Hi Bionic Turtle, just wanted to let you know that I'm a derivatives trader and first thing they made me do was trying to valuate a IRS on my own without Bloomberg or any calculator and this has come super handy. Thanks for all your effort.

thats very helpful but what rates do i use in reality? i am working on a loan that has been swapped with 3m euribor payments. it runs until september 2024... there are no libor or euribor spot rates for that maturity. pls help

Hi, great stuff thank you very much. One thing i always wondered how it worked in practice as opposed to in theory is the yield curve and interest rates to use. How a swap works in theory is completely clear to me (i got my CFA charter in February so that helps haha). I work in real estate and i was given the task to value a swap that is hedging a variable rate loan on a property. the floating payer pays 3M EURIBOR, while the fixed payer pays 0,208% with a maturity to 30th Sept 2024. And that is where it gets unclear to me. EURIBOR curve does not extend until that maturity, since max maturity is 12M. so i got 1M, 3M, 6M and 12M EURIBOR. So the EURIBOR forward curve determines the future floating payments, so far so good. but what rate do i use to discount those future payments? i cant use forward rates to discount and i have no spot rates above 12M. pls help and sorry for the long message! cheers all the best

Were did you get the Libor curve, and how much interest rate was at prior 6mo? My bloomberg searches leads me to a curve with max 1y rate, could I get the GOVT bonds yield curve for that? Thanks a lot

we have a support forum at www.bionicturtle.com/forum where you can probably get some help (including I monitor it daily). Specifically, in the free forum, swaps are discussed in P1.T3 Financial Markets & Products at www.bionicturtle.com/forum/forums/p1-t3-financial-markets-products-30.6/

Hull calls it "valuation in terms of bond prices." I don't think it would be called a zero-coupon method because you are treating the swap as two coupon-bearing bonds (one fixed and one floating) where the coupons are netted at each cash flow settlement date

Thanks a lot for the amazing content! In row 14, I think you are calculating the forward rates p.a not s.a. That's why you are again dividing them by 2 when computing the floating CFs. So the "s.a" written in brackets in row 14 are confusing.

Hi Bionic Turtle, just wanted to let you know that I'm a derivatives trader and first thing they made me do was trying to valuate a IRS on my own without Bloomberg or any calculator and this has come super handy.

Thanks for all your effort.

THE EXCEL SHEET IS NOT AVAILABLE , can you provide that, thanks a lot for this great effort

you saved my life. much love

thats very helpful but what rates do i use in reality? i am working on a loan that has been swapped with 3m euribor payments. it runs until september 2024... there are no libor or euribor spot rates for that maturity. pls help

Excellent video.

Thank you for watching!

great stuff! thank you

Hi, can you link the video or explain how to get the future rates from the spot rates??

Thanks for the awesome video... really helped!

Why dont use boostraping for calculating forward rates?

Hi,

great stuff thank you very much. One thing i always wondered how it worked in practice as opposed to in theory is the yield curve and interest rates to use. How a swap works in theory is completely clear to me (i got my CFA charter in February so that helps haha). I work in real estate and i was given the task to value a swap that is hedging a variable rate loan on a property. the floating payer pays 3M EURIBOR, while the fixed payer pays 0,208% with a maturity to 30th Sept 2024. And that is where it gets unclear to me. EURIBOR curve does not extend until that maturity, since max maturity is 12M. so i got 1M, 3M, 6M and 12M EURIBOR. So the EURIBOR forward curve determines the future floating payments, so far so good. but what rate do i use to discount those future payments? i cant use forward rates to discount and i have no spot rates above 12M. pls help and sorry for the long message! cheers all the best

could you rollover at the end of 12 M?

Your contents are amazing! Thank you for sharing these!

Were did you get the Libor curve, and how much interest rate was at prior 6mo? My bloomberg searches leads me to a curve with max 1y rate, could I get the GOVT bonds yield curve for that? Thanks a lot

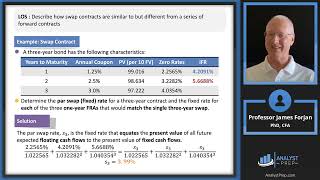

this is illustrates Hull example 7-1 (see label) so the libor curve is entirely fictional-illustrative

@@bionicturtle Ah ok. But if I would get the real rates, could I get the govt Yield curve?

@@PedroJardo yes of course, you could really use any rates (it's a function of the swap obviously)

Hello. I need some help on basic swap problems. Is there a way for you to take a glimpse at those?

we have a support forum at www.bionicturtle.com/forum where you can probably get some help (including I monitor it daily). Specifically, in the free forum, swaps are discussed in P1.T3 Financial Markets & Products at www.bionicturtle.com/forum/forums/p1-t3-financial-markets-products-30.6/

Is the second method in this video a zero coupon valuation method?

Hull calls it "valuation in terms of bond prices." I don't think it would be called a zero-coupon method because you are treating the swap as two coupon-bearing bonds (one fixed and one floating) where the coupons are netted at each cash flow settlement date

If you had this swap but had to value it using a 'zero coupon valuation method' how would you go about doing this?@@bionicturtle

The discount factor based on which rate?

based on e ^ (-t * LIBOR at t)

Could you please share the excel file ?

As I almost always provide, a link to the XLS is found ABOVE in the video's description; ie, "[ here is my XLS trtl.bz/2Q4XFCh ]"

Thanks a lot for the amazing content!

In row 14, I think you are calculating the forward rates p.a not s.a. That's why you are again dividing them by 2 when computing the floating CFs. So the "s.a" written in brackets in row 14 are confusing.

thank you sir!

Your contents are amazing! Thank you for sharing these!