Hey Nayantara, I am glad it helped you. I hope it can help as many people as possible. Maybe I should change the name of the channel to remove UofT haha. Actually most of the viewers are not even from Canada.

you are an absolute legend for posting this. It was so helpful! You organised the video and the results in such an great way the results became iterative. Thank you!

Grim Reaper He is taking the derivative of the equation he had above, so exponent comes down, rewrite equation and the power is what you had before '-1' so in this case it was to the power 2 but now its to the power one. After that you must multiply it by the derivative of the equation inside the brackets, thus giving him (-1). I hope this helps

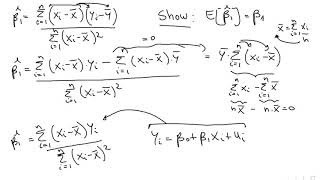

ok, but it`s not clear yet for me, excuse me...I hope you understand me...then you write at 16:44 ... =SUMXi2...but how can this be able? it is a Xi uppercase times xi lowercase? could you explain please? thanks again

I found there are a lot of existing videos for Matrix Algebra. Is there any particular topic you were interested in ? I particularly like this playlist that uses an intuition based approach: ruclips.net/p/PLZHQObOWTQDPD3MizzM2xVFitgF8hE_ab

Thanks for the reply. The link looks useful. The course I am doing follows M. Verbeek, A Guide to Modern Econometrics. We have started with OLS estimation and moved on to maximum likelihood estimation, methods of moments estimation, and Within and Random Effects Estimation using panel data. Although I have been taught about OLS estimation before, it has adopted the single observation proofs/derivations, such as this video. However now everything is being taught in vector/matrix notation, which I'm finding a bit confusing. There is a particular example; I am struggling with seeing how one can easily go from summation notation using vectors to matrix notation, particularly when deriving the OLS estimator. Thanks again!

Oh, you are doing graduate level econometrics. I might do a video when I go back to the office at the end of the week. Message me if I forget. If you want to try it by yourself. Remember that the X matrix has first a column of 1. After a few manipulations, that gives you the sum of x, or sum of y when you multiply it with the right vector.

+Prosper K Shumba Are you talking about Sum(x.xbar) ? Since x.bar does not change with i, I can take it out of the sum and get xbar*sum(x). And sum(x)=n xbar by definition: from xbar = sum(x)/n

+Help for Economics UofT yes i was talking about Sum(x.xbar). thanks for the explanation. do you have clips on how to conduct the various tests for heteroskedasticity such as the Koenkar, Koenkar-Basset, Glejser etc using excel?

Can you please show us how we can obtain intercept and slope of B0 and B1 after shift line l to l'? Till now I understand but next part I can't solve it

Hmm... the xi are already given. We want to know what beta0 and beta1 are so that ui^^2 is minimized. With the derivative of SSR with respect to beta0 we are basically asking "for which beta0 is SSR minimized?" and the same goes for beta1. Doing the derivative of SSR with respect to xi is the same as asking "for which xi is SSR minimized?" which wouldn't help us at all since the xi are given from our data set (we can't choose a random xi at will). Hope this helps!

Hey Sudip, To understand where the LASSO method comes from, you would have to first study Bayesian statistics. It would take me too long to make all the videos to cover that but there are already a lot of good things about it available on internet !

Ok thanks for your reply, I have an another doubt.For the linear regression model => y_i = beta_0 + summation(x_i,j * beta_j )+ e_j . from here How I will find the values of (Beta_1,Beta_2 .... Beta_j) ?? just help me at least this.

Hi Rishi, with your question, I have no clue what alpha is. (There are about a million methods that can use an alpha hat) Also to prove something you need a provable statement. For instance "Rishi asked a question" is a statement and I can prove it. But I cannot prove just "Rishi". It is the same as asking me to prove "alpha hat". Good luck with your research !

I would advise to get a Tutor or ask a more senior student to help. As much as I would like to, it is impossible for me to answer individual questions like this. Good luck with your study of econometrics !

Because it is based on the law of large numbers (requiring 1/n), so it is a bit different from the covariance based on unbiasedness. But here it doesn't matter much which one you use, both are at 0.

Suppose we estimate a consumption function Yi = α0 + α1Xi + ui, i = 1, ..., n, and a saving function Zi = β0 + β1Xi + vi, i = 1, ..., n, where: • Yi: consumption of individual i • Zi: saving of individual i • Xi: income of individual i Since income is equal to the sum of consumption and savings, Xi = Yi + Zi, ________ What is the relationship between the MCO estimators of α0, α1 and those of β0, β1? b. Is the sum of squares of the residuals the same for the two models? Can the two models be compared in terms of R2? Abrir en Google Traductor

@@yesseniafonttisbeltran457 substitute Xi by Yi + Zi, solve for Zi and Yi, and you have what we call a "Simultaneous equations model". You should find a chapter about that in most econometrics books (or online), since it is a classical problem in econometrics (for supply vs demand). You will need instrumental variables to estimate the coefficients.

