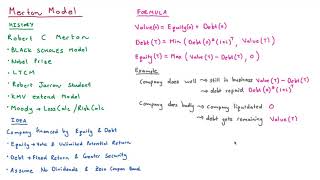

Thanks Brian. A curious thing with valuing equity as an option is that the BSM-implied value generally exceeds the observed market value. Does this imply that the BSM framework generally overestimates equity value, or that the market generally underestimates it (or maybe neither...)? Any thoughts on this?

Hi Brian, great video!!!! can we use etils value (the asse volatility formula you have) to calculate the volatility of a company and then use that in the black-scholes?

Hi Brian, first off, this video was very helpful, so thank you for the great explanation. However, my question is, does this model only work for public companies? Thanks!

@@BrianByrneFinance Ok one last question, can it be used for private companies using the value of equity from the balance sheet, obviously making it less precise, but would it be possible? Thanks in advance!

Hello Brian,

What would you do if you wanted to have the probability of default for 3 years from now?

Thank you Brian. This is really helpful. It is helping me in my Homework.

Dear Sir I encounter #Num Error during Solver routine how can I resolve this issue please advice.

Thanks Brian. A curious thing with valuing equity as an option is that the BSM-implied value generally exceeds the observed market value. Does this imply that the BSM framework generally overestimates equity value, or that the market generally underestimates it (or maybe neither...)? Any thoughts on this?

Hi Brian, great video!!!! can we use etils value (the asse volatility formula you have) to calculate the volatility of a company and then use that in the black-scholes?

Hi Brian, first off, this video was very helpful, so thank you for the great explanation. However, my question is, does this model only work for public companies?

Thanks!

Hi Alvaro, only public companies.

@@BrianByrneFinance Ok one last question, can it be used for private companies using the value of equity from the balance sheet, obviously making it less precise, but would it be possible?

Thanks in advance!