Hey @JKMath , it's a small request, I'd really appreciate if you could do some videos for Sinking Funds too. Your videos are really comprehensive and easily understandable :)

Thanks for the suggestion! I will add it to my list of topics for potential "one-off" FM videos to make one day, similar to the Drop vs Balloon payment video in my FM playlist. I appreciate the kind feedback!

I don't currently have any plans to cover the actuary Exam P. However, at some point in the future I do plan on making videos for a general probability and statistics course, which should have some overlapping topics with Exam P.

This video was very helpful, but I am still kind of confused about premiums and discounts. Correct me if I am wrong on any of these. What perspective should I view this as? The bond issuer or the bond investor? Would the discount and premium be beneficial or unbeneficial for either party? and what does the yield rate actually do in terms of this? Does the yield rate calculate the interest being paid per coupon? And would the "r" rate just to calculate the "base" value of a coupon per period?

In general we view theses problems from the perspective of the bond investor, but the terminology of discount/premium does not change depending on the perspective. A bond bought at a discount always has a yield rate greater than the coupon rate, and a bond bought at a premium always has a yield rate less than the coupon rate. In terms of who benefits, this really depends on when the bond is "called," which is where callable bonds come into play. I explain this in detail in lesson 24, so I would recommend you watch that as well. However the general idea is this: If the bond is to be bought at a premium, the investor will want to "call" or redeem the bond at the earliest date possible in order to pay the lowest price. But if the bond is to be bought at a discount, the investor will want to redeem the bond at the latest date possible in order to pay the lowest price. In both cases, the investor will benefit if the bond is redeemed at the right time. However, if the bond is not callable, a discounted bond will always benefit the investor (lower price paid), and a premium bond will benefit the issuer (higher price paid for investor).

In regards to what the yield rate and coupon rate actually are/ what they do: The coupon rate is a fixed rate that is agreed upon between the issuer and buyer. It determines the value of the payments the investor will receive. This rate will not change for the duration of the bond. The investor is guaranteed to be paid the coupons whose value is determined by that rate. The yield rate on the other hand determines the present value of the stream of coupons and redemption amount, and is subject to change based on current financial market conditions. It is my understanding that once a bond is purchased, this yield rate is set for the duration of the bond, however if the investor waits on purchasing the bond until the yield rate is more desirable (in comparison to coupon rate for a premium/discount), then the yield rate would be different. The issuer has no control over the yield rate since it is determined by the market conditions, it is up to the investor to decide when they should purchase a bond based on the yield and coupon rates in order for it benefit them. And so in these problems for the exam, we are already told what the yield rate is when the investor purchases the bond. It has already been decided. That is why the yield rate does not change in most problems. Hope this all helps!

I have always had trouble understanding the "price" of a bond. The price is the present value of how much the borrower is paying back to the lender, hence the formula seems to make a lot of sense. However, if an investor buys a bond (i.e. they are the lender), then the amount the investor invests is the face value of the bond, is it not? Because that is how much they are paying (loaning) at time zero. But for some reason, in the fm exam practice questions, the amount invested in the bond is equal to the price of the bond, which I find confusing. Please clarify?

Are you referring to the face value vs the redemption amount? I am not sure I entirely understand your questions, but I'll say this: It is often assumed in FM problems that the face value is the same as the redemption amount, even if that is super unlikely in a realistic scenario, as it makes for easier problems and calculations. There are some problems where the face value and redemption amount differ, but they are uncommon. When it does happen though, the problem will be sure to make a note of it. A lot of the times for concepts in fm, the focus is on more theoretical examples than practical examples, so even if something doesn't make sense realistically, it doesn't mean that we can't do it theoretically with math. Hope this helps!

For the coupons, does the NPV account for the FV of all of the coupons being paid at different times? To me it seems like you only discounted the $1000 lump sum at the end appropriately

Yes, when you multiply the $ amount of the coupons by the PV annuity-immediate notation, that accounts for the PV of the coupons paid at the different times (As long as you use the correct value for the number of coupons and the appropriate yield rate). Remember that the PV annuity notation represents a formula that calculates the present value of a series of payments (of equal amount) taking each of their times into account. Hope this helps!

