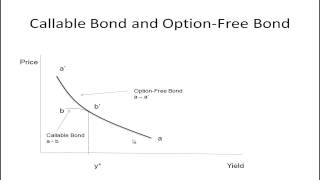

Thanks for your feedback. On rechecking, I notice that there is no mistake and the formula is correct. For more information, refer to: Introduction to Cashflow Analysis., Robert J. Donohue CCIM, Regent School Press, ISBN 978-1-886654-09-9

at 3:30 how can we assume 1/(1+Y) approximates 1? You stated that for small changes in Y, this holds. But the above expression is Y, not delta Y. I'm confused.

Aw by the way... In my teacher's notes the function for convexity was exactly the same as yours but he also divided it by 2. Basically every function of his was 0.5*(convexity function in this video) ...could you explain why would he do that?

![YoungBoy Never Broke Again - Catch Me [Official Video]](http://i.ytimg.com/vi/KxwEXXFQMTY/mqdefault.jpg)

![ATEEZ(에이티즈) - [GOLDEN HOUR : Part.2] Preview](http://i.ytimg.com/vi/X4PfgRPBUVo/mqdefault.jpg)

Thanks for your feedback. On rechecking, I notice that there is no mistake and the formula is correct. For more information, refer to:

Introduction to Cashflow Analysis., Robert J. Donohue CCIM, Regent School Press,

ISBN 978-1-886654-09-9

convexity is the second derivative. just derive from the first one ... clear explanation here!

Great video. It's very easy to understand. Thank you very much!

Thank you Sir.. A big thank you for explaining it so lucidly...from India

at 3:30 how can we assume 1/(1+Y) approximates 1? You stated that for small changes in Y, this holds. But the above expression is Y, not delta Y. I'm confused.

it's not change in yield correct, i guess it's a simplifying assumption and thats why in textbooks they mention duration is approximately equal to..

This really helps. Thanks a bunch.

excellent exposition!

Thank you, very intuitive now!

you are the boss!

Excellent! Thanks.

Thank you Sir

Aw by the way...

In my teacher's notes the function for convexity was exactly the same as yours but he also divided it by 2.

Basically every function of his was 0.5*(convexity function in this video)

...could you explain why would he do that?

probably because he assumed semi annual compounding.

Nice