I want to appreciate all my subscribers from across the globe (Africa, Asia, Europe, the Middle East, The Americas, and The Pacific). Thank you all for your support. I am encouraged by your comments, questions, likes and critiques. They keep me focussed and poised to do better. I will continue to contribute my little quota such that every student and researcher will independently analyse his/her data. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Please do not keep me to yourself (lol) inform your friends, students and academic networks about my Channel. Tell them CrunchEconometrix breaks down the econometric jargons and teaches with simplicity. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

The computation for Chisq DF is "k-1" where k = no of regressors and 1 = constant. So, the correct DF is 1 not 2 but you will still get the same outcome and conclusion. Thanks for picking this out...deeply appreciated.

I am highly grateful... I came across your LinkedIn post .. Immediately I searched you here... Please I want to connect to you on LinkedIn.... I am Sanusi Akeem ACHIEVER.. PLEASE I WANT TO CONNECT TO YOU... YOU ARE DOING A GREAT JOB.. MORE GRACE MA'AM

Very nice and well-explained video. I want to ask if I have the ability to follow the same methodology in order to detect heteroskedasticity in panel data models. Thanks in advance

hi teacher. hope you are doing well. whenever i try to run heteroscedasticity test using views it shows "cross section effects with period GLS weights not allowed ". i dont know what does it mean. i am new in the field of econometrics. can u help me pls? thank you.

I was looking for such a teacher. She has her job very professionally. I want to interact with her. I am teaching Econometrics to Students of Economics Hons in Delhi University. Congratulations. Wonderful jib. Can I get her e mail id? I have a number of issues in Econometrics.

@@CrunchEconometrix mam it means there is no specific reason behind using ARCH test we can use it like other tests of Heteroscedasticity as per our wish...ok thanku mam

I want to appreciate all my subscribers from across the globe (Africa, Asia, Europe, the Middle East, The Americas, and The Pacific). Thank you all for your support. I am encouraged by your comments, questions, likes and critiques. They keep me focussed and poised to do better. I will continue to contribute my little quota such that every student and researcher will independently analyse his/her data. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Please do not keep me to yourself (lol) inform your friends, students and academic networks about my Channel. Tell them CrunchEconometrix breaks down the econometric jargons and teaches with simplicity. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

Ma i gave ur contact to a friend (commander) in UK....He needs clarifications on a concept n ideology...

@@onojadavidoguche4064 Ok, thanks. Please may I know from where (location) you are reaching me?

@@CrunchEconometrix I'm reaching you ma from...Nigeria.. Butbmy friend that needs more explanation...I spoke with him..n he said he has mailed you.

Well explained.

Thanks for the encouraging words, Rose. Appreciated!

Nice Lecture ...Dr.. Thanks from India..

Thanks for the encouraging feedback, Shamej. Deeply appreciated! Much love from Nigeria 🇳🇬

Thank you for your dedication, Dr. May I know how did you determine the 2 degree of freedom? Thank you.

The computation for Chisq DF is "k-1" where k = no of regressors and 1 = constant. So, the correct DF is 1 not 2 but you will still get the same outcome and conclusion. Thanks for picking this out...deeply appreciated.

@@CrunchEconometrix This is noted. Thank you for responding, Dr.

I am highly grateful...

I came across your LinkedIn post .. Immediately I searched you here...

Please I want to connect to you on LinkedIn....

I am Sanusi Akeem ACHIEVER..

PLEASE I WANT TO CONNECT TO YOU...

YOU ARE DOING A GREAT JOB..

MORE GRACE MA'AM

Thanks, Sanusi for the encouraging feedback. Deeply appreciated.

Very nice and well-explained video. I want to ask if I have the ability to follow the same methodology in order to detect heteroskedasticity in panel data models.

Thanks in advance

Hi Kokosis, thanks for the encouraging feedback. Yes, it is applicable to panel data analysis.

What do you do if you have heteroskedasticity and does it affect VECM?

Hi Kamran, heteroscedasticity affects ALL results the reason why it must be removed. You can re-estimate the model at higher lags.

Are you using the F test here since you equated every parameter to zero in the null hypothesis ?

Hi Saied, I explained the "decision criteria".

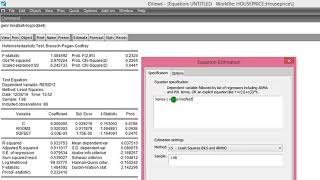

Hi madam, may i know, how do you get the 0.95 (in the genr chi) and the 2 degree of freedom?

Greeting from Malaysia. 😁

Hi Deralsd, 0.95 is the confidence interval of the test and 2 = number of regressors.

Thank you madam. 😁

hi teacher. hope you are doing well. whenever i try to run heteroscedasticity test using views it shows "cross section effects with period GLS weights not allowed ". i dont know what does it mean. i am new in the field of econometrics. can u help me pls? thank you.

Hi Fariha, I'm doing ok. If you follow my guides you shouldn't encounter any errors. Please follow the steps, thanks.

I was looking for such a teacher. She has her job very professionally. I want to interact with her. I am teaching Econometrics to Students of Economics Hons in Delhi University. Congratulations. Wonderful jib. Can I get her e mail id? I have a number of issues in Econometrics.

Wow, thank you, Ashis. Kindly post your questions here and will do my best to guide you. Take care.

Hello madam, how did you get the degree of freedom 2?

Hi Yashna, I have responded to you via Facebook.

@@CrunchEconometrix yes thank you

@@CrunchEconometrix hello madam same question here how did you get the degree of freedom 2?

mam when we can use ARCH test for heteroscadasticity?

You use it same you use every other test for heteroscedasticity.

@@CrunchEconometrix mam it means there is no specific reason behind using ARCH test we can use it like other tests of Heteroscedasticity as per our wish...ok thanku mam