FRM: TI BA II+ to compute bond yield (YTM)

HTML-код

- Опубликовано: 8 июл 2012

- Given four inputs (price, term/maturity, coupon rate, and face/par value), we can use the calculator's I/Y to find the bond's yield (yield to maturity). For more financial risk videos, visit our website! www.bionicturtle.com

I paid over 100 dollars for a Pearson textbook that didn't teach me as well as this video for free. Pearson is an evil company. Keep up the 'good work'.

We are happy to hear that our video was helpful! Thank you for watching!

Same here, except for us, the evil is called McGraw-Hill and their online courseware CONNECT.

What is the Present Value of your Pearson textbook??

@@davidp18 goodwill

@@davidp18 negative :) ( somehow...)

10 years later this video is still amazing. Fantastic teacher!

Kind of shows you that things in finance and accounting world does not change much at all with how it works.

@@kgregorius8550or at least the schooling part of it

I had been another video that used P/Y and C/Y. These ended up causing issues with my results, so I re-set them to 1 again. So glad I tuned in - this is very helpful.

Thanks a ton , David! Your videos are really really helpful.

I forgot to use negative sign for PV and as a result I kept getting the Error 5. And finally I'm feeling relieved.

Also, I am feeling grateful for those who ask such questions , nd makes it easy for us. Thanks a lot.

Thank you for watching! We are happy to hear that our video was so helpful :)

Thank you ! My college degree depends on this video haha

Great work! Too late to find such wonderful video after surviving my MBA 2 years ago. My financial professors didn't teach as clear or understandable as in this video.

Thank you so much for this video! I passed a second year uni paper in New Zealand thanks to you ;) got B+ which I was stoked with :)

I had forgotten how to calculate cost of equity using the BA 2 calculator, thank you!

Thank you for sharing the method!

I'm confused on a question. A 2-year Treasury bond with principal $100, price $98.39, coupon rate 6% per annum and paid semiannually.

The result given by the calculator is 3.4377. So, the yield to maturity per annum should be 6.8754%. But if I calculate this way: 3*e^(-y*0.5)+3*e^(-y*1)+3*e^(-y*1.5)+103*e^(-y*2)=98.39, the answer came out as 6.5798%. Why there is the slight difference?

Can somebody help me answer it? Thank you!

Hi, what kind of app do you guys use to screencast the calculator?

Wow, I'm glad I turned to this video. I kept getting "Error 5" and now I figured it out. Thank you!

You're welcome! I'm happy to hear that our video was so helpful!

U forget put negative sign for PV?

thank you very much indeed for making this helpful video. what helped me is to enter negative pv and pmt.

Thank you for watching!

Thank you for this video!! Very easy to understand!!! You're a lifesaver!!

You're welcome! Thank you for watching! :)

You should teach the use of the P/Y and the xP/Y keys. This will make life easier.

A 7 year $10,500 bond paying a coupon rate of

5.50% compounded semi-annually was purchased

at 98.30. Calculate the yield at the time of purchase of the bond.

THe answer given to me on my assignment was 5.80...im so confused.

Thank you so so so much! I feel way more confident about my finance final exam tomorrow now!

+Olivia Huang You're welcome! We are happy to hear that our video was so helpful, and we hope you did well on your exam :)

Can you please confirmm this PV formula that I understood from your video:

Year 0.5 FV = 2/(1+(YTM/2))^0.5/2

Thank you so much. Im just stared how to use ba 2 plus. This video is very easy to understand it.

Thank you for this. It was very well explained.

Definitively what I needed, txs!

Thank you so much I didn't realize you had to hit cpt then hit the one you want to solve for😅

This was so easy to follow! Thank you

You're welcome! Thank you for watching! We are happy to hear that our video was so helpful :)

I type everything exactly the same as on video, but my result is 35,2 :(

Something must be wrong with the setup I guess. How can I solve that?!

i have the same , what did u do to fix it can anyone help i have an exam

Yea same

Maybe its ur PY and CY setting?

simply lovely..well explained!

Thanks Dave for explaining it !!!

Bionic Turtle-- I entered everything in on my calculator exactly as you did but my calculator gave me the correct answer without having to multiply by 2 at the end to get 5.87. Why is that? Is my calculator on a different setting or something?If you had not already told the answer, I would have ended up multiplying 5.87 x 2 to get 11.74

Excellent video. Thanks!

