Hi. Thanks for very helpful videos. I am also wondering how you set the weights combinations in the blue table. It would have been helpful if you could spend a minute to explain that step as it is very confusing? Any help please

Good day, i have 30 stocks, for this procedure we have a lot of time to enter the Portfolio Std Dev, there is another way or formula to enter in this row or calculate this parameter? Greetings and thak you, have a nice one!!!

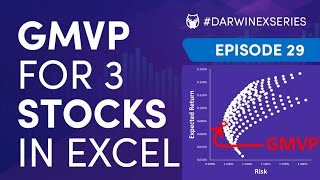

Hi Umi. The last two columns are calculated using formulae as shown in the video. The first 3 columns we done manually by myself using standard copy/paste/drag to complete... It's nothing more than every combination for 3 assets in increments of 5%. Hope that helps

@@TradeLikeAMachine hi, I'm also trying to replicate the blue table and I was wondering if there is a rationale to complete the columns of the weights. I attempted to do it manually but I think I'm replicating lines with same weight. For example if using increments of 2.5 instead than 5 how many totals rows should I have?

Hi. Thanks for very helpful videos. I am also wondering how you set the weights combinations in the blue table. It would have been helpful if you could spend a minute to explain that step as it is very confusing? Any help please

Good day, i have 30 stocks, for this procedure we have a lot of time to enter the Portfolio Std Dev, there is another way or formula to enter in this row or calculate this parameter? Greetings and thak you, have a nice one!!!

How do you generate that blue table? Is there a formula for it

Hi Umi. The last two columns are calculated using formulae as shown in the video. The first 3 columns we done manually by myself using standard copy/paste/drag to complete... It's nothing more than every combination for 3 assets in increments of 5%. Hope that helps

@@TradeLikeAMachine hi, I'm also trying to replicate the blue table and I was wondering if there is a rationale to complete the columns of the weights. I attempted to do it manually but I think I'm replicating lines with same weight. For example if using increments of 2.5 instead than 5 how many totals rows should I have?

Do you make the excel spreadsheets available?