(EViews10): How to Estimate ARDL Models and Bounds Test

HTML-код

- Опубликовано: 8 сен 2024

- Upon performing the bounds cointegration test, there are two (2) likely outcomes: either the variables are cointegrated or they are not. If the variables are not cointegrated, the next thing to do is to specify the short-run model, which is the autoregressive distributed lag (ARDL) model but if cointegration is the outcome, then the appropriate model to specify is the error or vector error correction model (ECM/VECM) as the case may be. This video details how to estimate the bounds test for cointegration in EViews10 and interpret the results.

Here is the link to the engee2.xlsx dataset used for this tutorial (endeavour to have a Google account for easy accessibility): drive.google.c...

Follow up with soft-notes and updates from CrunchEconometrix:

Website: cruncheconometr...

Blog: cruncheconomet...

Forum: cruncheconometr...

Facebook: / cruncheconometrix

RUclips Custom URL: / cruncheconometrix

Stata Videos Playlist: • (Stata13):Estimate and...

EViews Videos Playlist: • (EViews10):Interpret V...

RUclips recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, help me stay online.

I need help, how can I perform forecast after running ardl model and I have cointegration after bound test I would like do forecast, can I use residual from ardl model and then us it as ec(t-1) in ecm equation. In other words how do forecast after ardl model if cointegration exist. Can't found make model in proc using ardl

I have no idea about this, at the moment.

mis i follow your teaching and i found its really useful thanks for your hard working by the time have question about my bound test F-statistic value is 25.65239 i don't understand why its such big number the data is quarterly data for 12 years is that problem when F-statistic is that high ? thanks in advance

12 years quarterly data gives 48 observations. The higher the F-stat the better the model.

Ma'am, you're highly exceptional in dishing out perfect lecture... Thanks so much

Thanks for the kind words and encouragement, appreciated!

Thank you so much, Ma, for your wonderful explanation. This is just what I needed to continue my research.

You are welcome, Graham 🙏😊

what a clear and pragmatic explanation! Thanks so much

Thanks, Maps for the positive feedback. Deeply appreciated! Please may I know from where (location) you are reaching me?

Thank you professor for the excellent tutorial!

I have two questions:

1) Can we use ARDL if we have variables that are integrated of the same order?

2) Do we perform additional diagnostic tests except the bounds test?

Thank you very much!

Hi Pepe:

1) Yes...if they are ALL I(1). Use OLS if they are ALL I(0).

2) Heteroscedasticity, serial correlation, normality, and stability tests.

@@CrunchEconometrix Thank you!!

Respected Mam,

Why did you run ARDL model directly on log of variables ie. lnmva. Ca we not run ardl on base series.

Hi Dhaval, using the log of a series is at the discretion of the researcher. Regards.

First of all thank you for this explanation. Please how we perform the wald test in the case of ARDL model.

Hi Aiboud, I have never perfomed the WT for my ARDL analyses. You may want to check other online resources. Thanks.

Dear Ngozi,

I want to ask a question about short-run and long-run estimation of coefficients at the time of running ARDL. firstly, if there is no cointrgration, you in your video said ARDL (step-1) gives short-run coefficients. does the same holds true if there is cointegration?

secondly, in case of cointegration, long run form and bound test table (table2) gives the long-run coefficients under the heading level equations, then when we go for Error Correction Form (Table 3) we get cointeq(-1) and there also we find some variables besides counter(-1) what does they indicate? and sometime we get only constant--what does it mean?

regards

Dr Agarwal

Dear Doc, I explained in detail the ARDL-ECM technique in several videos. You may want to watch these videos again. I have several of them to broaden understanding.

Thank you Professor !!!!!

U're welcome, Sir 🥰🙏

Dear Dr. Ngozi. Please do you have a video on Bootstrap ARDL bounds test? I look forward to hearing from you and thank you for doing a fantastic job.

Not at all, but I have noted the suggestion. I'll read up to understand the procedure. Thanks.

@@CrunchEconometrix Thank You Doc.

Madam, I appreciate your clarity of explanation. I am writing a research paper based on your videos. In the F-Bounds Test, along with F-statistic, it is also shown Actual sample, Finite sample size and 10%, 5% and 1%. May I know the meaning of these and when do we use those aspects of the result?.

Hi Manoj, I concern myself with only the F-stat. That is the most important part of the result.

Please may you assist. I am using EVIEWS 13, model is ARDL. I seem to not have the functionalities that you are showing. Example I do not have the long run Cointegration/bounds option. I do have another option which is "Cointegrating Relation" but this does not provide results of the DW test, everything else is there just not the DW test.

I have no idea why that is the case. But does not getting the DW affect your results?

Thank you for the video and for the explanation. I would have a question regarding the short-run coefficients. What does the expession: Z = Z(-1) + D(Z) mean, and how can i get the short-run efficients from this? I would be very grateful for your reply

Hi Charlie, Z(-1) is the 1st lag. D(Z) is the 1st difference. You get this from following the guide shown in my ARDL-ECM videos.

@@CrunchEconometrix Thank you for your reply, Eviews gives me this expression for a variable where the model has selected an optimal lag of 0. How can this then be interpreted and is it still possible to obtain a short-run coefficient? I would be very grateful for your help

Yes, D(Z) is the short-run coefficient.

