Had I watched it before knowing a little bit what these terms are, I would have not understood it. It has been amazing to clear my haziness! Great job! Thank you so much for explaining things with such nice intuition

@04274108 The standard deviations (ie., volatilities) are SQRT(0.67) not 0.67, so correlation = 0.67 / SQRT(0.67)*SQRT(0.67), and since SQRT(0.67)*SQRT(0.67) = 0.67, we have 0.67/0.67. Thanks for your kind words!

@chrisxed thanks, that is correct. Both are linear co-movement. As covariance is rendered in the same awkward format as variance (i.e., units^2 or returns^2), correlation translates it into a unitless (intuitive) format.

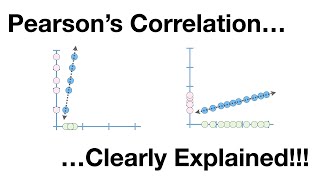

@hawaypg there are no sample statistics here, these are (to keep it simple) merely illustrating "population" -based correlation. As the Average(X) = 3, the (population) variance of X = average[0^2, 1^2, 1^2] = 0.67, such that the StdDev(X) = SQRT(0.67). Similarly, (pop) var(Y) = avg[0,1,1]. It's not meant to be coincident, i just didn't show the StdDev calcs. Hope that explains, thanks, David

if it isn't 1, it means that the relationship resembles a straight line, that is, that you can model it as a linear relationship. The point about causality is very important to understand, by the way, and a lot of people confuse that.

You all probably dont give a shit but does someone know of a trick to log back into an instagram account? I somehow lost the account password. I would love any help you can give me

@Yael Rayden i really appreciate your reply. I got to the site through google and im in the hacking process now. Looks like it's gonna take quite some time so I will reply here later with my results.

Even though your aim was financial math, you kept the theory discussion nicely generalized. Great job! What you're saying is that the correlation (functional) is the normalization of the covariance (i.e. makes it a dimensionless metric). I'm certain that the term covariance refers to complimentary-variance similar to the cosine being a complimentary-sine. Is this correct?

Thank you for the alternative formula! I was having trouble inputting all the values one-by-one and computing all the differences and squares by hand. Little did I know that I could use r to convert it into covariance by multiplying it with the sds of x and y!!! Thanks again!!! Edit: Misspelled word

Would there be a bionicturtle complete course which takes the individual through a complete dissertation of these statistical quantities, and then translates them into practical use by application to 'the greeks' components in options?

@patrickrueegg Actually the standard deviation of both X and Y is 1. However, the variance of both is 0.81649658. As you have correctly pointed out 0.816497 x 0.816497 = 0.67. The covariance coefficient and the final correlation coefficient remains the same but the denominator he discusses in the correlation formula is entirely wrong. The correlation formula should read: Cov(X,Y) / (σx * σy)

Awesome video! This might be a irrelevant question, but what is the reason behind dividing with the product of the standard deviation in order to translate the covariance to correlation?

Missed a tutorial on covariance, found that the suggested reading only made it more difficult, your video on the other hand, was fantastic. Solved and completed my work in no time at all. Thanks. Although saying that - I did get a question wrong. I had a question where the covariance was 0, and it then proceeded to ask if X and Y were independant, i thought yes, but that's apparently incorrect. Do you have any videos explaining why this is? Thanks x

I thank you so much for this tutorial but I have something to ask you,does the covariance in bi-variate distribution differ from those formula you showed in this tutorial?

thanks a lot, my lecture gave me note function last night n i try to search what she want me to annalise, is the coefficient correlation similar with probability (ρ)?

no, not even, correlation is merely a measure of observed *linear* relationship between two variables. Says nothing about causality; e.g., a third variable can cause them both. Further, it's just linear - variables can be dependent but non-linear. A limited metric.

Another thing that I believe may be tripping people up here is that you forgot to put (n) into the denominator of the equation for covariance (where shown)... unless my eyes are failing me.

