Implied Volatility Calculation with Newton-Raphson Algorithm

HTML-код

- Опубликовано: 30 июл 2024

- ★★ Save 10% on All Quant Next Courses with the Coupon Code: QuantNextRUclips10 ★★

★★ For students and graduates, we offer a 50% discount on all courses, please contact us if you are interested ★★

★★ Visit us: quant-next.com ★★

★★ Contact us: contact@quant-next.com ★★

★★ Follow us: / quant-next ★★

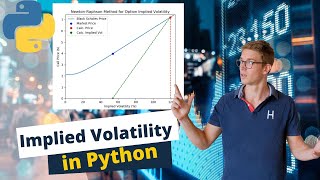

I will present in this video the Newton-Raphson method for extracting the implied volatility from option prices.

The Python code is available in the related article: quant-next.com/implied-volati...

0:00 Introduction

0:13 Black-Scholes Price vs Volatility

0:54 How to Calculate the Volatility Implied by Option Prices?

1:22 Newton-Raphson Method

1:56 Python Code - Generic

2:40 Newton Raphson Method - Derivation

3:06 Newton Raphson Method - Drawbacks

3:29 Implied Volatility Calculation - in Practice

4:42 Python Code

#quantnext, #optionpricing, #derivatives, #quantitativefinance, #financeeducation

Keep uploading, amazing work! Thank you. ❤

Thank you for your feedback and your support!

Thank you so much!!!

Thanks for the support!