Thanks for this explanation. Please i would like to know what it means to use unrestricted constant and unrestricted trend (case 5) and how to interpret having the constant and trend in the short run ECM but not having it in the long run. Also, after i am done running the long run and ECM tests, which of them do i run my post diagnostic tests on. Thanks in anticipation.

Hi Angela, thanks for the positive feedback. I use Case 3, you may need to check other online resources about Case 5. Also, I cover diagnostics in my ARDL videos. Kindly watch and follow the steps. Kind regards.

Hi Mam! First of all, I would like to thank you for providing such kind of useful content.

I have a small question regarding trend specification in ARDL bound test approach. How can we select the trend specification? What is the rationale behind this selection?

Hi Kalani, you may include a trend if you visualise (from the graph) that your depvar exhibit such.

Thank you so much for the explanation. While estimating the ARDL my model shows bettter results when I take trend (Case 5) and the trend is also signicficant. If we take trend does the regression that we estimate later using OLS remain the same or it changes?

Please Help

Hi Vella, like I always tell my students: explore your curiosity. Estimate both and compare results. It's the best way to learn.

Nice video Ma. Keep it up. Please, to check for cointegration using long -run and bound test for cointegration, (1). should we compare the f-stats with all the critical values to arrive at a decision or should we compare it specifically to 5% or our desired level of significance?

(2). In a case where the F-stats value is greater than the critical value of the 1(1) bound at say 1% but lower at 5% and 10%. Can we conclude that the variables are cointegrated, despite the fact that the F-stats value is lower than the crivalue value of I(1) at 5 and 10percent? Anticipating your reply Ma

Hi Uche, this video is quite clear and explicit. I explained what needs to be done. You may need to watch again and adapt to your results. Thanks.

Madam, I very much appreciate your videos which are very helpful for writing research articles. Is it possible that you get contradicting results between F-Bounds test and t-bounds tests for a given level of significance? For instance, I got F-statistic value as 4.6194414 with I(0) = 2.86 and I(1)= 4.01. Also t-statistic value is -3.612247 with I(0) = -2.86 and I(1) = -3.99. Thus,. you can see that with F-statistic there is clearly cointegration while with t-statistic, what can I conclude about cointegration? This is at 5% level of significance. Please help me out.

Hi Manoj, always use the F-stat bcos interpretating the t-stat can be confusing due to the negative signs.

Thank Dr for your response.

which views software is appropriate to estimate panel ARDL model.

the example you domesticated here is time series.

Hi Chelsea, in my opinion Stata is more robust for ALL panel data analysis.

Hi ma'am, thanks for making econometrics easy for us😅. Please, if I am using quarterly data, what is the minimum number of years I can use to get a reliable result

Hi Rita, thanks for your encouraging feedback. Deeply appreciated 🙏. Getting good results depends on several factors: scope of data, variables used, empirical approach etc. The standard practice for any research is to have a minimum of 30 observations. This could be 30 years, 30 months, 30 quarters, 30 days etc

Thank you for your video. May I ask two questions:

1.why should we specify the short-run form with the difference value? The ARDL output in Eviews is equation without Difference.

2.And as for independent variables, I found that the generalize form is including the dependent variable itself( means X at t=0),not only have the lag terms.But in this tutorial or even OLS method tutorial both, the present value of independent variables were not included in.

Looking forward to your reply.

Many thanks

Sorry, let me correct question 2.I mean as for independent variables, I found that the generalize form is including the independent variable itself( means X at t=0),not only have the lag terms.But in this tutorial or even OLS method tutorial both, the present value of independent variables were not included in.

Hi Yang, the regressors can appear in the model as in periods t and/or t-i (where i = 1,2,...,T).

Hi prof. I’m really really in need of some guidance.

I’m getting heteroskedasticity in my ARDL model. I watched your video and several other ones and I’ve tried all the ways of changing the specifications to HAC (with condition Auto AIC) and White but it either doesn’t correct my heteroskedasticity or it says I can’t take log of non-positive numbers. What do I do?

Hi Samriddhi, modify the lag structure and re-estimate.

it was more helpful for my understanding.thank u very much.pleace ,let me know how to select lag lenght.i watched your lag selection video,but,there it is done by one by one variable.how i do it in ARDL model.i use annual data.so is it correct if i use lags 2?

Yes, you can use 2 lags for annual data.

Hello prof, it is mentioned in the video that VECM can only be done if 3 equations are cointegrated. Is that mean only 3 cointegrated equations are required or 3 because you have 3 variables. In this case I have 5 variables. Really hope for your answer, thank you

Hi Bella, I never said that. Please watch the clip again to understand why I did an improvised VECM in ARDL.

Thank you So much I have learnt a lot from yours videos, please regarding bound test when you checking cointegration You use 1 lag for both dependent and independent variables is that how it should be or your sample lag was one ? Thanks

Abdirahman, please watch my video on OPTIMAL LAG SELECTION. I chose one-period lag here due to sample size.

@@CrunchEconometrix yes I watch I my data is not all one lag I got some 4 lags and most of them 1 how to do data like that

Abdirahman, you aren't paying attention to my response neither did you when you watched the video on OPTIMAL LAG SELECTION. You may have to make informed decision about your data. Please watch the clip again.

Hi Prof.,

Thank you so much for your clear and instructive tutorials on ARDL, Cointegration and bound tests, they were really helpful.