Bruno Falconi You're welcome! Glad you liked it!

so great. made it easy to understand.

can you please make a video on how to cal. ytm at zero coupon bond by using financial calculator

Life saver! Thank you!

This is a great video. Quite helpful.

We are happy to hear our video was so helpful! Thank you for watching :)

Thanks! Right, well the practical impacts and nuances of negative yield don't really enter here: this is "merely" an internally consistent TVM (math) calculation that returns a nominal IRR. We could use =-PV(YTM = 0, n = 10, PMT = 2, FV = 100) = $120.00 to infer a $120.00 breakeven such that a price above $120 for a $100 face, 4% coupon, 5 year bond will produce a negative YTM

Super useful video! Thank you !!

You're welcome! Thank you for watching!

what do you set the p/yr to?

Great video. Thank you!

You're welcome! Thank you for watching!

great speech!

Calculate the fair present value of the following bonds, all of which have a 10% coupon rate (paid semi-annually) a face value of $1,000.00 and a required rate of return of 8%.

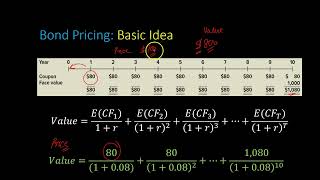

a. The bond has 10 years remaining to maturity

b. The bond has 15 years remaining to maturity

c. The bond had 20 years remaining to maturity

d. What do your answers to parts a - c tell you about the relation between present value and time to maturity?

I somehow find it easier to use CF function to find the YTM or price of the bond

We put rate *2 to find semi anual ytm. But if we want the anual Ytm what i'll do ??

My BA II Plus gave me a YTM of 5.87 when I pressed I/Y. I didn't need to multiply it by 2.

Thanks for the help! Sux that I’ll forget it by next week.

I keep getting the value 35.21667 for I/Y when I used the same inputs. Please advise what I'm doing wrong. I recalled all the inputs and they match what you said to put in the video.

Nvm! I got it. I had P/Y set to 12. I set it back to 1.

Even i am getting 35.21 for I/Y. So just want to know how to set P/Y to 1?

Why no setting in P/Y=2??

The excel table already provide that ur YTM is represented in semiannual, not the standard annual and it can be confusing for students with optional answers

He should really be teach users how to use the 2nd P/Y and C/Y features on the calculator to match the number of coupons per year or compounding per year. If you do that then you don't have worry about multiplying at the end to get the correct answer.

Not sure why but my calcualtor spits out my I/Y as 5.869% with the same inputs and not the 2.3% you get that you had to multiply by 2 if anyone can help me thank you

thank u, i have my finance final tomorrow 😢

I don't understand why you adjust N for the compounding period and then also adjust the p/y to tell it how many times it compounds per year.

Well, firstly thanks for your video, it really helps me! But I still have a problem, I do what you said to compute the YTM of a 1000 face value bond, with 5%coupon rate, 10 periods (annually), and the current price is 1268$. The outcome is -1.91. I don't know why it is negative instead of positive?

If you didn't input your initial PV as negative (-), then your answer will be negative.

If the semi-annual coupon rate is 4%, why do we still need to divide by 2?

Superficially it's about syntax. My view is that rates by default should be given in PER ANNUM terms, to avoid long run confusion; e.g., semi-annual coupon rate of 4.0% means "the coupon rate is 4.0% per annum and pays semi-annually" which implies, of course, 2.0% every six months. We've been teaching finance for over a decade and I really believe it's less confusing in the long run if interest rates are expressed in their per annum terms. (e.g., notable authors like Hull do this. When this convention is maintained, we know that a given 3.0% interest rate, for example, is per annum). Alternatively, if the problem wants to be goofy, it can do that but it should be specific eg "The bond pays a 2.0% coupon every six months." Substantively, we divide by 2 to get the PER-PERIOD coupon rate; the most important thing in the calculation solution is to be consistent about the per-period assumptions. Dividing the coupon rate by 2 is consistent with multiplying the term of 5 years by 2, because we are ultimately just solving for the per period yield where, in this case, the number of periods is 5*2 = 10 period, and each period happens to be six months (but the calculator doesn't care about the six months, it is solving based on 10 periods because the yield is compounded twice per year).. Thanks!