If it is not clear, maybe you can be more effective by covering the prerequisites instead of rewatching it. To understand it, you need 2 things: calculus and optimization. Maybe watch some videos about these topics first, then the video should become easy to follow.

i havent seen anyone teaching Econometrics with this ease and grip on the subject ..

Thank you so much for these - not from UofT but watching these tutorials for 2 hours has helped me more than 6 weeks of lectures at my uni!

Hey Nayantara, I am glad it helped you.

I hope it can help as many people as possible. Maybe I should change the name of the channel to remove UofT haha. Actually most of the viewers are not even from Canada.

Bro have an exam tomorrow and you made it super simple to revise...! thank you

Such a great video. We can get so many conclusions from an equation.

you are an absolute legend for posting this. It was so helpful! You organised the video and the results in such an great way the results became iterative. Thank you!

You are really good 😮😮. I can't express myself because I have exams next week and you just simplified it with ease and I also learnt with ease

Thank you so much! Merci infiniment pour votre clarté absolue.

You legend, I hope you're still teaching.

You are an absolute beast. Thanks for your help!

Thank you so much for this, much easier to understand than my lecturer 👍

The best on RUclips!! I rarely comment on RUclips. But for this I have to.

Great! thanks for sharing such remarkable knowledge... May God bless you

Thanks for showing this derivation step by step!

Thank you for taking the time and making this video.

Good explanation. Congratulation sir. Teach me a lot

You teach really well! Thanks a lot!

thank you. :) this is well explained.

This has contributed a lot to my understanding. Thank you

This is so great!! I hope you come back and teach again

Thanks a lot ! (^_^)

this is top tier explanation

Excellent Tutorial.

Merci beaucoup c'était vraiment bien expliqué!

UofT alum, overseas for my masters, thanks for the help!

You're the best of best. Thanks a lot

Good explanation and video!!

CAN'T BELIEVE THIS WAS SO SIMPLE

You are awesome! Thank you for the help

Its a good presentation

thank you from York U!!!

A pleasure to help Toronto Universities Students ;)

@@EconometricsAndAnalytics 6:00 I dont understand how that simplification works, please help!

6:00 I dont understand how that simplification works, please help!

Grim Reaper He is taking the derivative of the equation he had above, so exponent comes down, rewrite equation and the power is what you had before '-1' so in this case it was to the power 2 but now its to the power one. After that you must multiply it by the derivative of the equation inside the brackets, thus giving him (-1). I hope this helps

Thank you for this

Quite helpful. Thank you!

Regards from TU Dortmund.

Thank you so much!!!!

Awesome Tutorial, I'm grateful for your free knowledge sharing.

Can I get the following tutorials?

Please Assist me.

Thank you so much. It's help me a lot...

thank you, really helpful

Thank you thank yo thank you🙈

systematic, Felt real environment, I am an old age student

waw, awesome tutorial. thank you

pure gold

Thank you :)

Pleasure !

Please! Make more! MOREEEE!!!

at 16:38 you write that (xi-Xbar)=Xi uppercase ...why? it should be xi lowercase or the same xi deviation? may you explain?

thanks.

It is not an uppercase, just bad hand writing (-_-;) sorry for the confusion

ok, but it`s not clear yet for me, excuse me...I hope you understand me...then you write at 16:44 ... =SUMXi2...but how can this be able? it is a Xi uppercase times xi lowercase? could you explain please? thanks again

Everything is lowercase

Is the sum of the error term the same as the expected value of the error term, since both equal zero?

My listening skill is not well, please adding the subtitle so that i can understand it more

3.32 you wrote minus in yi=B0 - BXi (with hats) however in picture of graph fitted value is plus yi=B0 + BXi (with hats)????

+Промо Код The trick here is - (B0 + BXi) = - B0 - BXi

Since we have minus y_hat we have to put minuses everywhere (or put parentheses)

Well explained, thank you .

Thanks for these videos. Are there any equivalent lessons for advanced topics also using matrix algebra?

I found there are a lot of existing videos for Matrix Algebra.

Is there any particular topic you were interested in ?

I particularly like this playlist that uses an intuition based approach:

ruclips.net/p/PLZHQObOWTQDPD3MizzM2xVFitgF8hE_ab

Thanks for the reply. The link looks useful. The course I am doing follows M. Verbeek, A Guide to Modern Econometrics. We have started with OLS estimation and moved on to maximum likelihood estimation, methods of moments estimation, and Within and Random Effects Estimation using panel data.

Although I have been taught about OLS estimation before, it has adopted the single observation proofs/derivations, such as this video. However now everything is being taught in vector/matrix notation, which I'm finding a bit confusing.

There is a particular example; I am struggling with seeing how one can easily go from summation notation using vectors to matrix notation, particularly when deriving the OLS estimator.

Thanks again!

Oh, you are doing graduate level econometrics.

I might do a video when I go back to the office at the end of the week. Message me if I forget.

If you want to try it by yourself. Remember that the X matrix has first a column of 1. After a few manipulations, that gives you the sum of x, or sum of y when you multiply it with the right vector.

Help for Economics UofT That would be great, thanks. You're videos are helpful as they go through each step of the algebra, so I would appreciate it.

