Это видео недоступно.

Сожалеем об этом.

Options Strategies - Part I: Asset Returns Replication (2024 Level III CFA® Exam - Reading 7)

HTML-код

- Опубликовано: 14 авг 2024

- Prep Packages for the CFA® Program offered by AnalystPrep (study notes, video lessons, question bank, mock exams, and much more):

Level I: analystprep.co...

Level II: analystprep.co...

Level III: analystprep.co...

Levels I, II & III (Lifetime access): analystprep.co...

Prep Packages for the FRM® Program:

FRM Part I & Part II (Lifetime access): analystprep.co...

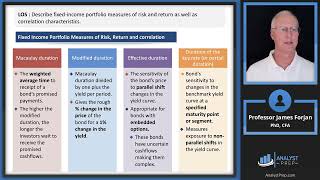

Topic 3 - Derivatives and Currency Management

Reading 7 - Options Strategies - Part I: Asset Returns Replication

LOS : Demonstrate how an asset’s returns may be replicated by using options.

at 5:25, I think there is a mistake in put option pay off function: Max (0, K-St)

You will exercise your right to sell the underlying (i.e. Stocks) when the prices of underlying falls, giving you the profit= so the payoff for the holder of put option=(K-St)

kindly have a look! (Payoff graph is also wrong for long put option)

I'm pretty sure that's the wrong payoff for the European Put Option?

Thanks Prof.Jim. Why didn't the synthetic equivalent include PV(K) in the 'All synthetic combinations' table?