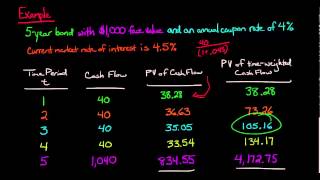

@back2root just to clarify further, the general form of the Price (PV) of the zero coupon bond is here: PV = face / (1+y/k)^(k*T) where y = ytm & k = periods per year. So, your PV is true for k=1 and mine is true for k = 2. So, as k increases, the price decreases and ultimate converges (as k tends to infinite) on continuous compounding where PV = face*exp(-y*T) where T = number of years.

Hi Josh, yes that is correct. Under daily (although T = 250 or 252 trading days), the y/k term is small but non-zero, such that for a given Mac duration, modified duration varies (a little), is variant to the compound frequency, and is slightly less than Mac duration. As k --> infinite, y/k --> 0 and we have the special case: only when compounding is continuous does Mac = Mod duration. Thanks,

@back2root $55.84 assumes effective annual yield (i.e., annual instead of semi-annual) as 55.88 = 100/(1+6%)^10. So, i think you've shown why discount (compound) frequency impacts the PV. It's just the reverse of compounding forward, where it also matters. Mine is semi-annual: 55.37 = 100/(1+6%/2)^(10*2). In extremis, the PV under continuous = $54.88 = 100*exp(-6%*10).

hi bionicturtledotcom, Just a little confused on something...if you were to find the daily compounded equivalent ytm...obviously ytm would be smaller right?...it is about 5.91%. so if we redid this exercise using y=5.91% and k=365...then the y/k term = 1.619*10^-4. Using semi-annual compounding, the y/k term = 0.03. With Macaulay duration always the same, both methods will bear different results for modified duration????

@back2root just to clarify further, the general form of the Price (PV) of the zero coupon bond is here: PV = face / (1+y/k)^(k*T) where y = ytm & k = periods per year. So, your PV is true for k=1 and mine is true for k = 2. So, as k increases, the price decreases and ultimate converges (as k tends to infinite) on continuous compounding where PV = face*exp(-y*T) where T = number of years.

Hi Josh, yes that is correct. Under daily (although T = 250 or 252 trading days), the y/k term is small but non-zero, such that for a given Mac duration, modified duration varies (a little), is variant to the compound frequency, and is slightly less than Mac duration. As k --> infinite, y/k --> 0 and we have the special case: only when compounding is continuous does Mac = Mod duration. Thanks,

@back2root $55.84 assumes effective annual yield (i.e., annual instead of semi-annual) as 55.88 = 100/(1+6%)^10. So, i think you've shown why discount (compound) frequency impacts the PV. It's just the reverse of compounding forward, where it also matters. Mine is semi-annual: 55.37 = 100/(1+6%/2)^(10*2). In extremis, the PV under continuous = $54.88 = 100*exp(-6%*10).

So an Interest paying bond will have lower Modified Duration than a Zero coupon bond?

hi bionicturtledotcom,

Just a little confused on something...if you were to find the daily compounded equivalent ytm...obviously ytm would be smaller right?...it is about 5.91%.

so if we redid this exercise using y=5.91% and k=365...then the y/k term = 1.619*10^-4.

Using semi-annual compounding, the y/k term = 0.03.

With Macaulay duration always the same, both methods will bear different results for modified duration????