Bionic Turtle ah that makes sense, thanks! Great video as always!

Also if you use the P/Y you won't have to convert the interest rate to per annum.

Thank you so much, ❤

Super helpful!

Thank you for watching! We are happy to hear that our video was helpful.

Thanks mate you a star

a company has 5000 of 5% coupon bond which are trading at 95% of par value and have one year to maturity what is the cost of debt

Why I get 35.22 by doing as same as the steps in the video?

thanks very much helpful 11 years on

So helpful

Thank you so much

Thank you sir 🙏🏾🙏🏾🙏🏾🙏🏾

What is $D$15 on the dcf?

this dude is gooooood

You are taking semi-annual YTM and multiplying by 2 to get annual YTM. Is that not wrong? Instead Annual YTM = (1 + Semiannual YTM)^2 -1 so that YTM= 5.96%. Is there some silly convention I'm overlooking?

It's not silly, it's a well-established convention, it is called the bond-equivalent basis (see Fabozzi or many others). Bond-equivalent basis refers to "5.87% per annum with semi-annual compounding.," in this case. That is, the 5.87% is not the effective interest rate, it is the STATED (aka, NOMINAL) interest rate and by itself makes no assumption about the compound frequency. We always want to express interest rates in PER ANNUM terms but a stated, per annum rate by itself is not enough information to convey the exact rate b/c we won't know the compound frequency. "Bond equivalent basis" refers to s.a. compound frequency (k = 2 periods per year) because it is the most common as most bonds pay a semi-annual coupon. Thanks,

Nice clarification. Thanks.

thank you !!!

If you set p/y to 2 and C/y to 2 by pressing 2nd I/y 2 and enter you will not have to multiply by two at the end.

true, we just don't recommend this in an exam setting because you have to change them each time (eg, annual). It's more reliable (less error prone) to keep them on p/y = c/y = 1, is our experience

Thanks thanks a tonne!!!!

Thank you for watching!

uggg I have a long way to go. I completely misinterpreted the question and what it was asking for. I glossed over "coupon" and "yield to maturity". I'm so used to sovling for FV that I was plugging everything away in my calc and when you skipped i/y I was like errrr, I read the question wrong.

but, I have time to get all of this right. I can do this. I am the cfa, be the cfa, let the cfa flow through you. hummmmm

Thank you..:)

thank you so much !!!

You're welcome! Thank you for watching!

Thank you so much this video correct my lot of errors

All you have to do is split the coupon and term in half then multiply your answer by 2.

i get error 5 when using my values

save mt life turtle man

I’m following along and I keep getting 35.22

Am thinking, examiners always want to see some workouts, but u just input all the numbers in the calc and u get a final answer, i don't get that why. Btw no student in an exam room can pull that lil trik of inputing the numbers and writing down the final answer. Just do a normal calculation and use the calc where it's obvious

this is a normal use of the TVM keystrokes, i have no idea what you mean by "just do a normal calculation." It would take many more keystrokes to detail the DCF. Of course you can write stuff down while doing it. I showed the numbers in excel because it's more clear than my handwriting.

@@bionicturtle just write it down. I cannot understand wat u r doing on the calc, an working to show how to get yield, that's all

@@arfenmalik1717 the purpose of this video is to explain how the TI BA II+ calculator is used to solve for a bond's yield (YTM). The TI BA II+ is the most commonly used (among approved) calculators for the CFA and FRM. For such problems, you need the calculator; YTM is an IRR, it's solution is iterative, not analytical, you NEED the calculator. I really have no idea what you are trying to say.

@@bionicturtle as a finace student i know examiners want to see the workings, but u entered everything in the calc

@@arfenmalik1717 Yes I did: YTM has no analytical solution, it requires an iteration by the calculator

sounds like kermit.

glad you took the time to contribute a comment, it was worth the wait

Hahaha! Thank you for your help! My professor doesn't speak English so I am very thankful for an explanation I can understand. I will be back to your page for more :)

@@allisonwelch7733 in that case, we forgive you and look forward to your return!

so slow

Yuck, get a 12C

Bla bla bla... go to the point directly!

Yea sure, look: I'm always trying to improve on that. It's harder than it looks. But thanks for the feedback

You made it 10x longer while explaining every single little detail. You just needed 30 second to explain your calculation

Seriously! Almost 10 minutes, he talks to much!