(EViews10) - How to Forecast ARCH Volatility

HTML-код

- Опубликовано: 21 авг 2024

- This video simplifies the understanding of the autoregressive conditional heteroscedasticity (ARCH) using an approach that beginners can grasp. The video series will contain four other tutorials: (1) How to Simulate ARCH model; (2) How to Test for the presence of ARCH Effects; (3) How to Estimate ARCH Models and (4) How to Forecast ARCH Volatility. So, what is ARCH? Autoregressive indicates that heteroscedasticity observed over different time periods may be autocorrelated; conditional informs that variance is based on past errors; heteroscedasticity implies the series displays unequal variance. Popularised by Nobel Prize Winner, Robert F. Engel (1982)

Why use ARCH: Models the attitude of investors not only towards expected returns but also towards risk (uncertainty); Relates to economic forecasting and measuring volatility; Techniques ARCH, ARCH-M, GARCH, GARCH-M, TGARCH and EGARCH; Concerned with modeling the volatility of the variance; Conditional and time-varying variance; Deals with stationary (time-invariant mean) and nonstationary (time-varying mean) variables; Nonstationary varying mean; Heteroscedastic varying variance; Concerns financial and macroeconomic time series; Duration daily, weekly, monthly, quarterly (high frequency data); Financial/economic series stock prices, oil prices, bond prices, inflation rates, exchange rates, interest rates, GDP, unemployment rates etc.

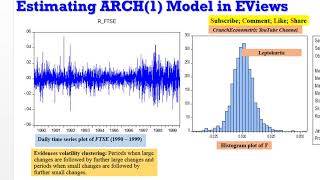

What is conditional variance? The assumption of homoscedasticity (constant variance) is very limiting, hence preferable to examine patterns that allow the variance to depend (conditional) on its history. Volatility: When the values of financial variables change rapidly from time to time in an apparently unpredictable manner. Volatility Clustering: Periods when large changes are followed by further large changes and periods when small changes are followed by further small changes. Shows wild and calm periods.

The ARCH Estimator: The presence of ARCH does not affect consistency of OLS. Still has desirable properties under ARCH. OLS yields consistent but inefficient estimates. Estimates of the covariance matrix will be biased. Leading to invalid t-statistics. Remember, these are valid for any form of heteroskedasticity, and ARCH is just one particular form of heteroskedasticity. An efficient estimator is required maximum likelihood algorithm.

Some Lessons Learnt: The time-varying variance is modeled by the procedure called autoregressive conditional heteroscedasticity (ARCH); ARCH simply conveys that the series in question has a time-varying variance (heteroscedasticity) that depends on (conditional on) lagged effects (autocorrelation); ARCH model is intuitively appealing because it explains volatility as a function of the errors. These errors are called “shocks” or “news” by financial analysts. They represent the unexpected!; The larger the shocks, the greater the volatility in the series; Since variance is often used to measure volatility, and volatility is a key element in asset pricing theories, ARCH models have become important in empirical finance; Most financial time series like stock prices, exchange rates, oil prices etc. exhibit random walks in their level form, that is, nonstationary (time-varying means); But stationary at 1st difference which often exhibit wide swings or volatility; Wide swings suggest that the variance of the financial time series changes over time (time-varying volatility); Volatility clustering big changes in u_t are fed into further big changes in h_t via the lagged effects u_(t-1); ARCH modeling has become increasingly popular; useful for modeling volatility; especially changes in volatility over time (that is, time-varying volatility).

Here is the link to the data used: www.macmillani...

References and Readings: Asteriou and Hall (2016) Applied Econometrics, 3ed; Hill, Griffiths and Lim (2008) Principles of Econometrics, 3ed; Roman Kozan (2010) Financial Econometrics with EViews; Gujarati and Damodar (2009) Basic Econometrics, International Edition; R. Engle, “Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation,” Econometrica, vol. 50. No. 1, 1982, pp. 987-1007; A. Bera and M. Higgins, “ARCH Models: Properties, Estimation and Testing,” Journal of Economic Surveys, vol. 7, 1993, pp. 305-366.