I'm not entirely sure I understand your question. Can you provide more details on the problem/question you are trying to solve? I would love to help you and give you an answer, but I need a little bit more information. Let me know!

A loan at 8% annually has an initial payment of 1,000, and 9 further payments. The payment amount decreases by 2% each year. Find the loan balance immediately after the third payment.@@JKMath for example

For this type of problem I believe my lesson video on Amortization may be of some help. The procedure is very similar, although my video does the focus on level payment loans, you can still apply it to a loan with decreasing payments (just can't use certain formulas I show you in the video). So feel free to check out... but here is the basic idea of how you would solve your problem: To find the loan balance after the third payment, you need to subtract out the amount paid on the loan 3 years in, considering the interest that would be accumulated during that time. First you need the initial loan amount which would be the PV of the 10 payments of the decreasing geometric annuity. You can calculate that yourself (you may need to reference my video one esoteric annuities), but lets just represent the PV with L for this comment. Next you want to calculate the interest in the first year, so take L times the interest rate: L*.08. Subtract that amount from the first payment, so 1000 - L*.08. This will give you how much of the loan you actually pay off in the first year (the amount of the payment minus the interest accrued for the year). Then subtract this from the loan balance, and start the process over for year 2/the second payment. Take the new loan balance and multiply by .08. Then subtract that from the amount of the second payment (which is 1000(1-.02) since each payment decreases by 2%). Then subtract the result from the loan balance. You would then repeat this process again for the third payment, of which then you would be done for that example. Does this help? Let me know!

⬇Download my FREE worksheet set for all my Financial Mathematics videos!

www.jkmathematics.com/financial-mathematics-worksheet-set

Hey @JKMath , it's a small request, I'd really appreciate if you could do some videos for Sinking Funds too. Your videos are really comprehensive and easily understandable :)

Thanks for the suggestion! I will add it to my list of topics for potential "one-off" FM videos to make one day, similar to the Drop vs Balloon payment video in my FM playlist. I appreciate the kind feedback!

You are such a kind person🥰🥰. Thank you so much for making these videos. Truly Appreciate it🙏

You're very welcome! :)

thankyou for your video and explanation, i really really like it and appreciate it so muchhh ❤

Dear Josh, thank you for your painstaking efforts in making these tutorials. Really appreciate the content.

You are very welcome!! Thank you for your generosity, it is much appreciated! I will continue to make the best videos I can :)

thank you This video was very helpful

You’re welcome! Glad to help :)

@@JKMath when will you be sharing Exam P tutorials

I don't currently have any plans to cover the actuary Exam P. However, at some point in the future I do plan on making videos for a general probability and statistics course, which should have some overlapping topics with Exam P.

@@JKMath ook i understand

Tgnk you for theese videos are really helpful❤😊

You're welcome! Glad they are helpful for you :)

thank you! You explain really well

Glad you found it helpful! :)

This video was very helpful, but I am still kind of confused about premiums and discounts. Correct me if I am wrong on any of these. What perspective should I view this as? The bond issuer or the bond investor? Would the discount and premium be beneficial or unbeneficial for either party? and what does the yield rate actually do in terms of this? Does the yield rate calculate the interest being paid per coupon? And would the "r" rate just to calculate the "base" value of a coupon per period?

In general we view theses problems from the perspective of the bond investor, but the terminology of discount/premium does not change depending on the perspective. A bond bought at a discount always has a yield rate greater than the coupon rate, and a bond bought at a premium always has a yield rate less than the coupon rate. In terms of who benefits, this really depends on when the bond is "called," which is where callable bonds come into play. I explain this in detail in lesson 24, so I would recommend you watch that as well. However the general idea is this: If the bond is to be bought at a premium, the investor will want to "call" or redeem the bond at the earliest date possible in order to pay the lowest price. But if the bond is to be bought at a discount, the investor will want to redeem the bond at the latest date possible in order to pay the lowest price. In both cases, the investor will benefit if the bond is redeemed at the right time. However, if the bond is not callable, a discounted bond will always benefit the investor (lower price paid), and a premium bond will benefit the issuer (higher price paid for investor).