I have just one question: in the ARDL Model how do we determine the maximum number of lags for both the dependent variable and the regressors. I mean if I have (88) number of observations in (quarterly data) what will be the max. lags to be selected? as the estimation output differs greatly if I chose 4 lags than 8 lags.

Thanks in advance

Hi Hend, I showed how to obtain optimum lags in my ARDL videos. Kindly watch them. Thanks.

@@CrunchEconometrix Thank you professor for your prompt reply but actually my concern is related to determining the Maximum lag in the drop-down box which we specify for E-views to carry out the estimation, not the optimal lag (determined by the E-Views) which you had explained very clearly in the video and it was really helpful. Or should I try the different Maximum lags found in the drop-down box (from 1 to 12) and then choose the lowest information criteria among them? or just accept the default lagnumber provided by the E-views which is 4?. Thanks a lot.

May God bless you for this ma! I needed this for my research project. Quick question though: at 2:58, why did you change the default Max lags from 4 to 1? My study's scope is also 34 years.

Thanks for the encouraging feedback...deeply appreciated. I changed the lags from 4 to 1 to avoid losing too many observations that will negatively impact the degrees of freedom.

Thank you Dr. Bosede Ngozi Adeleye for your amazing explanation in econometric. I just have one query. Can u please explain me the difference between Constant and restricted constant? I am running ARDL model. But when I am taking unrestricted constant (model 3 in eviews 10) in my analysis there is inconclusive results in long run and bound test unlike taking restricted constant then there is cointegration among the variables. Can I take restricted constant?

Hi Gholam, the explanation is a bit technical, to be honest. But if you get a good result with "restricted" constant, I suggest that you go with that. Please may I know from where (location) you are reaching me?

Thanks, I am from Kolkata, India.

hello ma, thank you for the video. pls i wanted to ask if we necessarily have to use the log of a variable

Hi Susan, not exactly. You have the sole discretion on the functional form of the model to deploy. However, using the log form has several benefits. You can check online for more on using natural logarithms. I have detailed videos on FUNCTIONAL FORMS on my Teachable paid platform cruncheconometrix.teachable.com

Hi Dr. I have some questions.

1. How to know the max lag for the dependant and the regressor?

2. How to know when to change the Fixed regressor trend specifications?

3. If the variable for example is I (1), to include it into the estimation, do we need to difference the variable first (make new data), before regress or just use the raw variables data?

Thank you very much in advance.

Hi Nikmat, all your questions have been answered in my ARDL videos. Please watch them ALL, load your data, follow my procedures and replicate. Thanks.

@@CrunchEconometrix all right Dr. Thank you very much. Best regards.

Is 30 years of observation required to conduct ARDL? I have 23 years of time series data. Is it okay to conduct ARDL with it??

Ritu, it's at least 30 observations. The application of lag length to the model reduces the number of observations.

Hi Prof.

Thank you for the demonstration. I would like to ask what it means when you have the coefficient for the Error Correction term to be positive when the ARDL is used and re-modelled

Hi Kweku, it means there's no reversion to long run equilibrium. Model diverges. Explosive.

@@CrunchEconometrix Thank you very much Prof.

U are welcome, Sir 🙏

Ma'am if we variables which we have into percentage chnages then log then at we should run the ardl

No need to log such variables.

Thank you ma’am. I tried to run a ARDL model and my target was to show the long run relationship between CO2 emission and economic growth. I have found perfect result. Now when I start writing my paper, I am facing a problem.

I have checked he diagnostic tests for

1. ARDL model

2. Short run model

3. Long run model

4. Error correction model

Which diagnostic tests, I should keep in my paper? The ARDL ones? The short run ones? The long run ones? The error correction model ones?

Hi Afia, check my Community Tab for any of my ARDL papers (or any ARDL publication) and adapt the diagnostics. Thanks.

hello

if the variables are not cointegreted,and all i need is to interpret the signes of the coefficiens is that mean that the ardl model is not significant and i can't interpret the signes ?

if the f bound test result is diferent from the t bound test what can i say ?

Yes Ayoub. Estimate ARDL if no cointegration. In regression Analysis generally, insignificant coefficients are not interpreted because they are equal to zero. The exception to that is when the key explvar is not significant and in that case, you have to mention/discuss it.

@@CrunchEconometrix what do you mean by the key explvar ?

@@ayoubsakhi3062 Essential. Not a control variable.

Thank you so much for your videos they are really useful, I've a question concerning the ECM (ARDL model), when I do the ECM it drops one variable (the dependent variable) from short-run coefficients so what should we do to know its short-run coefficient and why it is dropped?

Fayrouz, thanks for the positive feedback. Deeply appreciated. How can the depvar be dropped from a model? I don't understand this.

@@CrunchEconometrix It was not dropped in the ARDL but it didn't appear in the short-run coefficients of the ECM. Can you help me with how to solve this?

I have responded to you on a different thread.

hi , first think you

Cointegration rank applies to Johansen cointegration test. Not applicable to ARDL model but VAR/VECM.

Nice video again, Prof. I just have a question: Can ARDL be estimated if your variable is stationary after second difference alone? That is I (2)

No, Kehinde. ARDL is not applicable with I(2) variables.

@@CrunchEconometrix Hi prof! does it work if I take the natural log of the variable (in my case: CPI of India) and then it becomes an I(1) process?

Hi Samriddhi, sure you can.

