(EViews10): Heteroskedasticity and Weighted (Generalised) Least Squares

HTML-код

- Опубликовано: 7 сен 2024

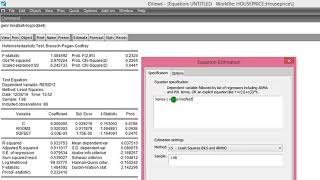

- @CrunchEconometrix This video explains how to correct heteroscedasticity with weighted (generalised) least squares. Coined from the Greek word hetero (which means different or unequal), and skedastic (which means spread or scatter). So, homoskedasticity means equal spread, and heteroskedasticity, on the other hand, means unequal spread. The measure of spread is the variance, hence, heteroskedasticity deals with unequal variances. Heteroskedasticity or heteroscedasticity is the same. Only be consistent. Yes! The longest word in the econometrics dictionary with 18 words. One of the assumptions of ordinary least squares (OLS) is that the model must be homoskedastic. Needed to justify the usual t tests, F tests, and confidence intervals for OLS estimation of the linear regression model, even in large samples. In general, heteroskedasticity is more likely to occur in cross-sectional analysis. This does not imply that heteroskedasticity in time series models is impossible. What are the causes of heteroskedasticity? (1) Poor data sampling method may lead to heteroskedasticity particularly when collecting primary data. (2) Wrong data transformation. For instance, over-differencing a variable may lead to heteroskedasticity. (3) Wrong model specification. Related to the functional form: log-log, log-level, and level-level models. (4) The presence of outliers can lead to your model becoming heteroskedastic. Bogus figures that stands out. Very obvious to the prying eyes. (5) Skewness of one or more regressors (closely related to outliers being evident in the data). Consequences of heteroskedasticity: (1) OLS estimators, β ̂_OLS are still linear, unbiased and consistent. Hence the regression estimates remain unbiased and consistent. (2) But the estimators, β ̂_OLS are inefficient (that is, not having minimum variance) in the class of minimum variance estimators. (3) Therefore, OLS is no longer BLUE (Best Linear Unbiased Estimator). (4) Such that regression predictors (estimates) are also inefficient, though consistent. (5) Implies that the regression estimates cannot be used to construct confidence intervals, or used for inferences. (6) Affects the variances (and standard errors) of the estimated β ̂_S. (7) OLS method under-estimates the variances (and standard errors). (8) Yields low standard errors (9) Leads to higher than expected values of t and F statistics. (10) Yields statistically significant coefficients. (11) Rejection of the null hypothesis too often (12) Causes Type I error. (13) Both the t and the F statistics are no longer reliable any more for hypothesis testing. Some heteroskedasticity tests are: Breusch-Pagan LM Test; Glesjer LM Test; Harvey-Godfrey LM Test; Park LM Test; Goldfeld-Quandt Test; White’s Test; Engle’s ARCH Test; and Koenker-Basset Test. Heteroskedasticity can be resolved by: (1) Functional Forms; (2) Generalised (Weighted) Least Squares (GLS/WLS); and (3) White’s Robust-Standard Errors. How to detect heteroskedasticity? The truth is that there is no hard and fast rule for detecting heteroskedasticity. Therefore, more often than not, heteroskedasticity may be a case of educated guesswork, prior empirical experiences or mere speculation. However, informal and formal approaches can be used in detecting the presence of heteroskedasticity such as: Informal approach: Plotting the residuals from the regression against the estimated dependent variable

Formal approach: Perform econometric tests. There are several tests of heteroskedasticity, each based on certain assumptions. The interested reader may want to consult the references listed at the end of the video.

Link to A&H_hprice.xlsx data (free) and dofile (Subject to payment) cruncheconomet...

Note: You have to CART and CHECKOUT.

References and Readings: Asteriou and Hall (2016) Applied Econometrics, 3ed; Wooldridge, J. M. (1995). Econometric Analysis of Cross Section and Panel Data. London, England: The MIT Press, Cambridge, Massachusetts; Baltagi, B.H. (1995) Econometric Analysis of Panel Data. New York, NY: John Wiley and Sons; Hsiao, C. (1986) Analysis of Panel Data, Econometric Society Monographs No. 11. Cambridge, United Kingdom: Cambridge University Press; Gujarati and Porter (2009) Basic Econometrics, International Edition; John, F. (1997) Applied Regression Analysis, Linear Models, and Related Methods, Sage Publications, California, p. 306; Mankiw, GN. (1990) “A Quick Refresher Course in Macroeconomics,” Journal of Economic Literature, Vol. XXVIII, p. 1648

Follow up with soft-notes and updates from CrunchEconometrix:

Playlists: / cruncheconometrix

Website: cruncheconomet...

Blog: cruncheconomet...

