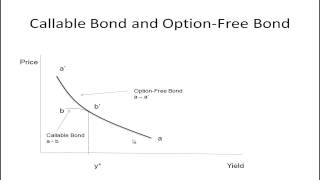

Thank you! Yes, in the case of a callable bond, when interest rates become low enough, the curve becomes concave and that makes the convexity adjustment negative.

Hello Sir Should your videos enough to get concepts cleared ? or better to opt as member. I'm located currently in UAE and can't join as nothing appear when press join button.

@@letmeexplaincfa oh I was asking out of desperation a general question on cfa content - I really do not get why convexity gets converted from 0.25 to 25 when you calculate approximate price change percentage. Any help to let me explain would be greatly appreciated

Extremely well explained and I understood it completely. Thanks a lot.

Thanks a lot for the simple yet clear explanation!!

You are very welcome :)

Love the presentation and explanation, I subbed

Thanks 🙏

Thank you! Clear as usual :)

You’re welcome!

Thank you for this !

You’re very welcome👍

Thank you so much sir !

So well explained.

Thank you so much!

Thank you for the great explanation

You are very welcome!

Great work

🙏

You’re amazing 👌🏼

Thank you!

Thank you for your amazing work! Please correct me if I'm wrong - the convexity adjustment could also be negative for a callable bond, right?

Thank you! Yes, in the case of a callable bond, when interest rates become low enough, the curve becomes concave and that makes the convexity adjustment negative.

Hello Sir

Should your videos enough to get concepts cleared ? or better to opt as member. I'm located currently in UAE and can't join as nothing appear when press join button.

Are you viewing from a computer? The UAE is on the list of eligible countries. I certainly recommend you join as a member.

@@letmeexplaincfa

I'm trying from mobile , alright will check from computer

how to join membership pls?

Please look for the Join button when viewing from a computer

Why when convexity is 0.25 do we have to convert it to 25. How did it get converted to 25?This is for credit risk section regarding price change

25 basis points is the change in yield, giving 0.0025 expressed in decimal format. I don't thing I made any conversions to the convexity measure.

@@letmeexplaincfa oh I was asking out of desperation a general question on cfa content - I really do not get why convexity gets converted from 0.25 to 25 when you calculate approximate price change percentage. Any help to let me explain would be greatly appreciated