Follow up with soft-notes and updates from CrunchEconometrix:

Playlists: / cruncheconometrix

Website: cruncheconometr...

Blog: cruncheconomet...

Facebook: / cruncheconometrix

RUclips Custom URL: / cruncheconometrix

Twitter: / crunchmetrix

Reddit: / crunchmetrix

Beloved guest/subscriber, you have discovered my amazing RUclips Channel tailored specifically for you and other beginners and intermediate users. Please do not keep me to yourself (lol). Kindly share my videos and links with your students, colleagues and academic community so that they too can SUBSCRIBE and learn with ease….and for the global community to be aware that applied econometrics can be simplified. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

This is a very useful site for those with interest in financial econometrics. From Seoul, South Korea.

Thanks for the encouraging words and feedback. Deeply appreciated!

Thank you ma. I'm a graduate student studying in the United States and I'm taking a class on quantitative methods of finance II using stata.

I have a project due tomorrow, and this video has helped me understand a whole lot more about ARCH modeling . O seun pupo ma 🙏🙏.

You are most welcome, Sir Traveler! (lol)

plz need your help ths is also my project

Hi Nazia, please go ahead with your question.

Thank you mam. Your videos are helping me out a lot in my thesis research of Masters degree in Economics.

From Nepal, SA.

Thanks Aditya, for the kind words. I wish you the best in your future endeavors. Much love from Nigeria 🇳🇬! 💞

@@CrunchEconometrix you are welcome mam... keep blessing students like us. Waiting for your more videos! ☺

All your videos are really good to understand and apply in research activities. Thank you for sharing these videos

Thanks for the positive feedback, Tushar. Deeply appreciated! May I know from where (location) you are reaching me?

@@CrunchEconometrix Mumbai, India

@@CrunchEconometrix could you please upload videos on Baysian SVAR. and PARX model?

I love the way you explain the complex econometric things in the simplest possible way.

@@tusharpanigrahi4138 Awesome! I have many research collaborators from India. good people!...please spread the word about my YT Channel to your students and colleagues. Encourage them to subscribe. Thanks!

@@tusharpanigrahi4138 I will definitely once I fully grasp the procedure. Thanks for the encouragement, Tushar!

All your videos are really easy to understand

Thanks, Tushar for the positive feedback. Deeply appreciated! May I know from where (location) you are reaching me?

its good to see you again in RUclips ;)

Hahahaha, thanks Gus....I literally had to whip myself back😄. School work and manuscripts took much of my time. More educative videos coming. Thanks for the support...gracias! 🙏 😄

@@CrunchEconometrix Excellent work Prof. These videos are of high quality.

Thanks WW2 for the encouraging feedback😄

i have see all videos on ARCH Modeling. Great job done ....thanks a lot. Please guide us on GARCH Models also. Request you to make some videos on GARCH also

Thanks Monica for the positive feedback on my videos. Deeply appreciated! 💕 Will do the GARCH once I fully understand the concept. May I know from where (location) you are reaching me?

Good day Proff, thanks for the educative videos. Can you please provide EViews tutoring on Volatility Spillover and Volatility Transmission between products and between markets (e.g) Gold and Oil prices; Wheat and Maize prices. Transmission of Wheat prices in Nigeria vs Wheat price in Kenya etc.

Hi Kalima, I may but it will be published on my Teachable paid platform cruncheconometrix.teachable.com

Great job. Waiting for a video on nonlinear Ardl model

Thanks for the positive feedback, Yeboua. Deeply appreciated! 💕 I'll do my best regarding NARDL as I've received many requests. Though, I'm yet to learn the procedure. May I know from where (location) you are reaching me?

@@CrunchEconometrix İstanbul

@@yebouakouassi3694 Wow! Kindly spread the word about my videos to your friends and academic community in Turkey 🇹🇷...thanks 😊

Please, upload videos on Panel Data analysis. What differentiates it from the Seemingly Unrelated Regression Estimation (SURE) and when to use any of them.

