I am a CFP, I studied finance at Virginia Tech, passed all my securities exams, and am now studying for CIMA. I have studied bond duration and convexity and interest rates, etc. multiple times... and this is the best explanation yet. Thank you!!!

The best explanation on RUclips! Finally someone who actually shows the application after the concept has been explained. Concept without application is useless. Great lesson!

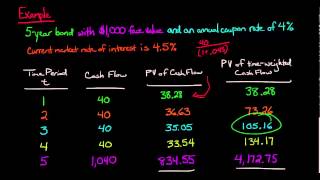

@@Edspira thank you! 1 question though, if I change the market rate assumption from 4.5% to 5.5%, I calculate a bond price of $936 which is -4.30% vs the $978 bond price at market rate of 4.5%...I know the difference is small but just curious to understand why the price decrease doesn't match exactly with the ModD which predicts a -4.43% decrease in bond price?

I really want to thank you for explaining everything about Bonds so well. I have to say you are much easier to understand than many finance professors I've had. Thank you so much and keep up the great work! You ROCK!

You are such an amazing explainer!! So many times after I learn things (in general), I feel like "why did they make it more complicated than it needed to be to learn it?? You are so skilled an breaking down the concept into straight forward steps and explaining the reasoning behind everything. It is also very helpful that you continued the example from the MacD, instead of putting brand new numbers in my brain and also tying the whole thing into a realistic application.

Nicely explained and presented. Modified duration is helpful in that it attempts to account for int rate changes and reinvestment risk. Macaulay duration does not incorporate either of these concepts, and so, other than understanding the weighted avg duration of the flows from a FI instrument, it isn't practically useful. "Duration" as you see it today will be expressed as mod duration (Morningstar, etc).

As the payment period increase (i.e. from annual to semi-annual), the Mod duration increases, suggesting a higher sensitivity to a price change. Why is that, please?

Quick question: If I see that an investment grade corporate bond has a duration of 6, I understand that a 1% move in rates results in -6% in the bond price, but WHAT RATES ARE WE TRACKING? The 10 Yr treasury? 5 year treasury? Thank you!!

THANKS A LOT. I DID NOT SEE ANY VIDEO EXPLAINING ModD SO WELL, IN SO MUCH DETAIL AND THAT TOO IN A SIMPLIFIED MANNER TO UNDETSTAND EASILY. Hope you'll continue uploading such videos. If possible kindly also upload a video of "How to calculate Rolling Returns of Mutual Funds in EXCEL taking historical daily data of 10-15 years with a rolling returns window of 7 years". Most of people are already doing that including me, but sat, sun stock market is closed, so in few cases, referring back corresponding 7 year back date, if that day is sat or sun, we have to take next NAV(Net Asset Value or Price) of Monday. So, how to tackle this issue. Usually people delete this data, so total data points reduces and affecting sample size resulting reduced accuracy of result. Your views on the subject means a lot to us. If you can tell your mail id, I can send you sample daily historical data of 15 years of a mutual fund (with NAV Date & NAV). Regards.

Hi, you explain it really clear. I am just wondering what will happen to the Modified duration within two coupon payment dates? Increase, decrease over time or uncertain and why.

lol ive sold all my holdings and put them into long term treasury etfs. vg and schwab have one that tracks bloomberg's, called VGLT. everyone is fighting over eachother to try and find the best CD/treasury auction to lock in ~5% interest like its the 1980s again.... meanwhile theyre all leaving 100% gain over 1-2 months on the table. the average duration of these ETFs like VGLT is like ~20 years with a 3% coupon. you already know the feds are about to break something and the overnight rate will plummet to "save the day." if 10 or 30 yr Treasury rates go back to 2019-2020 levels from where theyre at right now, these long term bond ETF's should ~double. its the prefect short play for the market. earning ~3% APR (basically the risk free rate) to play roulette until it lands on red. crazy times to be alive and watching rates. im thinking june/july will be some action. by then I should be ready to claim that sweet sweet long term capital gains tax rate. Im happy for everyone bragging about their 9% i bonds and 5% CD's... lol

Question: Modified Duration = Duration / (1 +YTM) But duration is expressed in number of years while the denominator is measured in terms of percentage. But why is it when you divide no. of years by percentage, you get a percentage i.e. Modified duration? Please enlighten me. Why does number of (years / Percentage) give you an answer expressed in percentage?