Hello Dear Prof. Ngozi Adeleye,

I hope my text finds you happy and healthy.

I have conducted the ARDL model, in the long-run and short-run.

In the long-run model, the results are okay. But in the short run model the variables are omitted from the model, just the variables are kept in the model which are statistically significant.

So, Kindly, could you help me what is the reason?

Hi Sherzad, when SR coefficients don't appear in the ECT model it is because they have contemporaneous effect on the depvar. That is, they have 0 lags.

@@CrunchEconometrix Many thanks, your video and support are highly appreciated.

@@CrunchEconometrix Kindly, could you provide me a justification for the above explanation?

Sherzad, do a Google search query on contemporaneous relationships for articles and other online resources to support your work. I have pointed you in the right direction. Do the rest for more informed learning. Thanks.

@@CrunchEconometrix Dear Prof. Ngozi Adeleye, many thanks, I really appreciate your support.

thanks a lot. pls how do I remove serial correlation from ardl model. if you have a video let me know

Edward, several ways. Adjust the lags, drop/replace explvars.

Madam, I very much appreciate your prompt response to the questions posed by all the learners. I have a question. My ARDL (1, 1, 1,1, 0) model (with fixed regressor Trend specification as CONSTANT), has the variables gdp, gfc, labour, reneng, nonreneng with gdp being the dependent variable. With this model when I went for the ARDL long run form and Bounds Test (in the conditional error correction regression Output), the term D(nonreneng) was missing. However, I got the output only for C, gdp(-1), gfc(-1), labour(-1), reneng(-1), nonreneng(-1), D(gfc), D(labour) and D(reneng). Why is this so? I need to specify the Short-Run Dynamic ECT Model which should contain all the D terms of the independent variables. I am using Eviews 10 student version. Please clear my doubt.

D(nonreneng) is missing because it has 0 lag from your indicated lag structure.

From Nairobi Kenya with greetings Madam.Thanks Madam for your great assistance on ARDL Models. I have gone through all your ARDL models and they are very helpful. i have followed you all along. I want to estimate long run and short run coefficients effect of ARDL model. should i use the ECM model or how do i go about it

Hi Ngugi, thanks for watching my videos and the positive feedback. But your query is conflicting because I have shown and explained short- and long-run ARDL estimates. You may need to watch them again, thanks.

Hi Ngugi, thanks for watching my videos and the positive feedback. But your query is conflicting because I have shown and explained short- and long-run ARDL estimates. You may need to watch them again, thanks.

Great Work

Thanks Imtiaz!!!

Dear madam, first of all, thank you so much for your informative videos, but I have a question.

If I have chosen to use the ARDL approach in my study, do I still need to run the Johanson Juselius cointegration test?

Or can I just run the Unit Root Test and the ARDL test like the video shown?

Hi and thanks for the positive feedback. Deeply appreciated...and no, JCT is not required for ARDL technique.

@@CrunchEconometrix Thank you Madam for the reply. And I have one more question regarding ARDL. If I got no cointegration in the bound test, does it means I can just stop there and straight to the conclusion, no need to go for the ARDL-ECM part?

I have read your research, namely "Financial reforms and credit growth in Nigeria: empirical insights from ARDL and ECM techniques". In my case with no cointegration, is it means that I can just stop at the 4.2 Bound test and then proceed to the conclusion, no need to go for the 4.3 and 4.4?

Estimate the unrestricted ARDL if there's no cointegration... Not the ECM (restricted ARDL).

@@CrunchEconometrix Noted. Thank you so much, Madam. This helps a lot.

Hi ma'am! I have sequentially followed your video and got a short run relationship between the variables. Ma'am can you suggest me some literatures where I can get the exact model description that you have suggested in the video?

Kamikaa, see references indicated at the end of the video and other online resources.

great works indeed! btw, one confusion is that i am working with 8 variables, to decide VECM or ARDL, is it needed to have 8 co integrating equations to use VECM? or presence of more than one cointegration equation is enough to go for VECM and testing johansen cointegration? do I need to check all those 8 as dependent variable forming equation for all?

Thanks Asmaul, for the positive feedback on my RUclips videos. Deeply appreciated! However, you have muddled up your queries. Besides, ARDL and VAR are different techniques. I will advise you watch ALL my videos on both and decide which one to adopt. May I know from where (location) you are reaching me?

Hi @CrunchEconometrix let say I'm estimating the model with ARDL (4,1,0,0,3) with quarterly data how would i determine the number of period for short run causality and number of period for long run causality?

Hi Patrick, please watch my videos on Causality and follow the guides.

How do you select trend specification?Is it automatically selected??

Hi Mukti, not automatic. You indicate "trend".

Hello Dr,

Please which Eviews software package is appropriate for ARDL estimation--- which software packing did you use for this analysis--

Is it Eviews 10 University Edition or is it Eviews 10 professional or which type?

Thank you , hope to hear from you soon.

Not sure which. It was installed by a colleague several years ago.

Mam please upload video of BDS test for non linearity ( in Eviews)

Hi Diyyala, thanks for the suggestion but I have no idea what BDS is. Thanks

Professor thanks for the video.. In some video i saw they use the 1st difference of the variable at the 1st step for constructing of ARDL model. What should we do?? Can we use the 1st difference or the level form for ARDL model?

Bela, please re-watch this clip. I explained the conditions for using ARDL.

