Размер видео: 1280 X 720853 X 480640 X 360

Показать панель управления

Автовоспроизведение

Автоповтор

Million thanks for your explanation! very clear!!

Great video! It clears my concept on those terms. Thank you so much!

so so so helpful!!! Explicit ! Amazing in every way, thanks a lot.

Thank you for watching!

god bless you @ David, these videos are so helpful

WELL EXPLAINED SIR. !

Well explained.

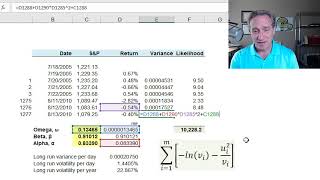

It's a great lecture regarding a variance to the GARCH model. How Can I GARCH model convert to IV "Idiosyncratic Volatility"? please guide me.

Cool

![Blox Fruits Dragon Rework Update [Full Stream]](http://i.ytimg.com/vi/EqDAp8udhm0/mqdefault.jpg)

Million thanks for your explanation! very clear!!

Great video! It clears my concept on those terms. Thank you so much!

so so so helpful!!! Explicit ! Amazing in every way, thanks a lot.

Thank you for watching!

god bless you @ David, these videos are so helpful

WELL EXPLAINED SIR. !

Well explained.

It's a great lecture regarding a variance to the GARCH model. How Can I GARCH model convert to IV "Idiosyncratic Volatility"? please guide me.

Cool