In the Derivation of OLS Estimators, can i know how you simplify the n?

Thank you soooo muchhh

isn't the sum of expectation to actual values squared your SSE? while SSR is expectation to average

so what's the point of getting u hat = 0, if you could just derive the estimator in the last part of the video

Thank you so much!

how did you come up with nx-bar squared when you multiplied x-bar and x

+Prosper K Shumba

Are you talking about Sum(x.xbar) ?

Since x.bar does not change with i, I can take it out of the sum and get xbar*sum(x).

And sum(x)=n xbar by definition: from xbar = sum(x)/n

+Help for Economics UofT yes i was talking about Sum(x.xbar). thanks for the explanation. do you have clips on how to conduct the various tests for heteroskedasticity such as the Koenkar, Koenkar-Basset, Glejser etc using excel?

I don't, sorry :(

thank you so much for calculating bets in such a esay way.

Why Yi hat does not include ui hat

Can you please show us how we can obtain intercept and slope of B0 and B1 after shift line l to l'? Till now I understand but next part I can't solve it

Why sigma ui hat has been devided by 1/n ?

Could you please tell me after the 9th minute?

Why do you take derivatives with respect to Bo and B1 and not xi?

Hmm... the xi are already given. We want to know what beta0 and beta1 are so that ui^^2 is minimized. With the derivative of SSR with respect to beta0 we are basically asking "for which beta0 is SSR minimized?" and the same goes for beta1.

Doing the derivative of SSR with respect to xi is the same as asking "for which xi is SSR minimized?" which wouldn't help us at all since the xi are given from our data set (we can't choose a random xi at will).

Hope this helps!

thanks a lot

great explanation. can you help me for LASSO model ??

Hey Sudip,

To understand where the LASSO method comes from, you would have to first study Bayesian statistics. It would take me too long to make all the videos to cover that but there are already a lot of good things about it available on internet !

Ok thanks for your reply, I have an another doubt.For the linear regression model =>

y_i = beta_0 + summation(x_i,j * beta_j )+ e_j

. from here How I will find the values of (Beta_1,Beta_2 .... Beta_j) ??

just help me at least this.

ruclips.net/video/OHJXFAPqiVo/видео.html

Thank you so much. (Y)

Hi thanks for the videos! Can you do a video on proving alpha hat and it's relation to gauss Markov when looking at alpha tilda star ☺️☺️

Hi Rishi, with your question, I have no clue what alpha is. (There are about a million methods that can use an alpha hat)

Also to prove something you need a provable statement.

For instance "Rishi asked a question" is a statement and I can prove it.

But I cannot prove just "Rishi". It is the same as asking me to prove "alpha hat".

Good luck with your research !

Help for Economics UofT is there any way I could send you the question sheet, it's very difficult for me to express it on RUclips

I would advise to get a Tutor or ask a more senior student to help.

As much as I would like to, it is impossible for me to answer individual questions like this.

Good luck with your study of econometrics !

@@EconometricsAndAnalytics please respond

thank u soo much

Thank you :,)

Do you have videos regrading matrix derivations of OLS for time series?

I don't have videos for derivations in matrix form, nor for time series, sorry. :(

Would help if you do graduate level econometrics

Why use n not n-1, it’s sample Can somebody explain

Because it is based on the law of large numbers (requiring 1/n), so it is a bit different from the covariance based on unbiasedness.

But here it doesn't matter much which one you use, both are at 0.

Thank you!!

Can you tell me between 9 and 17 minutes please

implications of first order condition - sum of error terms is zero, and covariance between error terms and x terms is zero.

i need you :(

Here is the motivational support:

Dont give up! You can definitely do it!

@@EconometricsAndAnalytics

How can I know the relationship between 2 estimators

Suppose we estimate a consumption function

Yi = α0 + α1Xi + ui, i = 1, ..., n,

and a saving function

Zi = β0 + β1Xi + vi, i = 1, ..., n,

where: • Yi: consumption of individual i

• Zi: saving of individual i

• Xi: income of individual i

Since income is equal to the sum of consumption and savings, Xi = Yi + Zi,

________

What is the relationship between the MCO estimators of α0, α1 and those of β0, β1? b. Is the sum of squares of the residuals the same for the two models?

Can the two models be compared in terms of R2?

Abrir en Google Traductor

@@yesseniafonttisbeltran457 substitute Xi by Yi + Zi, solve for Zi and Yi, and you have what we call a "Simultaneous equations model".

You should find a chapter about that in most econometrics books (or online), since it is a classical problem in econometrics (for supply vs demand). You will need instrumental variables to estimate the coefficients.

@@EconometricsAndAnalytics thank you very much

I still don't get it I guess I'll watch it 10 more times :(

If it is not clear, maybe you can be more effective by covering the prerequisites instead of rewatching it.

To understand it, you need 2 things: calculus and optimization.

Maybe watch some videos about these topics first, then the video should become easy to follow.

@@RemiDav Ok thank you

"Basically" in English means "more or less", so I wouldn't use it if something is exact

Thanks a lot