My name is Ahmed, I am a student and in my research work I have used the ARDL approach.

I have a delicate question!

I used 5 variables and after applying the stationarity, ADF and PP tests, I found that the dependent variable is I(0) and all the explanatory variables are I(1) in my model.

In this case, is there a problem with my estimated model?

Hi Ahmed, there is nothing wrong with your model. Pesaran and Shin (1998) and Pesaran, Shin, and Smith (2001) are not explicit on the status of the depvar. Though for cointegration, it is expected that the depvar is I(1). I have seen papers use ARDL with an I(0) depvar (mine inclusive). So, I will say that you can proceed with your analysis. Thanks.

@@CrunchEconometrix thank you for this clarification

More than 4 independent variable how i run ardl bound test?please tell me

Same way I showed how to perform Bounds test. Number of variables is immaterial.

This is a great video.

Hi BiY, thanks for the positive feedback on my video. Deeply appreciated!😃 May I know from where (location) you are reaching me?

@@CrunchEconometrix New Zealand.

@@spinebuster9490 Wow! Kindly spread the word about my videos and RUclips Channel to your friends, students and academic community in New Zealand for awareness. They'll learn some useful tips and hints too😃

Hello Prof, i noticed some typo in some of your equations ma, thought i should bring it to your attention. E.g. the long run is t-1, but you sometimes write t-i, which is for short run and should be summed.

Yes Ade, those are typos. I had uploaded before noticing the errors. Should be t-1 and not t-i. Thanks for the observation. May I know from where (location) you are reaching me?

Madam i have a query

If in var most of the criterion supports 3 lags then is it necessary when applying ardl i have to select 3 lags for both dependent variable and regressors .

Hi Waqas, for ARDL model you MUST select the lags separately for the variables. Please watch the prerequisite video "This is how to specify ARDL Model" for proper guide on the ARDL model. Thanks.

Greetings CrunchEconometrix, could you please specify, steps by steps, the procedure to follow, and the diagnostic tests to perform, when you are running ARDL models. Thank you.

Hi Iddriss, the steps are adequately covered in my ARDL videos. Kindly browse thru the Playlists. Thanks.

Hello, crunch econometrix, thank you so much for decent interpretations on econometrix modelling. It's really useful.

I have one question please, how we gonna apply cointegration test on Panel Ardl model (pmg) model ? And short and long run causalities?

Thanks in advance

Enkhtuvshin Ganbaatar Hi Enk, thanks for the kind words and encouragement. From PSS (1997,1999) Cointegration is inferred from the statistical significance of the ECT. But you can further apply Pedroni and/or Westerlund tests if you so wish. Likewise, long and short-run causalities are inferred from the statistical significance of the regressors.

CrunchEconometrix thank you very much. Will try to apply pedroni and kao tests, but my variables are mixed with I0 and I1, so I'm not sure to pedroni is appropriate. Since eviews doesn't support westerlund cointegration test.

What are the steps? first specify ARDL then bounds test then choose to use model ARDL or VECM?

Am I correct to say that there is no way to check bounds test without making ARDL model with your variables in EVIEWS? It is a bit hard to find the right structure for my thesis

Yes, you are correct.

@@CrunchEconometrix and is breakpoint analysis required prior ARDL specification?

@@TheEnyoy You can test if you wish to.

Hi, thank you for the help ! I have a question from the beginning I don't know whether to use the log(price) or the log(return)? Because when running the long run relationship using the log(return), the variable will be differentiated again no ? so using log(return) can be problematic + I will find all variable stationary at level please I need help thank you !

Hi Meriem, unfortunately I can't decide for you. This is your research. Price and return are related. Check what similar studies used and take your decision. Thanks.

Hello Thank you for your video. Can you tell me if I can run error correction model if I find that I have mixture of stationary? I'm working with Panel data

Hi Ibrahim, not an ECM per se but a heterogeneous dynamic panel model using PMG, MG and DFE estimators. I have videos on them but using Stata not EViews. But watch my video on "Basics of Panel ARDL". It's quite detailed to guide you on what to do.

great .Hello Prof. I have one question concerning ARDL model using Eviews 9. My question is how can we analyze the long run diagnostic test? I have got the coefficients of long run form. The short run diagnostic is simply I have no question for this. I need separtate autocorrelation , heteroskedasticity, and normally test for short run and long run.

Regards

Hi Girum, your queries are confusing. Please be explicit so I can guide you correctly.

Hello madam, having known that for a VECM to be used, all variables must be endogenous. However, is it compulsory, that for this model to be used, each of the variables must be modelled on others, i.e if the variables are three, then three models must be constructed, and if so, do we also have to carry out the VECM estimation of all these equations and necessary tests on them all?

Hi Tunde, remember that this is an ARDL model not VAR and if you had listened to my explanations, the assumption of all variables being endogenous does not apply. ARDL is a single-equation model and I explained that I only used this VECM approach to show that a vector of equations can be constructed from an ARDL model. As a researcher, you can always make your own assumptions.

i get you, i actually got this question having listened to your VECM estimation, sorry that am asking for the answer under a different thread which is ARDL, but the question is actually for VECM, kindly address it as asked, thanks madam

@@olatundeadex1052 Ok, but you got it all mixed up. For you to understand VECM, you must first understand a VAR model, its assumptions and specifications. I'll advise that you watch my videos on VAR because I addressed all your queries. It is always helpful to jot down some points because you have a lot to take in. If you still further queries, post them in the appropriate comment section of the respective video, and I'll respond from there.

