Lognormal property of stock prices assumed by Black-Scholes (FRM T4-10)

US

Войти

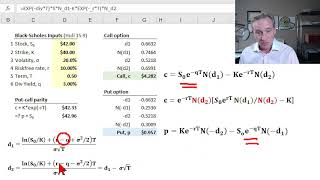

Black Scholes Merton option pricing model (FRM T4-11)

11:53

Why are Stock Prices Lognormal?

12:28

The Trillion Dollar Equation

31:22

MARK 마크 '프락치 (Fraktsiya) (Feat. 이영지)' MV

03:20

Yelling at my GF in front of FaZe Rug and Brawadis..

22:49

Avengers wake up, Marvel Rivals is fire

18:15

Lognormal property of stock prices assumed by Black-Scholes (FRM T4-10)

Bionic Turtle

Подписаться

100 тыс.

Скачать

Готовим ссылку...

Просмотров 25 тыс.

0

0

Добавить в

Мой плейлист

Посмотреть позже

Поделиться

Поделиться

HTML-код

Размер видео:

1280 X 720

853 X 480

640 X 360

Показать панель управления

Автовоспроизведение

Автоповтор

Опубликовано: 17 янв 2025

Комментарии • 25

Следующие

Автовоспроизведение

11:53

Black Scholes Merton option pricing model (FRM T4-11)

Bionic Turtle

Просмотров 27 тыс.

12:28

Why are Stock Prices Lognormal?

Options A to Z - Facebook Trading Group

Просмотров 7 тыс.

31:22

The Trillion Dollar Equation

Veritasium

Просмотров 10 млн

03:20

MARK 마크 '프락치 (Fraktsiya) (Feat. 이영지)' MV

SMTOWN

Просмотров 1,6 млн

22:49

Yelling at my GF in front of FaZe Rug and Brawadis..

Sherman

Просмотров 657 тыс.

18:15

Avengers wake up, Marvel Rivals is fire

zanny

Просмотров 1,1 млн

13:22

Making Cookies For Santa

Johnnie Guilbert

Просмотров 251 тыс.

14:20

CFA Level I. Module 10 3 Lognormal Distribution, Simulations

cfa studymaterials

Просмотров 8 тыс.

18:10

Option delta (FRM T4-13)

Bionic Turtle

Просмотров 15 тыс.

9:36

The Lognormal Model of Stock Prices

Mike, the Mathematician

Просмотров 2 тыс.

18:02

Three approaches to value at risk (VaR) and volatility (FRM T4-1)

Bionic Turtle

Просмотров 43 тыс.

36:11

How to Think About Risk with Howard Marks

Oaktree Capital

Просмотров 389 тыс.

14:12

How to interpret N(d1) and N(d2) in Black Scholes Merton (FRM T4-12)

Bionic Turtle

Просмотров 49 тыс.

19:46

Dynamic option delta hedge (FRM T4-14)

Bionic Turtle

Просмотров 39 тыс.

50:41

The Psychology of Hedge Fund Traders (Insights from Elite Trading Psychologist)

SMB Capital

Просмотров 474 тыс.

20:32

Normal and Lognormal Distributions (SOA Exam P - Probability - Univariate Random Variables)

AnalystPrep

Просмотров 15 тыс.

00:36

Бог и Дьявол "Игры в Кальмара"

Star Family

Просмотров 937 тыс.

01:00

На ЭТО можно смотреть БЕСКОНЕЧНО 👌👌👌

БЕЗУМНЫЙ СПОРТ

Просмотров 745 тыс.

00:15

Solo Chef Adventures: Mom Hacks for Cooking with a Tiny Taster! 🍳👶 #Kitchen #Cooking

Doods

Просмотров 7 млн

00:58

Провальная Акция в Pizza Hut 🍕

Тимур Сидельников

Просмотров 144 тыс.

10:06

Сидел бы дома 🤕

Valera Ghosther

Просмотров 227 тыс.

26:25

HUSTLE VLOG - UFC 311 , ЛОС-АНДЖЕЛЕС

adam zubayraev

Просмотров 165 тыс.

35:05

Кто заплатит за пожары в Лос-Анджелесе: простой ответ или сложный вопрос?

АМЕРИКА Наизнанку

Просмотров 141 тыс.

00:35

Игра в калмэра в реальной жизни

МЯТНАЯ ФАНТА

Просмотров 102 тыс.