Honestly speaking this is the best summary without leaving minute things. I wish i could have seen this before....now its only 10 days left for the attempt....Thank you so much Sir.

Yes. Put option holders are awaiting the sale of the underlying, for which they will receive the exercise price. The longer they have to wait, the lower the present value of the payoff. IFT Support Team

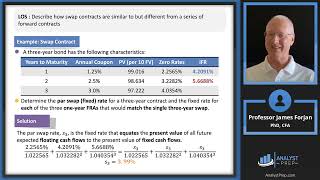

The value of a forward rate agreement at initiation is zero because neither party pays any money to the other. There is no value to either party. IFT Support Team

can you pls explain how effect of risk free rate of interest benefits call value and decrease put value in the same way can you explain how dividends benefits put but not call. what i think is, if the risk free rate increases then forward price increases. If the forward price increases it will decrease value for call and increases the value for put. In the same way Dividends will decrease the forward price and eventually it will increase the value for call. Kindly let me where I'm missing out.

The call option holder continues to earn interest on the money that could be expended later in paying the exercise price upon exercise of the option. For puts, the opposite argument prevails. A higher interest rate lowers the present value of the receipt of the exercise price upon exercise. Thus, the value today of what the put holder might receive at expiration is lower. IFT Support Team

+Mahmoud Rebai Thanks for your question. This Video is completely valid for the 2016 exams. Remember however that it is a summary of the reading. In case you need the full videos on the readings you will have to purchase that at www.ift.world.

How come in binomial valuations that is second last slide the probability of stock falling down is 0.75? When upward probability is .75 then downward probability should be 0.25! As total probability is 1.

Dear Lakshya, Yes and as explained in the video at 25:50 the slide correctly shows that the probability of a down move is 0.25. Perhaps, you were confused because of the handwriting. IFT Support Team

![Megan Thee Stallion - Roc Steady (feat. Flo Milli) [Official Video]](http://i.ytimg.com/vi/HozPPyqW0dY/mqdefault.jpg)

Honestly speaking this is the best summary without leaving minute things. I wish i could have seen this before....now its only 10 days left for the attempt....Thank you so much Sir.

hope you made it!!!!

@@yocanialice4784 yes..Aug-2022

Taught me in 10 mins what I couldn't understand in 1 hour

Thanks for the kind words.

IFT Support Team

This is thing....

but sometimes longer time to expiration (and interest rate) has indirect effect on put option value. because of lower pv of strike price

Yes. Put option holders are awaiting the sale of the underlying, for which they will receive the exercise price. The longer they have to wait, the lower the present value of the payoff.

IFT Support Team

sir, what would be the value of a forward rate agreement at initiation?

The value of a forward rate agreement at initiation is zero because neither party pays any money to the other. There is no value to either party.

IFT Support Team

can you pls explain how effect of risk free rate of interest benefits call value and decrease put value in the same way can you explain how dividends benefits put but not call.

what i think is, if the risk free rate increases then forward price increases. If the forward price increases it will decrease value for call and increases the value for put. In the same way Dividends will decrease the forward price and eventually it will increase the value for call. Kindly let me where I'm missing out.

The call option holder continues to earn interest on the money that could be expended later in paying the exercise price upon exercise of the option. For puts, the opposite argument prevails. A higher interest rate lowers the present value of the receipt of the exercise price upon exercise. Thus, the value today of what the put holder might receive at expiration is lower.

IFT Support Team

Excellent summary

Dear Kanu,

Thank you .

IFT Support Team

Hi , Do this video is updated for the June 2016 exam ?

+Mahmoud Rebai Thanks for your question. This Video is completely valid for the 2016 exams. Remember however that it is a summary of the reading. In case you need the full videos on the readings you will have to purchase that at www.ift.world.

How come in binomial valuations that is second last slide the probability of stock falling down is 0.75? When upward probability is .75 then downward probability should be 0.25! As total probability is 1.

Dear Lakshya,

Yes and as explained in the video at 25:50 the slide correctly shows that the probability of a down move is 0.25. Perhaps, you were confused because of the handwriting.

IFT Support Team

Hi Sir, how are 2017 videos diferent from that of 2014-15

the portion back then might have been different from 2017 maybe thats why