Madam, Please tell me the source (in the form of say pdf) where I can find the critical values table for I(0) and I(1) for Narayan and Pesaran.

It's available on the internet. Just search and u'll find it.

Hello, why did you choose max lag as 1, what is the criteria for choosing max lags for dependent variables and regressors in ARDL

Kindly watch my video on "Optimal lag selection". You will find it very informative. Thanks.

Hi

Thanks for your informative videos

Why do you choose just 1lag to test the cointegration while the optimum lag for these variables is another number as you calculated ? I would appreciate if you elaborate on this issue

Amir, I allowed EViews to choose the optimal lags(1,0,0) see the result Table. All I did was to modify the default lags lags of 4 to 1 and I gave the reasons why (only 34 observations and not to lose too many degrees of freedom). I could still use 2 lags if I wanted to. Thanks for watching and hope that you'll share my videos with your students and colleagues :)

Thank u so much. If my f stastics above the upper limit and t statistics below the lower limit or vice versa, what kind of conclusion I could made, please?

Munshir, use the F-stat to avoid confusing yourself. Very straightforward.

@@CrunchEconometrix ok thank u for clarification

@@CrunchEconometrix Dear mam, couldnt see its continuous video...

Hi Munshir, which continuation video?

hi mam, continuation of estimating ARDL models in eviews (5). I reached up to this video. Now, I want to proceed to estimate ARDL and ECM

Hi, thank you for the vid. I would like to ask while equation estimation, why you cannot use default lag 4 and change to lag 1?( you mention that you only have 34 years data) for example, if i use 60 months data, it is okay for me to change to lag 6 since im using monthly data?

Hi Siti, kindly watch my video on "Optimal lag selection". Tx

the Log of variables is essential before apply ARDL ?

Taking log is at the discretion of the researcher.

@@CrunchEconometrix Thnx Ma'am

Thank you so much. I have a question that how can i include control variable while estimating ardl model? For example i have one dependent variable which is cpi and one independent variable which is oil price and one control variable which is broad money supply.

Waleed, contvars are treated the same way as explvars. Put them in the model and interpret your results.

Thank u mam. Last question, what happened or how do you report your short run relation when some IVs disappeared in the ECM regression result. Does it mean that the missing variables have no short run impact on the DV?

Yes, that's the interpretation.

Hello madam! Thank you for such an informative and helpful video. I have a small query - when you applied ardl bound test with Unrestricted Constant and no trend using log of IMP as the dependent variable, the F statistic that u obtained was 5.86 which is less than the Critical values at 10%, 5%, and 2.5% and u said that a cointegration relation exists. But at one percent the critical value is higher than the f statistic as it is 6.36%. So I want to ask if its a necessary condition that all I(1) upper bound critical values at various level of significance must be below the value of F-statistic to reject the null hypothesis of no cointegration??

Hi Saima, thanks for the positive feedback. Deeply appreciated. Please watch the video again because you are mixing up the decision criteria. You reject the null hypothesis of no cointegration if the F-stat is higher than the I(1) upper bound at the 1% OR 5% OR 10% significant levels.

@@CrunchEconometrix Got it. It's clear now. Thank you so much for your response!

Hello Prof, at 2:35 why the equation do not contain any I(1) variable ? Are all the variable stationary at level I(0) so you do not put any d(variable) there ?

That's the specification for ARDL models.

Thank you prof, one more question. If my result shows no cointegration, and I perform OLS to find short-run, then should I use variable in difference I(1) and level I(0) according to the stationary test of each variable ? Or should I use all the variable to be stationary at I(1)?

I showed detailed steps. Kindly follow.

Hello! Thanks again for your videos.

When I run the bounds test on my data, the F statistic is clearly above the I(1) critical value, however the T statistic lies in between the I(0) and I(1) critical values, so what does that mean? Are my variables cointegrated or not? To be honest I still don’t understand very well how the T test works for the ARDL Bounds test and what does it measure exactly.

Hi Raymundo, relax and follow my lead. Use the F-stats. Search through the literature to observe that the T-stat is rarely used in the Bounds test compared to the F-stat.

Hello. How about to run it in Stata. and what if I have only 30 observations ?

Mahir, go ahead but use only ONE period lag to avoid loss of degrees of freedom.

@@CrunchEconometrix could you pls elaborate

Mahir, kindly watch my video on OPTIMAL LAG SELECTION for clarity. Thanks

Hello, what coefficient values should I use here, the ones specified under Conditional Error Correction Regression or the ones in Levels Equation (Restricted constant and no trend)? Thanks.

Hi Vlado, what you need is the F-stat of the Bounds test (not the coefficient values) as I explained.

From these results, how would you obtain the long run equation and the short run equation? Thank you

Hi Tom, my videos are well-explained so, you need to watch the entire series to know the long-run and short-run results. The 1stseries shows how to specify an ARDL model. The 2nd which is this clip shows how to perform cointegration using the Bounds test. The 3rd clip shows how to obtain the short- (ARDL) and long-run (ECM) results. The videos are interwoven so you need to watch all and jot down some notes while at it. You may need to watch them again to fully understand the procedure and results interpretation. Hope these are helpful, thanks.

