the crispness & clarity, of an oft "black magic arts" subject, is refreshing; thank you. The best "gentle introduction" ... with nary an equation in sight.

I love how this video only has about 6000 views and actually talks about how option prices behave, whereas a daily Meet Kevin video gets over 600k views and while saying absolutely nothing.

Thing is, most people get into trading to get rich quick and are not genuinely interested in the topic. The irony is that the more you "learn" from so called gurus, the worse you become as a trader/investor.

@@andreasb8232 precisely, like every other profession this is a profession, we dedicate 3-4 years of our lives getting a degree and learning about that trade but expect to become a profitable trader or investor in a month or 2. given the kind of talent this profession involves one should be willing to spend even more time and be dedicated to it, that is one of the reasons they lose money and then blame everything else other than their behavior

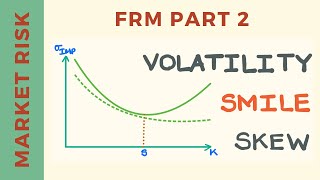

I LOVE how with many instruments, the volatility smile becomes far more convex AFTER a tail event, after which it is typically less likely for that fat tail event happening again in the following weeks, which makes for some interesting more complex strategies

Well, not necessarily more complex. You can just sell OTM puts AFTER a big drop and it's super simple and very often you just keep the premium. Only to do with options of stocks you are ok to go long if assigned, of course.

Very crisp and clear video. I always wonder how option sellers decide the implied volatility at which to sell a specific strike option , as the stock prices mostly donot follow lognormal distribution. Do they find the probability of option expiring in money by the other fat tailed parametric distribution the stock price movement resembles, set that probability equal to N(d2) of BSM, thereafter find IV from N(d2) and price of the option as per BSM? Just a wild guess, will be highly appreciated if u make a video on this topic.

Thanks for the clarification on BSM. With the high importance of volatility modeling; may i request a video on the Bergomi model and it's relevance to option pricing. Thanks I appreciate your content.

When you realize he knows what he is talking about and has barely any views vs mouth breathers who don't know the first thing about topics they speak on it becomes very easy to see why the market rewards the smart disciplined participants and takes away from the lazy, uninformed participants.

Patrick Boyle I had a look at your video channel ... there are many videos i am going to watch in these coming days... really thank you. But wondered if you had any videos about arbitrage in volatility trading.

I guess with a deep in the money option you pay less in absolute terms for volatility but more on a relative basis. In a deep in the money call option most of the premiums is for the in the money portion of the call.

Wouldn't an call option with a high strike price relative to the current underlying price be an in the money call as opposed to an out of the money call? I 🤔

@@jarenshyers9024 hahaha yeah omg wtf was i on about... 🤦♂️I confused what he was saying @ 5:20. I thought he meant high underlying price is more likely to be an out of the money call

Finally someone on youtube who actually knows what he is talking about.

Thanks!

This guy understands the difference between financial entertainment and financial education!

the crispness & clarity, of an oft "black magic arts" subject, is refreshing; thank you.

The best "gentle introduction" ... with nary an equation in sight.

I love how this video only has about 6000 views and actually talks about how option prices behave, whereas a daily Meet Kevin video gets over 600k views and while saying absolutely nothing.

Thing is, most people get into trading to get rich quick and are not genuinely interested in the topic. The irony is that the more you "learn" from so called gurus, the worse you become as a trader/investor.

Don't feel bad, a lot can be said about it.

@@andreasb8232 precisely, like every other profession this is a profession, we dedicate 3-4 years of our lives getting a degree and learning about that trade but expect to become a profitable trader or investor in a month or 2. given the kind of talent this profession involves one should be willing to spend even more time and be dedicated to it, that is one of the reasons they lose money and then blame everything else other than their behavior

Check out tech stocks. Smiles are making a comeback. The market is about to go boom boom.

This simple video taught me more about real-world options trading than anything I had ever seen before. Amazing content. Thank you!

Mate, your channel is so underrated!!!

Took you all of 4 minutes to explain what my university professor has been unable to articulate in 4 months (and counting!). Thanks

I LOVE how with many instruments, the volatility smile becomes far more convex AFTER a tail event, after which it is typically less likely for that fat tail event happening again in the following weeks, which makes for some interesting more complex strategies

Well, not necessarily more complex. You can just sell OTM puts AFTER a big drop and it's super simple and very often you just keep the premium. Only to do with options of stocks you are ok to go long if assigned, of course.

One of the best channels on RUclips. Thank you!

Clear & Concise ! Look forward to more

Wow -- what good commentary! Very high quality discussion.

I enjoyed the video. You explain the concept really well

Excellent video, so clearly explained and great examples. You are a pro my guy.

My god finally, not some idiot yelling and screaming to the moon for 1 million views lol you’re amazing thank you.

Wow, great info! Thank you.

Thanks Patrick very Clear and Concise . I've Subbed 👌.

Very helpful video, thanks!!

Awesome video mate, subscribed!

Great video!

Thanks! Great video!

Perfect!

At 3:00 you mean lognormal returns not prices

Very crisp and clear video. I always wonder how option sellers decide the implied volatility at which to sell a specific strike option , as the stock prices mostly donot follow lognormal distribution. Do they find the probability of option expiring in money by the other fat tailed parametric distribution the stock price movement resembles, set that probability equal to N(d2) of BSM, thereafter find IV from N(d2) and price of the option as per BSM? Just a wild guess, will be highly appreciated if u make a video on this topic.

Thanks for the clarification on BSM. With the high importance of volatility modeling; may i request a video on the Bergomi model and it's relevance to option pricing.

Thanks I appreciate your content.

Thanks, I am putting together some ideas for new videos right now and will add that to the list.

When you realize he knows what he is talking about and has barely any views vs mouth breathers who don't know the first thing about topics they speak on it becomes very easy to see why the market rewards the smart disciplined participants and takes away from the lazy, uninformed participants.

Excellent thank you so much !

You are welcome!

Patrick Boyle I had a look at your video channel ... there are many videos i am going to watch in these coming days... really thank you. But wondered if you had any videos about arbitrage in volatility trading.

I guess with a deep in the money option you pay less in absolute terms for volatility but more on a relative basis. In a deep in the money call option most of the premiums is for the in the money portion of the call.

How can we take advantage of vol. smile. Should we roll options closer/further from ITM/OTM as volatility increases/decreases.

Volatility skew only exists with derivatives?

So, before 1987, did the volatility curve more resemble a "V"?

excellent content :-)

Glad you enjoyed it

4:57

Wouldn't an call option with a high strike price relative to the current underlying price be an in the money call as opposed to an out of the money call? I 🤔

No, a call option with a strike ABOVE the current price is out. A put with a strike above the current price is in.

@@jarenshyers9024 hahaha yeah omg wtf was i on about... 🤦♂️I confused what he was saying @ 5:20. I thought he meant high underlying price is more likely to be an out of the money call

You're saying Black Scholes isn't completely accurate because people who sell at the money options price in a premium?

He is saying that the black scholes model isn't completely accurate because it assumes a perfect world

I can't understand that ... I want to learn but its another language