I'll do my best Chukwuma to create those videos once I clear up my backlogs. Thanks for watching and sharing. Grateful!

Good day ma. Thanks for the video. I have watched all the ARCH videos twice and I must commend the simplicity, the passion and the understanding of it. Great. Job!

My question is, the analysis you did showed that investors should hold their investments because the ARCH graphs are seen to be steady over the period. How do investors know when to sell off their shares or purchase more shares using the ARCH forecast?

Thanks.

Hi Chukwuma, same way an investor wants to hold a "stable" asset, no investor wants to hold a "volatile" asset. So, once the forecast shows volatility, the incentive to sell that asset rises. Hope this clarifies, thanks.

hello Ma'am you are doing a great job here. I have been following from quite some time now. Your explanation is crisp. can you post a video on Asymmetric causality test by Hathemi J(2012) on GAUSS software?

Thank you.

Hi Ayesha, thanks so much for the positive feedback. Deeply appreciated! 💕. But honestly I don't know what that procedure entails and I've never used the GAUSS software too...sorry 🙏

Requesting you to upload videos on Multivariate GARCH, Structural VAR and Baysian VAR using EVIEWS interface

Tushar, I'll do my best once I understand the techniques😊

Ma'am, your videos are very useful.

Objective of my research is finding the impact of Foreign Institutions Investment on the Volatality of Stock Market using GARCH model.

Is there some wrong in the objective. If no, how can we do it using GARCH Model?

Will be thankful If you can explain.

Regards

Thanks for the encouraging words and feedback about my videos. Deeply appreciated! But I don't delve into research topics. Out of my scope. Apologies🙏

What if forecast mean is not significant when p value is more than .05

Hi Arup, not significant implies no impact. Zero information about the future.

Thank you very much for these lectures. I have been working on a paper, I have data on oil price however, what I need is the oil price volatility, can i measure oil price volatility from the oil price data using ARCH?

Yes, you can. That is what I explained in the video.

Thank you very much Doc. for the insightful video. Could you please help me with how l could use eviews to generate annual crude oil price volatility for a 34 year period i.e from 1983 to 2017.

Hi Dennis, thanks for the positive feedback on my videos. Deeply appreciated! 💕 But what you need to do is not different from what I showed in this clip. Simply follow the process and modify your data accordingly. Thanks.

Hi Bosede, great videos. I was wondering how to get the arch data before you plotting the graph. Do you have for Garch models like Egarch tutorials as well. :)

Hi Khairul, I don't have the permission to share the Asteriou and Hall dataset...and I don't have videos on GARCH modeling, yet. Thanks for watching and the positive feedback, deeply appreciated! May I know from where (location) you are reaching me?

Malaysia :)

@@mustanggemini2156 Awesome! Kindly spread the word about my RUclips Channel to your friends and academic community in Malaysia 🇲🇾! 😀

Dr Bosede, may I know the best way to communicate with you for your suggestions and advice on econometrics issues which are related to your videos?

@@mustanggemini2156 You can always reach me via this medium. I will respond to your queries. Thanks.

Please understand the meaning of the standard error. Do not teach wrong. Other videos are very good. But here i have to differ. No forecast value can go beyond SE band as the positive and negative SE depend on the forecasted value. Then how can it go beyond it as per your interpretation?

Thanks, Suman for input. Appreciated.

What is the main difference between dynamic and static?

The inclusion of the lagged depvar as an explvar.

@@CrunchEconometrix so in my conclusion if i want to take MSE and MAE to comparison, is it will make any different?

Not to my knowledge.

how to forecast next period ؟؟؟

You do this by adjusting the sample period as demonstrated in the video.

@@CrunchEconometrix hell dear, thank you for your videos

I would like to forecast next future months,

When I change directly periods, it wont giving me result? How to forecast next periods?

Please