Это видео недоступно.

Сожалеем об этом.

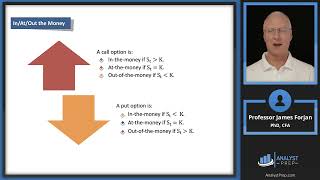

Principles of Asset Allocation (2024 Level III CFA® Exam - Reading 5)

HTML-код

- Опубликовано: 30 окт 2022

- Prep Packages for the CFA® Program offered by AnalystPrep (study notes, video lessons, question bank, mock exams, and much more):

Level I: analystprep.co...

Level II: analystprep.co...

Level III: analystprep.co...

Levels I, II & III (Lifetime access): analystprep.co...

Prep Packages for the FRM® Program:

FRM Part I & Part II (Lifetime access): analystprep.co...

Topic 2 - Asset Allocation and Related Decisions in Portfolio Management

Reading 5 - Principles of Asset Allocation

LOS : Describe and evaluate the use of mean-variance optimization in asset allocation.

LOS : Recommend and justify an asset allocation using mean-variance optimization.

LOS : Interpret and evaluate an asset allocation in relation to an investor’s economic balance sheet.

LOS : Discuss asset class liquidity considerations in asset allocation.

LOS : Explain absolute and relative risk budgets and their use in determining and implementing an asset allocation.

LOS : Describe how client needs and preferences regarding investment risks can be incorporated into asset allocation.

LOS : Discuss the use of Monte Carlo simulation and scenario analysis to evaluate the robustness of an asset allocation.

LOS : Describe the use of investment factors in constructing and analyzing an asset.

LOS : Recommend and justify an asset allocation based on the global market portfolio.

LOS : Describe and evaluate characteristics of liabilities that are relevant to asset allocation.

LOS : Discuss approaches to liability-relative asset allocation.

LOS : Recommend and justify a liability-relative asset allocation.

LOS : Recommend and justify an asset allocation using a goals-based approach.

LOS : Describe and evaluate heuristic and other approaches to asset allocation.

LOS : Discuss factors affecting rebalancing policy.

Dear James! Thanks a lot for your lectures! It's an absolute treasure

Glad you think so! If you like our video lessons, it would be appreciated if you could take 2 minutes of your time to leave us a review here: trustpilot.com/review/analystprep.com

This genuinely helps me a lot

thank you so much for wonderful video

So nice of you! If you like our video lessons, it would be appreciated if you could take 2 minutes of your time to leave us a Google review using this link: g.page/r/CQIlM78xSg01EB0/review

A kind note: at 57min, the Rm definition has a typo.

Is it just coincidence that the imputed returns also match the CAPM implied returns if you use the beta of each asset class?

So hold on, you've said that low risk high return isn't possible because some other guy said so... have a word. Don't rely on math.