This is the best explanation I have ever heard. I had some difficulties in understanding the concepts with my teacher so I was looking for some videos here and your explanations with illustrations are so easy to understand, thank you so much for that.

This video was excactly what i was looking for! I cannot thank you enough for explaining to me the Weiner process and especially the part about sqrt(d(t)). Your slides contain as much graphics and informations as needed. Well done!

Thanks a lot for the best explain and derivation of the BM! May I ask where is the 2nd part of this topic? That how you convert back from discrete to continuous. Really appreciate it!

Very helpful video. I have one question though: choice of sqrt (t) is motivated by its slow convergence to 0, so it makes sense to use a higher root of (t) say cube-root. What is the reason to not do that ?

Thank you for appreciating the video. The first noteworthy impact of working with cube root of Delta t will be that variance of increment of W won't be an integral power of Delta t.

Thank you for this video. Really understandable. I know you didn't cover this, but are Wiener Processes used in Monte Carlo Simulationsfor finance? Thanks once again.

Thank you for the appreciation for the video, Hrithik. The Wiener process is a very important building block used to model the dynamic (continuous time) evolution of assets or market variables that underlie derivatives contracts. Your first exposure to this process happens when you write down the Geometric Brownian Motion (GBM) assumption that Black Scholes Merton model makes. Monte Carlo simulation is a numerical technique that will indeed make use of the Wiener process if the chosen model assumptions require it to do so.

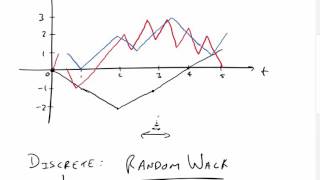

Hello Sengi Chin. In this case, W(t2) and W(t1) are not independent. Their covariance is given by cov(W(t1), W(t2)) = min(t1,t2) = t1. To work out the variance of W(t2) - W(t1), it is best to think of this difference to be made up of changes in the process over tiny discrete time invervals (say of length Delta t). Each of these changes is independent, and has variance of Delta t. The variance of the sum of these tiny changes will be the length of the time interval i.e. t2-t1.

This is the best and most lucid explanation I have ever seen. Thank you very much!!!

Glad you found the video helpful, Avadhesh.

one of the best video on Wiener process in entire youtube space

This is the best explanation I have ever heard. I had some difficulties in understanding the concepts with my teacher so I was looking for some videos here and your explanations with illustrations are so easy to understand, thank you so much for that.

Thank you for the kind words of appreciation. Glad that the video was helpful.

Intuitive way of understanding why the law of large numbers is talking about mean, and there is nothing that stops us from fluctuating a lot

Very detailed and easy to follow explanation. Thank you.

This video was excactly what i was looking for! I cannot thank you enough for explaining to me the Weiner process and especially the part about sqrt(d(t)). Your slides contain as much graphics and informations as needed. Well done!

Thank you for the appreciation, Iason. Glad that you found the video helpful.

I wanted to know why they use sqrt(del_t) as the variance and you explained that very intuitively.

Thank you for the upload.

Same! Seems like so many books gloss over this

Greatest lesson I've ever heard on Wiener Processes. Thanks very much!

Very intuitively explained what is so abstract and difficult to understand.

Excellent video, made the concepts crystal clear. thank you for this

Glad you found the video helpful, Syed.

please make a video about Ito's lemma as well...

and thank you for the video, you made it so easy to understand

Sure, will do. Glad that you found this video helpful.

@@finRGB Keeping an eye open for the Ito video, thank you!!!

Fantastic video. Incredibly helpful and so concise. Thank you very much!

This is amazing, really clear, impressive

Glad you found the video helpful, Sherry.

This is such a great explanation! Thanks a lot for sharing your knowledge.

Glad that you found the video helpful, Ruben.

Thanks a lot for the best explain and derivation of the BM! May I ask where is the 2nd part of this topic? That how you convert back from discrete to continuous. Really appreciate it!

Amazing lesson. ❤❤

Great explanation :)

Thank you so much for this video.. very helpful

superb presentation

Nicely explained

This is really great.....

perfectly explained thanks

This is just brilliant. Thank you!

Thank you for the appreciation, viiarush.

what software do you use? the handwriting is very nice

Very helpful video. I have one question though: choice of sqrt (t) is motivated by its slow convergence to 0, so it makes sense to use a higher root of (t) say cube-root. What is the reason to not do that ?

Thank you for appreciating the video. The first noteworthy impact of working with cube root of Delta t will be that variance of increment of W won't be an integral power of Delta t.

Why do we scale epsilon by sqrt(del_t)? I'm curious to understand why the square root is there.

Hello Charlie3k, the logic for sqrt(del_t) is covered from 9:20 onwards. Cheers

@@finRGB Ah, my apologies for missing that timestamp. Thank you for the fast response and the excellent video! :)

Thank you so much

Excellent

Thank you for this video. Really understandable. I know you didn't cover this, but are Wiener Processes used in Monte Carlo Simulationsfor finance?

Thanks once again.

Thank you for the appreciation for the video, Hrithik. The Wiener process is a very important building block used to model the dynamic (continuous time) evolution of assets or market variables that underlie derivatives contracts. Your first exposure to this process happens when you write down the Geometric Brownian Motion (GBM) assumption that Black Scholes Merton model makes. Monte Carlo simulation is a numerical technique that will indeed make use of the Wiener process if the chosen model assumptions require it to do so.

thank you for the video!

Thanks,very nice!

Thank you so much!

Thanks a lot

I think W_{t_2} - W_{t_1} ~ N(0,t_2 +t_1) (instead of minus), since Var(X-Y) = Var(X) + Var(Y) if X and Y are independent r.v.

Hello Sengi Chin. In this case, W(t2) and W(t1) are not independent. Their covariance is given by cov(W(t1), W(t2)) = min(t1,t2) = t1. To work out the variance of W(t2) - W(t1), it is best to think of this difference to be made up of changes in the process over tiny discrete time invervals (say of length Delta t). Each of these changes is independent, and has variance of Delta t. The variance of the sum of these tiny changes will be the length of the time interval i.e. t2-t1.

Thanks a lot!

thanks!

😁

very good explanation, nice and simple thanks

Thank you for the appreciation, Yamete Oni-chan.