Deflated Sharpe ratio: Adjusting for multiple testing (Excel)

HTML-код

- Опубликовано: 19 окт 2024

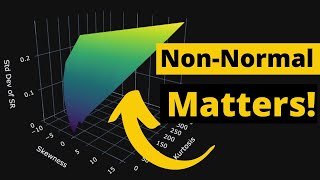

- It is very common in portfolio management and algorithmic trading to test a wide range of strategies before settling on the best-performing one. That is important for performance evaluation as it would mean the Sharpe ratio is inflated due to multiple testing. The deflated Sharpe ratio (DSR) is the go-to technique to take into account both the non-normal return distribution and multiple testing concerns when investigating various strategies. Today we are implementing the deflated Sharpe ratio calculation in Excel and discussing the concepts behind it.

Don't forget to subscribe to NEDL and give this video a thumbs up for more videos in Portfolio management!

Please consider supporting NEDL on Patreon: / nedleducation

You can find the spreadsheets for this video and some additional materials here: drive.google.com/drive/folders/1sP40IW0p0w5IETCgo464uhDFfdyR6rh7

Please consider supporting NEDL on Patreon: www.patreon.com/NEDLeducation

In your equation, you use N = number of trials. However, in a 2018 paper by Macros De Prado (DETECTION OF FALSE INVESTMENT STRATEGIES USING UNSUPERVISED LEARNING METHODS), he mentions that N should be the number of uncorrelated strategies. He estimates this E[K] by clustering correlated strategies. He also uses a different estimate for variance across sharpe.

Am I correctly identifying the difference with this approach?

@@robertsimonuy9743 it just says "number of independent trials", not uncorrelated. Not sure if there's a difference (I haven't studied statistics) but in my mind, two strategies can be run independently yet be highly correlated. I would believe that means you should use 2 and not 1, in that case.

Nevermind, you're more right than I am. I also need to be able to calculate N independent trials out of M, either by clustering or maybe just figuring out the average correlation..

Thank You, Professor! I´m from Brasil and i love your videos!

Ive been trying to learn this for weeks and I had almost given up. Now I can finally implement it properly. Thank you so much!

Incredible! This makes me so happy 😁 ⭐❤️

I believe you're the first person ever - on or outside of RUclips - to make the DSR comprehensible and available to the masses.

Thank you.

Hi Wilton, and thanks so much for the kind words. Glad to digest an academic concept and make it implementable - it is one of the purposes of this channel!

Wonderful teacher, please don't stop dong what you do!

Great video! Just for clarification, because people can get it wrong. If your sharpe ratio star in the probabilistic sharpe ratio procedure is that one you ESTIMATED for the market portfolio, you need to take care of changing the denominator too, in order to account for the standard error (volatility) of your market portfolio sharpe ratio estimate. Otherwise, if it is just an aribitrary scalar value, you can go as it is.

now that I rewatch and understand he actually did this in the video

compliments!

Can we use this for different stocks?

Hi Marouf, and thanks for the question! Yes, if they constitute various investment opportunities you want to select the "best performing" from. Generally these would be applied to portfolios/investment strategies though as hardly ever funds/investors allocate fully towards a single stock.