You mis-wrote the equation. Modified Duration = Mac Duration/(1+(YTM/K)), where k is the amount of compounding per year. Since K is expressed in years, the ending solution will be a percentage.

LIBOR is a benchmark rate that the world's leading banks charge each other for short-term loans, which is not always equivalent to the market rate. The following terms are often used to mean the market interest rate: effective interest rate yield to maturity discount rate The market interest rate is the prevailing rate of interest on loans determined by the demand and supply of credit and based on the duration and security of the loan.

What if I see the green letters the same way you guys see the purple letters, and vice versa, but we'll never know because what you think of as purple I have thought of as green my whole life and vice versa.. Don't even try to act like I didn't blow your minds just now.

It’s been 8 years, and this video still explain my 3 hours class better then my teacher, thanks a lot !

stg

I am a CFP, I studied finance at Virginia Tech, passed all my securities exams, and am now studying for CIMA. I have studied bond duration and convexity and interest rates, etc. multiple times... and this is the best explanation yet. Thank you!!!

⁰

The best explanation on RUclips! Finally someone who actually shows the application after the concept has been explained. Concept without application is useless. Great lesson!

Wow, thank you!

@@Edspira thank you! 1 question though, if I change the market rate assumption from 4.5% to 5.5%, I calculate a bond price of $936 which is -4.30% vs the $978 bond price at market rate of 4.5%...I know the difference is small but just curious to understand why the price decrease doesn't match exactly with the ModD which predicts a -4.43% decrease in bond price?

Quite possibly the best professor / explainer around - making my MSc Finance so much easier thank you

This channel is better than any other to understand concepts.

I really want to thank you for explaining everything about Bonds so well. I have to say you are much easier to understand than many finance professors I've had. Thank you so much and keep up the great work! You ROCK!

Mauro,

Bonds are always a difficult subject to teach/learn. Comments like these make my day. Thanks!

Okay, I rarely comment on videos, but I just want to say: THANK YOU SOOO MUCH!

i'm writing my final tomorrow. probably saved my semester. thank you sm

Good luck on your final!

You are such an amazing explainer!! So many times after I learn things (in general), I feel like "why did they make it more complicated than it needed to be to learn it?? You are so skilled an breaking down the concept into straight forward steps and explaining the reasoning behind everything. It is also very helpful that you continued the example from the MacD, instead of putting brand new numbers in my brain and also tying the whole thing into a realistic application.

The videos on duration are exceptional. Well done.

Thank you!

Excellent...like other comments, I have also watched many videos and this is the only video which clear allllll basic concept...thank a lot..

Thank you so much.

You've changed my life already!

Thanks man

Watched thousands of videos n finally got my concept clear by this 👍🏻

you are a lifesaver! thank you so much for making the time to make these videos

Love how there's barely any dislike in your videos.. You save everyone's butt! 😂

This content is absolutely amazing

Amazing video. I was looking for this. :)

Glad you liked it!

Thank you so much. I was having a hard time trying to understand this topic.

Glad it was helpful!

came here to try to understand the concept for the last time before my CFA1 exam

now i get finaly after months of tryings

Nicely explained and presented. Modified duration is helpful in that it attempts to account for int rate changes and reinvestment risk. Macaulay duration does not incorporate either of these concepts, and so, other than understanding the weighted avg duration of the flows from a FI instrument, it isn't practically useful. "Duration" as you see it today will be expressed as mod duration (Morningstar, etc).

Thanks a lot sir. I was really confused on this topic for weeks, but thankfully i found out the video. Made me understand it very well!

Awesome, i would also love to hear your lecture about convexity! (if available)

I go to a reputable university where fixed income is taught by an "expert". You're more helpful...for a lot less than 18k per semester.

Great video, you make this subject very clear!

As the payment period increase (i.e. from annual to semi-annual), the Mod duration increases, suggesting a higher sensitivity to a price change. Why is that, please?

thanks for both of these videos lol could not understand my university lecturer when she explained this too me

Quick question: If I see that an investment grade corporate bond has a duration of 6, I understand that a 1% move in rates results in -6% in the bond price, but WHAT RATES ARE WE TRACKING? The 10 Yr treasury? 5 year treasury? Thank you!!

this is number 50 in playlist - shouldnt it be after the video on macauley duration?

