter data that I have quarterly in Excel?

Is there a problem if the kurtosis of the dependent variable is higher than 3 (6)? What modification can I do to get a correct one?

Thank you if you respond.

Hello, I didn't really understand if the data you are using is yearly and transformed it to quarterly in Eviews. Kindly clarify that. If you convert yearly data to quarterly data, EViews will do like an average in split the yearly data into 4. I don't really recommend doing this as information is lost, there is no seasonality fluctuation. Finally, the kurthosis shouldn't be a problem.

Feel free to subscribe to get notified of the coming videos!

Regards,

JD

@@JDEconomics Thank you very much! I have collected quarterly data (e.g. 2020 Q1 2020 Q2 etc.) in the excel file and I want to enter the file in Eviews. How can I do it?

I just subscribed, really interested on your channel!

Hello

Thank you so much sir

I would love to know why my data are above P value Sig (0.05) and possible solutions to make them significance

Sometimes adding more variables can help. Sometimes, removing variables can help. Cheers!

Really help full, but the level of volume is very low😊

Thanks! And yes! Unfortunately that video (for some reason) recorded with low volume. The rest of the videos in my channel are ok.

Have a great day! JD

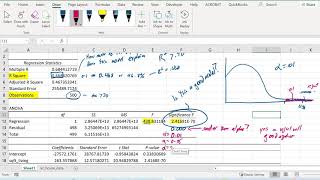

How can we build regression equation using this output

between 5:15 to 5:21 you said that brazil is statistically significant despite p value being less than 0.5%?

Hi, what’s the Null Hypothesis of the individual significance test?

@@JDEconomics sorry. i forgot what the null hypothesis was. i get it now

@@_Sam_-zh7sw no worries! Best regards

Hi, i will like to work with you.

Feel free to contact me at jdeconomics.inquiries@gmail.com

That is most likely a spurious correlation. You did not test for stationarity of the variables

Hi! Thanks for you comment. It is mentioned in the video. It is spurious. Regards, JD

@@JDEconomics Okay thank you for clarifying, I didn’t hear that part in the video. I have a question tho, currently studying for an exam :) When interpreting the coefficient of a time series data after differencing, do you interpret it the way you’d interpret a regular linear model or you make a reference to time in the interpretation. My question applies to both log and non-log models.

The audio is to low

Sorry about that. Regards