Stochastic Calculus Simplified: Probability, Brownian Motion, and Ito Integrals - Part 1

HTML-код

- Опубликовано: 11 июл 2024

- To support our channel, please like, comment, subscribe, share with friends, and use our affiliate links!

Don't forget to check out our patreon:

/ mathematicaltoolbox

An Informal Introduction To Stochastic Calculus With Applications: amzn.to/42lftyR

An Informal Introduction To Stochastic Calculus With Applications 2nd Edition: amzn.to/3LWTwAk

(Affiliate Links)

Thank you for supporting my channel!

0:00 About the Course, Prerequisites, and Disclaimer

3:16 Expectation and Variance

4:26 Brownian Motion

5:41 Sample Path of Brownian Motion

6:30 Moments of Brownian Motion

8:05 Some Examples using Expectation and Variance

9:00 Example 2

10:11 Example 3

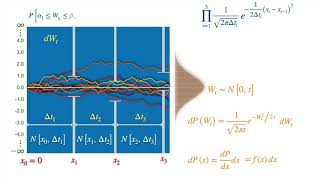

11:00 Ito Stochastic Integral

11:20 Examples of Ito Integrals

12:18 Some Important Identities

12:35 Basic Properties of the Ito Integral

12:54 Random Variable Properties of the Ito Integral

13:37 The Weiner Integral

14:39 Closing Comments and Part 2

Great initiative! Ito calculus is one of the most fascinating subjects. And the measure theoretic part of it can be quite demanding!

Thank you. It is definitely fascinating. It demanded my attention many years ago and has not wavered since. I hope that someone can find some utility in this series and that the field can become accessible to a wider audience.

Indeed, measure theory can be tough.

Thank you for the comment!

Gold content! I'm studying SDE by myself and it's perfect, hope that you're gonna make more content on SDE and how to code it in Python or other programming languages!

Thank you! I am always so happy whenever someone finds this useful. Sorry to disappoint you, but I don't plan on doing videos on Python or other programming languages. At least not with respect to SDE. It's just not where I want to dedicate my time. Perhaps in the future!

I plan on ending the series in three to four more videos. The final video will be on how to solve a simple stochastic partial differential equation.

By the way, judging by your name, you might be interested in this cool book on Mathematical Finance by Saari. Here's an affiliate link: amzn.to/3uNYA3O

Thank you again!

Whats your review on the Steven Shreve's books about Stochastic Calculus?

It's a very good book if you're interested in finance and have knowledge of probability. I had used it before and never had a problem with it. Shreve is a master at explaining the concepts of Stochastic Calculus.

It's entirely possible to go something like Calin into Shreve or Klebaner or Evans or Solin and Sarkka or Capasso and Bakstein. You can avoid Calin if you have some probability under your belt and some mathematical maturity (some experience with analysis would help with some of these).

EDIT: I would like to add that there are several solution manuals to Shreve online.

Why you hide other 2 videos?

Parts 3 and 4 in the series? I have not recorded them yet, but part 2 is available. They were not very popular, so I've prioritized making other videos. I'll upload them within the next week or two. Thanks for showing interest.