In the video, I said I would explain how I solved for the amount that should be invested in the short-term bond in order to achieve a duration with the barbell portfolio that matches the duration of the bullet portfolio. The key is to match dollar durations because if the dollar durations match, then the durations match (given the investment dollars are the same). Dollar duration equals investment multiplied by modified duration; that is, let D = modified duration and let V = value of dollars invested, such that DV = dollar duration. Further, define S = duration of short-term bond; M = duration of (bullet) medium-term bond; and L = duration of long-term bond. The dollar duration, then, of the bullet portfolio is simply V*M or, in my example, 63.763*15 = 956.44 million. The dollar duration of the barbell portfolio is given by S*V(small) + L*V(large), where V(small) and V(large) are the respective dollar investments. However, we require that V(small) + V(large) = V, and V(large) = V - V(small) such that the dollar duration of the barbell is given by S*V(small) + L*[V - V(small)]. Then the equality is given by: S*V(small) + L*[V - V(small)] = M*V --> S*V(small) + L*V - L*V(small)] = M*V --> V(small)*(S-L) + L*V = M*V --> V(small)*(S-L) = M*V - L*V --> V(small) = (M*V - L*V)/(S-L). In my example, S = 5.0, M = 15.0 and L = 30.0 such that V(small) = (15.0*V - 30*V)/(5.0 - 30.0) is the solution for V(small) as a function of V. In this case, V(small) = (15.0*63.763 - 30*63.763)/(5.0 - 30.0) = 38.26 million to the 5-year bond and the remaining 25.51 to the 30-year bond which turns out to be 60/40%. Thanks!

I have a question. In the example Tuckman table 4.7 the medium bond with 9.5 years to maturity. The yield is greater than a coupon for that bond, should we expect that the price should be below 100 (below face value)"? I understand that it might happen, but in theory it should be less than 100? Or there is some other condition in this exercise that could explain such situation?

Thanks again for this useful video. Can you please help me understand that, by price of Barbel portfolio would be lower, we mean although cost of portfolio would be 63, the portfolio would be marked at Lower price? Thanks in advance

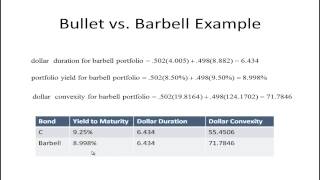

Hi Sunil, I just showed how the YIELD of the barbell will be LESS THAN the yield of the duration-matched bullet (both invest the same capital, so their initial values are the same). This is why no free lunch: the barbell's higher convexity (compared to the bullet) implies greater gain/smaller loss under big yield changes, but it has a lower YIELD at the INITIAL rate. The idea is that, if rates are constant (or move only a little) the bullet will outperform, consistent with its higher yield; but if rates are volatile, then the barbell will outperform. Thanks,

@@bionicturtle For bonds with different maturities if bond yields in the portfolio are not equal to each other we cannot just take weighted average of their yields to receive the portfolio yield. It can be easily checked for barbell portfolio in the example. It is necessary for portfolio yield y= 3.63% to fulfill the equation 38.26*exp(2%*5)exp(-y*5)+25.51*exp(4%*30)*exp(-y*30)=63.763 And in this particular case there is a free lunch.

@@kannushi Yes, excellent point! As I was following Tuckman's approach, I was using the WEIGHTED (average) yield, which is not the portfolio's yield. I agree with your calculation of the portfolio's yield to maturity (aka, IRR).

In the video, I said I would explain how I solved for the amount that should be invested in the short-term bond in order to achieve a duration with the barbell portfolio that matches the duration of the bullet portfolio. The key is to match dollar durations because if the dollar durations match, then the durations match (given the investment dollars are the same). Dollar duration equals investment multiplied by modified duration; that is, let D = modified duration and let V = value of dollars invested, such that DV = dollar duration. Further, define S = duration of short-term bond; M = duration of (bullet) medium-term bond; and L = duration of long-term bond. The dollar duration, then, of the bullet portfolio is simply V*M or, in my example, 63.763*15 = 956.44 million. The dollar duration of the barbell portfolio is given by S*V(small) + L*V(large), where V(small) and V(large) are the respective dollar investments. However, we require that V(small) + V(large) = V, and V(large) = V - V(small) such that the dollar duration of the barbell is given by S*V(small) + L*[V - V(small)]. Then the equality is given by: S*V(small) + L*[V - V(small)] = M*V --> S*V(small) + L*V - L*V(small)] = M*V --> V(small)*(S-L) + L*V = M*V --> V(small)*(S-L) = M*V - L*V --> V(small) = (M*V - L*V)/(S-L). In my example, S = 5.0, M = 15.0 and L = 30.0 such that V(small) = (15.0*V - 30*V)/(5.0 - 30.0) is the solution for V(small) as a function of V. In this case, V(small) = (15.0*63.763 - 30*63.763)/(5.0 - 30.0) = 38.26 million to the 5-year bond and the remaining 25.51 to the 30-year bond which turns out to be 60/40%. Thanks!

I thought a barbell portfolio was adding more weights on the short end and long end?

I have a question. In the example Tuckman table 4.7 the medium bond with 9.5 years to maturity. The yield is greater than a coupon for that bond, should we expect that the price should be below 100 (below face value)"? I understand that it might happen, but in theory it should be less than 100? Or there is some other condition in this exercise that could explain such situation?

Thanks again for this useful video.

Can you please help me understand that, by price of Barbel portfolio would be lower, we mean although cost of portfolio would be 63, the portfolio would be marked at Lower price?

Thanks in advance

Hi Sunil, I just showed how the YIELD of the barbell will be LESS THAN the yield of the duration-matched bullet (both invest the same capital, so their initial values are the same). This is why no free lunch: the barbell's higher convexity (compared to the bullet) implies greater gain/smaller loss under big yield changes, but it has a lower YIELD at the INITIAL rate. The idea is that, if rates are constant (or move only a little) the bullet will outperform, consistent with its higher yield; but if rates are volatile, then the barbell will outperform. Thanks,

@@bionicturtle Got it.. Thank you Sir

@@bionicturtle For bonds with different maturities if bond yields in the portfolio are not equal to each other we cannot just take weighted average of their yields to receive the portfolio yield. It can be easily checked for barbell portfolio in the example. It is necessary for portfolio yield y= 3.63% to fulfill the equation 38.26*exp(2%*5)exp(-y*5)+25.51*exp(4%*30)*exp(-y*30)=63.763 And in this particular case there is a free lunch.

@@kannushi Yes, excellent point! As I was following Tuckman's approach, I was using the WEIGHTED (average) yield, which is not the portfolio's yield. I agree with your calculation of the portfolio's yield to maturity (aka, IRR).