You have selected 1 lag here as default instead of the default 4 lags because you have only 34 years data.

Dear ma’am, if you had selected 3 lags or 4 lags as default, your optimal lag might have been different ( I mean it might not have appeared as 1, 0, 0).

I am also working on annual data and I do have only 34 years data just like your case. My question is

1. Should I select 1 or 2 lags as default instead of default 4 lags or not?

2. Why do you suggest to keep it lower here? Is it because it might cause serial correlation?

I will be really great full to you if you kindly answer to my questions. I am from Bangladesh and I am a faculty of one of the prestigious university here.

Hi Rafa, using lags is not an issue. Based on your 34 obs you can use between 1 to 4...most times, I allow EViews determine the optimal lags for the model.

Good day Dr. I estimated an ARDL model which the result came out with the R-squared greater that the durbin-watson stat. the cusum and cusumsq seems ok. the serial correlation and heteroskedasticity test all seem ok. i was very concerned about the r-squared and dubin watson stat. what do i do? should i continue with the analysis?

Hi Kenechukwu, that's a spurious regression. Test for unit root, use appropriate lags and re-estimate the model.

Thank youuuuuuuu

U are so welcome, Mimi!!!🥰

Hello Dr. I have some question

If dependent variable and Indepentdent variable are I(0) I(1) when I generate optimal lag, Can I formulate y c x1 x2 x3 d(x4) d(x5)?

Chanyaphat, my procedure is quite clear. I showed what to do. So, kindly follow. Thanks.

Hi, thank you for your videos they are very useful. I have a question. I am using ARDL model and ECM when appropriate. When I do the long run form and bound test it gives me the parameter of the cointegration equation in the ECT, however I want to show the intercept of this term. Should I chose the case 2) restricted constant instead of case 3) unrestricted constant and no trend to get the intercept? Or which is the intercept of the ECT?

Thank you for your help

Hi Monica, try both and observe your findings. May I know from where (location) you are reaching me?

@@CrunchEconometrix Thank you, I did that and by using the case 2 of restricted constant just adds the coefficient of the constant and the other coefficient remains intact. I'm looking at your videos from UK. But then to find if it has serial correlation and stability should I look at it using case 2 or 3 or it wont matter?

@@monicaguevara770 You have to stick with a particular case for consistency.

first of all, thank you.

your channel was very very helpful ...

have urgent q,

one of my variables was stationery at second level can I transform that variable then estimate ARDL?

thank you again

Hi Bayan,thanks for the kind comments and good to hear that my YT channel is helpful in some ways to you. But no, if the series is I(2) don't use it. It is advisable to drop/change such and use a closely related proxy that best capture the indicator.

please how do you know what maximum lag to use?

Iwasam, kindly watch my video on OPTIMAL LAG SELECTION for guide. Thanks.

Hello madam, my data unit root test stationer at 1st difference, no stationer at level. so which should I input in the ardl equation? variable or D(variable). I'm confused with this video and your next video which calculating ardl with OLS? here you input variable over there you use d(variable)

Hi, there is nothing to be confused about. ARDL model can be estimated using the ARDL or OLS estimator...that's why the videos are different. Use any approach.

@@CrunchEconometrix thx u for responding. so, if I approach with ardl methods like in your videos, I use variable data? and if I use the ols methods I use the d(variables)?

@@user-fc4ol1jd7o Exactly.

Hello. I have 2 questions to ask you:

1. For the short run causal effect, is the coefficient for the explanatory variable obtained from the “Conditional Error Correction Regression” table or the “Levels Equation” table? How do you interpret the value of the coefficient?

2. For the long run causal effect, is it correct to see the value of the coefficient from the "Conditional Error Correction Regression? How do you interpret it? Which one shows the speed of adjustment and how would you interpret the speed of adjustment?

Also, may I ask the name of the books and or journals that you are using as references? That would help a lot, thank you.

Hi Michael, hope you're doing gr8! To your enquiry:

1) (a)short-causal effects are obtained from the estimates of the ARDL model, which is the short-run model and that is what is estimated first.

(b) Interpretation is simply the "ceteris paribus" argument. For instance using the LNIMP equation, a percentage change in mva results in 0.026% change in imports, on average ceteris paribus.

2) (a) long-run causal effects are obtained from the long-run equation and the results are those shown in the "Level equation" table using Case 3 as specified in the model configuration.

(b) In the "Level equation" table, the ECT equation is stated...but since EViews did not calculate it from there, I don't know why you should (lol)

(c) So, click on "View" and select "Error correction form" to obtain the ECT and the respective speed of adjustment (SoA) coefficient

(d) Interpretation of SoA coefficient (an example): this indicates that adjustment to long-run equilibrium is at a speed rate of 12% OR the previous period's errors will be corrected at a speed of 12% in the current period.

3) Resources used are Gujarati's Basic Econometrics; Wooldridge's Introductory Econometrics:

Other materials are journal articles such as:

1. Ngozi Adeleye, Evans Osabuohien, Ebenezer Bowale, Oluwatoyin Matthew & Emmanuel Oduntan (2017): Financial reforms and credit growth in Nigeria: empirical insights from ARDL and ECM techniques, International Review of Applied Economics, DOI: 10.1080/02692171.2017.1375466

2. Belloumi, Mounir (2014). “The Relationship between Trade, FDI and Economic Growth in Tunisia: An Application of the Autoregressive Distributed Lag Model.” Economic Systems 38 (2): 269-287.