In regards to what the yield rate and coupon rate actually are/ what they do: The coupon rate is a fixed rate that is agreed upon between the issuer and buyer. It determines the value of the payments the investor will receive. This rate will not change for the duration of the bond. The investor is guaranteed to be paid the coupons whose value is determined by that rate. The yield rate on the other hand determines the present value of the stream of coupons and redemption amount, and is subject to change based on current financial market conditions. It is my understanding that once a bond is purchased, this yield rate is set for the duration of the bond, however if the investor waits on purchasing the bond until the yield rate is more desirable (in comparison to coupon rate for a premium/discount), then the yield rate would be different. The issuer has no control over the yield rate since it is determined by the market conditions, it is up to the investor to decide when they should purchase a bond based on the yield and coupon rates in order for it benefit them. And so in these problems for the exam, we are already told what the yield rate is when the investor purchases the bond. It has already been decided. That is why the yield rate does not change in most problems. Hope this all helps!

@@JKMath Omg thank you. That cleared everything up!! Thank you for ur detailed response and time!!

Awesome! Glad to help :)

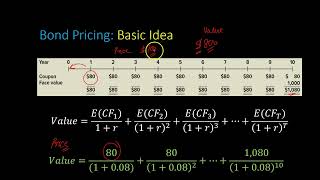

I have always had trouble understanding the "price" of a bond. The price is the present value of how much the borrower is paying back to the lender, hence the formula seems to make a lot of sense. However, if an investor buys a bond (i.e. they are the lender), then the amount the investor invests is the face value of the bond, is it not? Because that is how much they are paying (loaning) at time zero. But for some reason, in the fm exam practice questions, the amount invested in the bond is equal to the price of the bond, which I find confusing. Please clarify?

Are you referring to the face value vs the redemption amount? I am not sure I entirely understand your questions, but I'll say this: It is often assumed in FM problems that the face value is the same as the redemption amount, even if that is super unlikely in a realistic scenario, as it makes for easier problems and calculations. There are some problems where the face value and redemption amount differ, but they are uncommon. When it does happen though, the problem will be sure to make a note of it.

A lot of the times for concepts in fm, the focus is on more theoretical examples than practical examples, so even if something doesn't make sense realistically, it doesn't mean that we can't do it theoretically with math. Hope this helps!

For the coupons, does the NPV account for the FV of all of the coupons being paid at different times? To me it seems like you only discounted the $1000 lump sum at the end appropriately

Yes, when you multiply the $ amount of the coupons by the PV annuity-immediate notation, that accounts for the PV of the coupons paid at the different times (As long as you use the correct value for the number of coupons and the appropriate yield rate).

Remember that the PV annuity notation represents a formula that calculates the present value of a series of payments (of equal amount) taking each of their times into account. Hope this helps!

how about if the question gives interest rate (i) and sinking fund earning (j)

I'm not entirely sure I understand your question. Can you provide more details on the problem/question you are trying to solve? I would love to help you and give you an answer, but I need a little bit more information. Let me know!

A loan at 8% annually has an initial payment of 1,000, and 9 further payments. The payment

amount decreases by 2% each year. Find the loan balance immediately after the third payment.@@JKMath for example

For this type of problem I believe my lesson video on Amortization may be of some help. The procedure is very similar, although my video does the focus on level payment loans, you can still apply it to a loan with decreasing payments (just can't use certain formulas I show you in the video). So feel free to check out... but here is the basic idea of how you would solve your problem:

To find the loan balance after the third payment, you need to subtract out the amount paid on the loan 3 years in, considering the interest that would be accumulated during that time. First you need the initial loan amount which would be the PV of the 10 payments of the decreasing geometric annuity. You can calculate that yourself (you may need to reference my video one esoteric annuities), but lets just represent the PV with L for this comment. Next you want to calculate the interest in the first year, so take L times the interest rate: L*.08. Subtract that amount from the first payment, so 1000 - L*.08. This will give you how much of the loan you actually pay off in the first year (the amount of the payment minus the interest accrued for the year). Then subtract this from the loan balance, and start the process over for year 2/the second payment. Take the new loan balance and multiply by .08. Then subtract that from the amount of the second payment (which is 1000(1-.02) since each payment decreases by 2%). Then subtract the result from the loan balance. You would then repeat this process again for the third payment, of which then you would be done for that example. Does this help? Let me know!