So if the correlation is 1, that explains what is happening between assets in X and Y right? And what does the 1 actually mean in relation to Assets in X and Y? Can u explain asap please

0.67 multiplied by 0.67 should be 0.4489. so the calculation of correl is 0.67/(0.67*0.67) or 0.67/0/4489 = 1.5 . Actually the s.d of both series are 0.8165, and the product of the s.d is 0.67 which returns the correct correl of 1.0

nope, wrong, the correlation cannot be 1.5. The video is correct. The variance of each of X and Y is 2/3 or 0.667 such that σ(X) = σ(Y) = sqrt(0.667), the (population) covariance, σ(XY) = 0.667, so the correlation, ρ = 0.667/[sqrt(0.667)*sqrt(0.667)] = 0.667/0.667 = 1.0. Just like my video says, but thank you for the opportunity for me to check it yet AGAIN ... 10 years later! ;)

Hi Jane, yours is a correct sample variance because yours divides 2 by (n-1) or 3 rather than my population variance which divides 2 by n or 3. This is an old video of mine and frankly the sample covariance is better here when there are just a few points, so i think you are correct. thanks!

Where do we use this formula cov(X,Y)=∑_(all(x))∑_(all(y))〖XYP(X-μx)(Y-μy)P(X,Y)〗in computing covariance and how to use it?If possible use a typical example to show me how we solve a bi-variate distribution with this formula.Thank you very much,I wish that this will work.

Search for the difference between covariance and correlation and you'll find 1000 confused "answers". Finally, here is the answer in this video. If I'm understanding it correctly, they are essentially measuring the same thing (hence the confusion) but the correlation coefficient is a way to orient this property in a way that makes intuitive sense for humans (a range between -1 and 1 vs. an arbitrary number meaning who knows what out of context).

@meyero90 std of x=sqrt of {(3-3)*(3-3)+(2-3)*(2-3)+(4-3)+(4-3)}/ total no of items ie3=sqrroot of 2/3-sqr root of .67 similarly sd of y =sqrroot of .67

You definitely made my day. My Investment Analysis class confused me...but you clarified it for me. Wish more professors could teach like you.

Had I watched it before knowing a little bit what these terms are, I would have not understood it. It has been amazing to clear my haziness! Great job! Thank you so much for explaining things with such nice intuition

Thank you for watching and for providing such positive feedback! We are happy to hear that this was so helpful.

I looked at half a dozen explanations and after 3 minutes of your video it all clicked. Well done!!

Thank you for watching! We are happy to hear that our video was so helpful :)

@04274108 The standard deviations (ie., volatilities) are SQRT(0.67) not 0.67, so correlation = 0.67 / SQRT(0.67)*SQRT(0.67), and since SQRT(0.67)*SQRT(0.67) = 0.67, we have 0.67/0.67.

Thanks for your kind words!

@chrisxed thanks, that is correct. Both are linear co-movement. As covariance is rendered in the same awkward format as variance (i.e., units^2 or returns^2), correlation translates it into a unitless (intuitive) format.

This is a great explanation and interpretation. Most tutorials neglect to give the numbers meaning in-context.

@scottbroadway my pleasure, thanks for you kind feedback, makes my day!

@hawaypg there are no sample statistics here, these are (to keep it simple) merely illustrating "population" -based correlation. As the Average(X) = 3, the (population) variance of X = average[0^2, 1^2, 1^2] = 0.67, such that the StdDev(X) = SQRT(0.67). Similarly, (pop) var(Y) = avg[0,1,1]. It's not meant to be coincident, i just didn't show the StdDev calcs. Hope that explains, thanks, David

if it isn't 1, it means that the relationship resembles a straight line, that is, that you can model it as a linear relationship. The point about causality is very important to understand, by the way, and a lot of people confuse that.

Why couldn't my teacher have put it like that? Been struggling over this for weeks, huge THANKYOU!

A very clear explanation for such an abstract topic that's been giving me problems. Thank you.

Fantastic explanation! Thank you :)

The relationship with finance adds a useful perspective that I hadn't considered before too.

Thank you, thank you, thank you! This was a great help tying covariance and correlation together. Clear and to the point, can't thank you enough!

You all probably dont give a shit but does someone know of a trick to log back into an instagram account?

