yes, and also you have to extend the idea of efficient portfolios (Markowitz) to an equilibrium condition where all market is held (supply and demand), otherwise you can not conclude that the tangent portfolio is the market portfolio. It's easy to miss that insight because of the simplicity of the model.

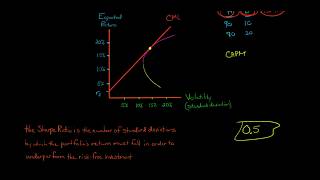

CML-return vs. risk graph; tgt to efficient frontier with left end at r_f denotes diff. portfolios as f(proportion) SML-return vs. beta graph; line denotes diff. portfolios in the CAPM equation

Hello, could anyone explain to me, how is it that it's impossible to invest in the CML at other points than in efficient frontier? Is it about CML being just the expectation and Efficient frontier the actual possible portfolios? I can't wrap my head around this.

Capital allocation line (CAL) is added to the efficient frontier. Points on capital allocation line (CAL) indicates borrowing (or lending money) to buy more (or less) of the optimal risky Portfolio. CML and market portfolio is special case of CAL and optimal risky portfolio.

Thanks. Key Point for me was that the CML represents portfolios that include the risk free asset.

yes, and also you have to extend the idea of efficient portfolios (Markowitz) to an equilibrium condition where all market is held (supply and demand), otherwise you can not conclude that the tangent portfolio is the market portfolio. It's easy to miss that insight because of the simplicity of the model.

In 5mins everything is explained

so nicely and smoothly. Thnx sir!

u r a genius! having gifted talent in teaching

so much better explaination than my professor.

Thank you very much professor ❤️. Keep posting videos. Knowledge forl all/ you are doing amazing job.

Thanks for your amazing video

Very helpful!

Great video!

thanks from France

Clarification about the white line: its the pink dot with varying amounts of riskless asset, the relative weights of the stocks stay the same!

Thanks McLaughlin!

No problem Rusty! I hope life is treating you well!

very helpful. thank you!

Can you explain me what does mean if portfolio lays on the right from CML? Does it make an investor a borrower?

CML-return vs. risk graph; tgt to efficient frontier with left end at r_f denotes diff. portfolios as f(proportion)

SML-return vs. beta graph; line denotes diff. portfolios in the CAPM equation

Thank you..

No problem!

Life saver

Thanks a lot.

thanks for this video

No problem!

So nice

thank you very much

Glad it helped!

Please help, are we dividing by the standard deviation of the EXCESS market return or by the standard deviation of the market return?

Hey, just a small request/suggestion. In the description, could you also mention the playlist this video is part of. Would be immensely helpful.

Awesome Video!

Do you have a scientific paper, that summarizes all of your information?😅

Thank you for that 🙏🙏🙏

how do you calculate the expected returns?

its more "historical return" than expected return

@TheCrackedFX Exactly, all this is past data statistics. Just history, useless.

tnx!

Hello, could anyone explain to me, how is it that it's impossible to invest in the CML at other points than in efficient frontier? Is it about CML being just the expectation and Efficient frontier the actual possible portfolios? I can't wrap my head around this.

Capital allocation line (CAL) is added to the efficient frontier. Points on capital allocation line (CAL) indicates borrowing (or lending money) to buy more (or less) of the optimal risky Portfolio. CML and market portfolio is special case of CAL and optimal risky portfolio.

So what is the optimum ratio of risk free assets?

ProfitusMaximus depends on the situation. You gotta do the math

Wow

What do I do with minus weights? Anybody I have an exam tomorrow?

Negative means you are shortselling

Has anybody ever told you that you sound exactly like foodwishes? Amerite?

Market LInes

All good, thanks, but...risk-free 4%. Seriously? This is cheating! ;P

Already 5% :)

Sharpe is reward to variability not volatility..volatility is captured by beta..and it is trenor

What incredibly frustrating delivery, at one point he repeats himself for 20 seconds.

zero analysis