Facebook: / cruncheconometrix

RUclips Custom URL: / cruncheconometrix

Twitter: / crunchmetrix

Reddit: / crunchmetrix

I want to appreciate all my subscribers from across the globe (Africa, Asia, Europe, the Middle East, The Americas, and The Pacific). Thank you all for your support. I am encouraged by your comments, questions, likes and critiques. They keep me focussed and poised to do better. I will continue to contribute my little quota such that every student and researcher will independently analyse his/her data. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Please do not keep me to yourself (lol) inform your friends, students and academic networks about my Channel. Tell them CrunchEconometrix breaks down the econometric jargons and teaches with simplicity. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

Thank you for these videos. I am currently working on my dissertation, and they have been very helpful. I realise this does not apply with panel dataset. How do I remove serial correlation and heteroskedasticity from my panel models?

@@oluwaseunmuraina9637 Better to estimate your panel data with techniques that correct for those.

@@CrunchEconometrix Many thanks for your response. Which techniques are appropriate? Do you mean the Fixed/random effect models?

@@oluwaseunmuraina9637 Yes, use the robust option. GMM works well too.

Thank you so much for your teaching

U're welcome 🙏

your lectures are very helful, I sincerely appreciate you.

Hi Om, thanks for the encouraging feedback. Deeply appreciated.

thanks a lot

You are most welcome, Sir 😊

This is great and I can relate with the explanation

This is very helpful.

Thanks for the positive feedback, Leah!!!

👍 I suggest if you can run this exercise in Stata.. However to a beginner in facing with hetrosckedacity it's appreciable to get an good understanding how to deal with this. 🙏

Wow, Mahesh. Thanks😊

Thank Youu ❣️

You’re welcome, Christine 😊!

Wow thank you I am thankful

From Germany

You are welcome!🥰

Thank you, this is so helpful!

Thanks Bernadette, for the encouraging words and feedback. Deeply appreciated! Please may I know from where (location) you are reaching me?

CrunchEconometrix I am doing a masters in econometrics and without your channel i wouldn’t have survived. it is the best. I follow you from Panama !!!

May I ask you to please explain the Engel Granger test ? I had a hard time finding an explanation for cointegration uning this test. Thank you again ! 💓

Sorry girl, I don't use E-G :) never used it.

plz, exercise white test about panel data to deduct heteroskedasticity, by equation manually

Hi Waqas, if that is computed by the software why do same manually?

That's what i was looking for, i did the same for my panel data just changed into fixed effect model and choose the cross section weights. Should i have to test the Heteroskedasticity again? coz i did not find how.... i keep one receiving (Procedure unavailable for equations estimated with iterated weights) thanx in advanced.

It should work with pooled data.

I wander does it has constant variance after weighted dependent data? could we consider its as classic linear model after weighted both denpendent data and independent data,?

Hi Bianca, the "weight" corrects for heteroscedasticity.

Did you use the panel data? or Cross section? I used a panel data, but I don't know how to solve heteroskedasticity. I tried transformation using inverse log and also natural log, yet It doesn't solve the heteroskedasticity problem.

Hi Muhd, I used cross-sectional data.

Thanks for your video. Can we plot residuals against a variable that does not enter into the regression model to judge the existence of heterodasticity?

Hi Xinru, I am not sure how that approach will test for heteroscedasticity.

@@CrunchEconometrix Okay. Thanks for your clear reply!:):):)

can i estimate garch model or heteroscedasticity by GLS If i have one variable ( index of stocks ) and how??

Using GARCH or GLS will depend on your study objective(s).

Thanks for your video. I resolved many problems about my panel. So thank you for your work.

I have a question. Is there a video in which you show us GLS regression in STATA? I saw a video about gls regression in eviews but not in stata.

Thank you for your time.

This video explains your query.

Is it possible with Panel data? I am trying but I couldn’t

It should work with pooled data.

Thank you very much. I would like to ask a question: what does d.f. Adjustment do? What if we uncheck that option in OLS regression? Will our results still be valid? Thank you beforehand.

Hi Ibrahim, thanks for the encouraging feedback. Deeply appreciated! I have never really investigated that. Why not try it out and compare your results?

What if I only have a single regressor and it is already in the log form and there is still heteroskedasticity. How do i remove it?

Use the robust option.

Maam can you help regarding estimations of markov switching model

Hi Asma, no idea at the moment. But I have noted your suggestion. I will find the time to learn it then create easy-to-understand videos.

@@CrunchEconometrix

Thanks maam now I learn it maam thanks alot

i tried all methods but always there is heteroskedasticity with p (0.000) normality too (0.000) correlation too (0.000) . Ps : i have 9 independent variables with 1300 observations for each one . pls help me what i have to do ??

Hi Ahmed, are you using cross-sectional data?

time series data : bitcoin ethereum gold oil ....

@@ahmedtrabelsi3589 I guess they are high-frequency variables. Besides, having 9 of such is too much. One or more could be driving heteroskedasticity.

@@ahmedtrabelsi3589 I would just like to please know how you were able to solve this issue as I am experiencing similar?

What issue?