I somehow lost the account password. I would love any help you can give me

@Caleb Antonio Instablaster :)

@Yael Rayden i really appreciate your reply. I got to the site through google and im in the hacking process now.

Looks like it's gonna take quite some time so I will reply here later with my results.

@Yael Rayden it worked and I finally got access to my account again. Im so happy!

Thank you so much you saved my ass !

@Caleb Antonio You are welcome =)

sooooooo easy to understand this solve all of my problems in understanding portfolio. Thank you very much sir.

Even though your aim was financial math, you kept the theory discussion nicely generalized. Great job! What you're saying is that the correlation (functional) is the normalization of the covariance (i.e. makes it a dimensionless metric). I'm certain that the term covariance refers to complimentary-variance similar to the cosine being a complimentary-sine. Is this correct?

i have been browsing around for something like this--very helpful. statistics suffers from somewhat clunky notation

Thank you for the alternative formula! I was having trouble inputting all the values one-by-one and computing all the differences and squares by hand. Little did I know that I could use r to convert it into covariance by multiplying it with the sds of x and y!!! Thanks again!!!

Edit: Misspelled word

Would there be a bionicturtle complete course which takes the individual through a complete dissertation of these statistical quantities, and then translates them into practical use by application to 'the greeks' components in options?

@patrickrueegg

Actually the standard deviation of both X and Y is 1. However, the variance of both is 0.81649658.

As you have correctly pointed out 0.816497 x 0.816497 = 0.67. The covariance coefficient and the final correlation coefficient remains the same but the denominator he discusses in the correlation formula is entirely wrong. The correlation formula should read: Cov(X,Y) / (σx * σy)

thank you very much, very good explanation, and the example showing how get the values just save me. thank you a lot

it's our pleasure, thank you!

your explanation just helped me understand it lol why can't people just say it like you in an easy concise way?

Youre freaking awesome! I am still wondering why the St. Dev is the same for x and y. Can you explain me that part please?

Awesome video! This might be a irrelevant question, but what is the reason behind dividing with the product of the standard deviation in order to translate the covariance to correlation?

@halfstep007 Here, here. This guy deserves a medal.

Missed a tutorial on covariance, found that the suggested reading only made it more difficult, your video on the other hand, was fantastic.

Solved and completed my work in no time at all. Thanks.

Although saying that - I did get a question wrong.

I had a question where the covariance was 0, and it then proceeded to ask if X and Y were independant, i thought yes, but that's apparently incorrect. Do you have any videos explaining why this is?

Thanks x

Thank you for making this intuitive, makes a lot more sense now.

awesome dude, you are making a great contribution to society.

Wow, thank you very much. I'm studying for CFA and this helped a lot.

You explained very simply.......thanx a lot !

you've made some points very, very clear. thank you!

i love you, worked for building my foundation understanding in econometrics!

@jim8z3 thank you, for such kind feedback

Life saver. Very well explained

great tutorial . thanks for expanding my concepts .

Thank you for watching! We are happy to hear that our video was helpful!

I thank you so much for this tutorial but I have something to ask you,does the covariance in bi-variate distribution differ from those formula you showed in this tutorial?

i appreciate that, thanks for your support!

Is there a mistake at 5:02

Does sigma xy represent cov(x,y)?

thanks a lot, my lecture gave me note function last night n i try to search what she want me to annalise, is the coefficient correlation similar with probability (ρ)?

no, not even, correlation is merely a measure of observed *linear* relationship between two variables. Says nothing about causality; e.g., a third variable can cause them both. Further, it's just linear - variables can be dependent but non-linear. A limited metric.

Man, you should just go to a campus bar and introduce yourself as Bionic Turtle. You'd get all the beers bought for you you wanted! Thanks for help.

Thank you soo much - Perfect explanation of relationships

Another thing that I believe may be tripping people up here is that you forgot to put (n) into the denominator of the equation for covariance (where shown)... unless my eyes are failing me.

Great Video. Awesome explanation.

Its not 0.67 / (0.67*0.67) .It is 0.67 /sqrt(0.67)*sqrt(0.67) which equals 1.Hope it helps.

