04:50 04:57 Hi David, thank you very very much for your contributions, you're really teaching us the abc of a lot of financial relates topics! Please never stop! 😊 I wanted to very respectfully point out 2 little mistakes so that the new viewers that don't know anything about this topic can better understand it: 04:50 "a longer term indicates a lower (exchange rate of) delta". 04:57 "the (exchange rate of) delta tends to peak... I think this is important since the second derivative measures "the change in the exchange rate of the exchange rate" if x. In this case, gamma'd measure the change in the exchange rate of delta (which in turn is another exchange rate, namely the one of the option's price with respect to the stock's price). I hope I get this right 😅 Thank you very much again!

I am doing a MSc in Banking & Finance and I gonna start to do an internship in equity derivatives sales. Your videos are great to brush up my skills. Thx a lot for your fantastic work! Keep going!

Hi David, I absolutely love your videos. I work in an investment bank and appreciate these tutorials. I think you mentioned at 4:15 or so that "options out of the money have low deltas, as do options deep in the money"..when I think you meant (if I'm not mistaken) that the delta tends (perhaps asymptotically) towards 1 when an option is deep in the money. Just want to point that out, or maybe I'm missing something here. Thanks again for your service to the finance community. Much appreciate!

Yes because gamma is rate of change of delta, so the Gamma plot is understood by rate of change in delta; e.g., gamma going to zero b/c delta is stabilizing.

Thanks for the excellent presentation. Althought at 4:21 you state "We have low delta close to 0 when the option is deeply Out of the Money, and also when the option is deeply in the money. The second part seems incorrect. Option delta for deeply in the money is 1.0".

A Financial institution has the following portfolio of over on. Sterling: Type| Position|Delta|Gamma| Vega Call.| -1000 | 0.50. | 2.2. | 1.8 Call.| -500. | 0.80. | 0.6. | 0.2 Put.| -2000. | -0.40 | 1.3. | 0.7 Call | -500. | 0.70. | 1.8. | 1.4 A traded option is available with a delta of 0.6, a gamma 0f 1.5 and a vega of 0.8. (a) What position in the traded option and in sterling would make the portfolio both gamma neutral and delta neutral? (b) What position in the traded option and in sterling would make the portfolio both vega neutral and delta neutral?

What program are you using to check the Delta of an Option? I can't figure out how to check the greeks of an option at all. I been using Google and Yahoo Finance and they don't seem to have any way to view option greeks. I'm pretty new to this.

Oops.. at 4:50 you also mention "a longer term means a lower delta" when I think you meant "lower gamma". I know it's clear from the chart. Sorry, I just wanted to bring to your attention. Thx.

For sure! Actually, I started a new series on the FRM and we have planned a comprehensive set of videos that will definitely include an updated tour through the Greeks. Please stay tuned, er I mean, subscribe and I look forward to sharing what we've learned. Thanks!

04:50

04:57

Hi David, thank you very very much for your contributions, you're really teaching us the abc of a lot of financial relates topics! Please never stop! 😊

I wanted to very respectfully point out 2 little mistakes so that the new viewers that don't know anything about this topic can better understand it:

04:50 "a longer term indicates a lower (exchange rate of) delta".

04:57 "the (exchange rate of) delta tends to peak...

I think this is important since the second derivative measures "the change in the exchange rate of the exchange rate" if x. In this case, gamma'd measure the change in the exchange rate of delta (which in turn is another exchange rate, namely the one of the option's price with respect to the stock's price).

I hope I get this right 😅

Thank you very much again!

I am doing a MSc in Banking & Finance and I gonna start to do an internship in equity derivatives sales. Your videos are great to brush up my skills. Thx a lot for your fantastic work! Keep going!

Hi David, I absolutely love your videos. I work in an investment bank and appreciate these tutorials. I think you mentioned at 4:15 or so that "options out of the money have low deltas, as do options deep in the money"..when I think you meant (if I'm not mistaken) that the delta tends (perhaps asymptotically) towards 1 when an option is deep in the money. Just want to point that out, or maybe I'm missing something here. Thanks again for your service to the finance community. Much appreciate!

I'm sure you know already but Delta DOES NOT decrease when an option is deeply ITM @ 4:20. Thanks for the video.

Yes because gamma is rate of change of delta, so the Gamma plot is understood by rate of change in delta; e.g., gamma going to zero b/c delta is stabilizing.

Thanks for the excellent presentation. Althought at 4:21 you state "We have low delta close to 0 when the option is deeply Out of the Money, and also when the option is deeply in the money. The second part seems incorrect. Option delta for deeply in the money is 1.0".

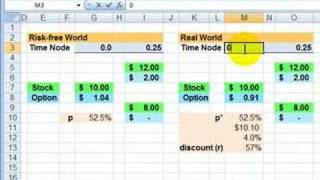

Can you explain how Delta, Gamma, etc, was calculated in this spreadsheet?

thanks for my time ? thank you for YOUR time ^^ very helpful

A Financial institution has the following portfolio of over on. Sterling:

Type| Position|Delta|Gamma| Vega

Call.| -1000 | 0.50. | 2.2. | 1.8

Call.| -500. | 0.80. | 0.6. | 0.2

Put.| -2000. | -0.40 | 1.3. | 0.7

Call | -500. | 0.70. | 1.8. | 1.4

A traded option is available with a delta of 0.6, a gamma 0f 1.5 and a vega of 0.8.

(a) What position in the traded option and in sterling would make the portfolio both gamma neutral and delta neutral?

(b) What position in the traded option and in sterling would make the portfolio both vega neutral and delta neutral?

Nice work man

Thanks .. i'm studying APRM from PRMIA .. and this was helpful

@TimbergoSpielbergo thanks, short but sweet and supportive!

In exlaining Gamma, it is repeatedly quoting Delta.

Excellent explanation! Thank you!

Theta, Vega and Rho are the rate of change in the portfolio value with respect to their respective variables, not the change in option price..

Amazing! Great job!

Could you share the excel, please?

What is a free program or website that will let me view the greeks of different options? I've looked all over the place. Thanks

What program are you using to check the Delta of an Option? I can't figure out how to check the greeks of an option at all. I been using Google and Yahoo Finance and they don't seem to have any way to view option greeks. I'm pretty new to this.

Oops.. at 4:50 you also mention "a longer term means a lower delta" when I think you meant "lower gamma". I know it's clear from the chart. Sorry, I just wanted to bring to your attention. Thx.

When explaining Gamma, it is repeatedly saying Delta.

What about a put option? Can you make another video on put options?

For sure! Actually, I started a new series on the FRM and we have planned a comprehensive set of videos that will definitely include an updated tour through the Greeks. Please stay tuned, er I mean, subscribe and I look forward to sharing what we've learned. Thanks!

great exp. Thanks.

Excellent

someone can tell me how to read gamma

you are amazing!

Great

Do gamma rays mutate your mom's rho, or is her vega to sore from delta's theta?

The 5th term should be Theta.

someone can tell me how to read gamma