Thank you for this valuable information!!

You are so welcome!

Great video, thanks a lot

why would macaulay duration and modified duration be the same with continuos compounding?

Thank you man!!

No problem!

its really helpful and good example that you made thank you

Thanks!

Professor is modified duration also known as Fisher-Weil duration, or it’s a different topic?

THANKS A LOT. I DID NOT SEE ANY VIDEO EXPLAINING ModD SO WELL, IN SO MUCH DETAIL AND THAT TOO IN A SIMPLIFIED MANNER TO UNDETSTAND EASILY.

Hope you'll continue uploading such videos. If possible kindly also upload a video of "How to calculate Rolling Returns of Mutual Funds in EXCEL taking historical daily data of 10-15 years with a rolling returns window of 7 years". Most of people are already doing that including me, but sat, sun stock market is closed, so in few cases, referring back corresponding 7 year back date, if that day is sat or sun, we have to take next NAV(Net Asset Value or Price) of Monday. So, how to tackle this issue. Usually people delete this data, so total data points reduces and affecting sample size resulting reduced accuracy of result. Your views on the subject means a lot to us.

If you can tell your mail id, I can send you sample daily historical data of 15 years of a mutual fund (with NAV Date & NAV).

Regards.

now I got it! thank you

Great job! Best wishes

thanks!!!!! Man wish my professor did this.

Hi, you explain it really clear. I am just wondering what will happen to the Modified duration within two coupon payment dates? Increase, decrease over time or uncertain and why.

Fantastic clarity. Thank you.,

Hi, is modified duration the same as volatility (%)? Thanks!

very good teacher

Thank you very much for this useful video :)

excellent

What if yield decrease -1in formula will always show negative number however decrease in yield will increase price

If the yield decrease -1, the price change will be positive, since it will be -1 x ModD x (-1) => positive price change

Great your explain,thanks

really helpful thank you so much

lol ive sold all my holdings and put them into long term treasury etfs. vg and schwab have one that tracks bloomberg's, called VGLT. everyone is fighting over eachother to try and find the best CD/treasury auction to lock in ~5% interest like its the 1980s again.... meanwhile theyre all leaving 100% gain over 1-2 months on the table.

the average duration of these ETFs like VGLT is like ~20 years with a 3% coupon.

you already know the feds are about to break something and the overnight rate will plummet to "save the day." if 10 or 30 yr Treasury rates go back to 2019-2020 levels from where theyre at right now, these long term bond ETF's should ~double. its the prefect short play for the market.

earning ~3% APR (basically the risk free rate) to play roulette until it lands on red. crazy times to be alive and watching rates. im thinking june/july will be some action. by then I should be ready to claim that sweet sweet long term capital gains tax rate.

Im happy for everyone bragging about their 9% i bonds and 5% CD's... lol

Question: Modified Duration = Duration / (1 +YTM)

But duration is expressed in number of years while the denominator is measured in terms of percentage.

But why is it when you divide no. of years by percentage, you get a percentage i.e. Modified duration?

Please enlighten me. Why does number of (years / Percentage) give you an answer expressed in percentage?

You mis-wrote the equation. Modified Duration = Mac Duration/(1+(YTM/K)), where k is the amount of compounding per year. Since K is expressed in years, the ending solution will be a percentage.

what causes an increase in the yield?

Wonderful

when you say market interest rate - do you mean LIBOR? What is this rate in real life?

LIBOR is a benchmark rate that the world's leading banks charge each other for short-term loans, which is not always equivalent to the market rate. The following terms are often used to mean the market interest rate:

effective interest rate

yield to maturity

discount rate

The market interest rate is the prevailing rate of interest on loans determined by the demand and supply of credit and based on the duration and security of the loan.

Great of u

GREAT

I love you.

too soft

What if I see the green letters the same way you guys see the purple letters, and vice versa, but we'll never know because what you think of as purple I have thought of as green my whole life and vice versa.. Don't even try to act like I didn't blow your minds just now.

I've always thought this lol