So if the correlation is 1, that explains what is happening between assets in X and Y right? And what does the 1 actually mean in relation to Assets in X and Y? Can u explain asap please

hello what is the expected value of 1 and 1. if it is the average, isn't 1. please help

Thank you. Knowledge is golden!

That was awesome. Thanks for sharing.

watching the video on 2023 thank you

thank that makes things so clear for me now !

@tedecc I have a biostats exam in two hours too! My lecturers lectures are also confusing

0.67 multiplied by 0.67 should be 0.4489. so the calculation of correl is 0.67/(0.67*0.67) or 0.67/0/4489 = 1.5 . Actually the s.d of both series are 0.8165, and the product of the s.d is 0.67 which returns the correct correl of 1.0

nope, wrong, the correlation cannot be 1.5. The video is correct. The variance of each of X and Y is 2/3 or 0.667 such that σ(X) = σ(Y) = sqrt(0.667), the (population) covariance, σ(XY) = 0.667, so the correlation, ρ = 0.667/[sqrt(0.667)*sqrt(0.667)] = 0.667/0.667 = 1.0. Just like my video says, but thank you for the opportunity for me to check it yet AGAIN ... 10 years later! ;)

when I use your data in Matlab, it says the covariance between x and y (cov(x,y) = 1, not .67. What is going on?

Hi Jane, yours is a correct sample variance because yours divides 2 by (n-1) or 3 rather than my population variance which divides 2 by n or 3. This is an old video of mine and frankly the sample covariance is better here when there are just a few points, so i think you are correct. thanks!

Thanks, this was helpful!

very very well put please come teach my finance class!

thank you, best explanation of covariance!

Where do we use this formula cov(X,Y)=∑_(all(x))∑_(all(y))〖XYP(X-μx)(Y-μy)P(X,Y)〗in computing covariance and how to use it?If possible use a typical example to show me how we solve a bi-variate distribution with this formula.Thank you very much,I wish that this will work.

how did you get the standard deviation for x and y?

Thank you for a clear explanation!

Amazing Explanation..cant thank you enough :)

Thank you David it helps.

You're welcome! Thank you for watching!

I doubt that .67 is not standard deviation. According to my calculation it is variance, is not it?

sqrt(0.67) does

Wind Scant Yea I was a bit confused but yea the denominator for the final equation is (sqrt(.67)*sqrt(.67)) or simply .67

Perfect explanation. So far I have not understood this shit. Thank you.!!

great explanation! Thanks a lot!!

Thanks for your vids, better than my professor, haha

nice explanation!

GREAT! Keep it up!!

thanks for your informative video

thanks, best explanation. I like the idear to change all the math symbols to plain english.

salute u sir!

just worked out why - thanks a lot. x

Search for the difference between covariance and correlation and you'll find 1000 confused "answers". Finally, here is the answer in this video. If I'm understanding it correctly, they are essentially measuring the same thing (hence the confusion) but the correlation coefficient is a way to orient this property in a way that makes intuitive sense for humans (a range between -1 and 1 vs. an arbitrary number meaning who knows what out of context).

really well donne, keep going.

Thaks

Very helpful! Thanks :)

saved me, thanks man

thank you so much for this!

thanks so much for posting =D

Thank tou sir ..that really helped...

Excellent!

Thank you for watching!!

s.d of x *s.d. of y = 0.4489 andnot 0.67

wow that was helpful, thanks!

I hate why Statistics professors don't teach like this, in this patient way!!!!!!...

Thank You a Lot

You're welcome! Thank you for watching!

@meyero90 std of x=sqrt of {(3-3)*(3-3)+(2-3)*(2-3)+(4-3)+(4-3)}/ total no of items ie3=sqrroot of 2/3-sqr root of .67 similarly sd of y =sqrroot of .67

thx u so much

Thanks a lot

Thanks for post

Thank you!!!

1.0

LAMENS TERMS PLEASE

nice

Thank you for watching!

he speaks too slowly! I have a test tomorrow I need this info fast

you sound like the chef guy from foodwishes! 8D

j

Thank you soo much - Perfect explanation of relationships

thank you so much for this!