3. Kripfganz, Sebastian, and Daniel C. Schneider (2016). “ARDL: Stata Module to Estimate Autoregressive Distributed Lag Models.” Stata Conference, Chicago, July 29.

4. Narayan, Paresh Kumar (2004). “Reformulating Critical Values for the Bounds F -statictics Approach to Cointegration: An Application to the Tourism Demand Model for Fiji.” Department of Economics Discussion Papers No. 02/04, Monash University, Melbourne, Australia.

5. Pesaran, M. Hashem, Yongcheol Shin, and Ron P. Smith (2001). “Bounds Testing Approaches to the Analysis of Level Relationship.” Journal of Applied Econometrics 16: 289-326.

...and so tons of papers on the ARDL and ECM techniques. Hope these tips are helpful.

It is very helpful indeed. Thank you so much mate.

I just have a couple of questions.

1. If there are two variables (1 dependent and 1 exogenous) which are both I(1), should I use Johansen Cointegration or can I also use the ARDL Cointegration and Bounds Test? What about if the two variables are I(0)? What cointegration test should I use?

2. Also, can I use the Granger Causality Test option on Eviews test to check the direction of causality after testing the cointegration with ARDL and Bounds Test? Do I need to or is it not legitimate based on previous studies on books and journals?

Thank you so much, sorry for the amount of questions.

Hi Michael, for ques (1) You may look up the EViews playlist for the videos relating to these. I have them. Ques (2), you can do Granger causality if it's part of your research argument.

Hello Dr. Ngozi, I have been replicating your tutorial on ARDL estimation on the analysis I am running. However, in one of my variables, the F-statistic fell between the lower bound and higher bound. it is inconclusive. what then do I do in this case?

You can do any or combination of these 3 things: 1) estimate the ARDL model, or 2) change/include more regressors and re-estimate, or 3) take logs.

HI....nice it is really helpful ......i need references for that model specification which u explained ...can i get that...

You can reference PSS or any paper that used the ARDL. look for Adeleye et al (2018) Financial reforms and credit growth paper. Thanks.

@@CrunchEconometrix thank you..

Hi, I was facing a question regarding the bounds test. What if fbounds says cointegration while tbounds says no cointegration?

It's very rare for a contradiction to occur...and where it does, you take the F-stat.

I think you should assign numbers to the vidios for sequence.

Hi Javed, thanks for the suggestion but I won't be able to do that because my videos are randomly made. For easy access, I have sorted my videos into 9 Playlists indicating the software used and data structure. Viewers can easily watch any clip once they identify what they need. Thanks anyways. May I know from where (location) you are reaching me?

Ps. Is as covariance method using Newey-West better than ordinary?

I have no idea what you are referring to.

starting from 9:10 madam, in the second bullet, do you mean cointegration from the three "variables" (given as specific dependent variable already) instead of "equations"?

Nope Herman, VECM should be specified if there's cointegration from the 3 equations not variables....as rightly explained. Note that cointegration among the 3 variables is obtained from one equation, hence an ECM model not a VECM.

@@CrunchEconometrix thanks!

@@CrunchEconometrix hi professor! your videos are easily understandable and appealing. your replies are very helpful as well.

i have another question madam: I have read journals and even your example has a negative and significant ECT that explains the speed of adjustments. in all the references that i see, the ECT does not exceed 1.00 and is interpreted in percent. now, how can an ECT coefficient of -1.15 be explained? thank you very much madam. i am currently working on a quarterly data and have followed all your instructions as well as your replies from previous inquiries.

Good to know Hernan, and I'm glad to be of help. Yes, any ECT value not lower than -2 is still acceptable. The root of the model still lies within the unit circle. See my paper Adeleye et al (2018) - Financial reforms and credit growth in Nigeria: Empirical insights from of ARDL and ECM techniques. Please tell your colleagues about my Channel...thanks!!!

Hello Dr. i'm a little bit confused about the the difference between the constant and restricted constant in the ARDL model. my data does not require to include restricted trend, constant and trend or none, only it requires a constant and i can't tell weather to choose/ include the restricted constant or just constant.

Hi Yasin, apologies for the late response. There are different assumption regarding when to use these options. You will have to read other references to know more. May I know from where (location) you are reaching me?

@@CrunchEconometrix well understood Dr. I'm a Somali student in Malaysia.

@@Yasin-bq5pn Awesome! Please spread the word about my videos to your students, friends and academic community in Somalia 🇸🇴 and Malaysia 🇲🇾 for awareness. They'll learn some useful tips and skills too...thanks 😊

dear ADELEYE,

i come back to you again for help.

i have run my bounds test and found cointegration since f-statistics was beyond the upper bound. so i moved on to estimate short-run and Long-run coefficients through the command ( long-run form and bounds test) and i get large coefficients provided that the model passed all tests ( LM, Qusum, etc). knowing that i transformed them into log. thanks

Coefficient

Variable A -23.75811

Variable B 29.87796

Variable C 4.429029

Variable D 40.56010

Variable E -43.58716

Variable F 0.690199

Variable G -19.99185

Constant 318.7827

Hi Belfqih, a log-log model should not give such high coefficients. Something is definitely wrong with your data.

@@CrunchEconometrix hi professor my dependent variable is numerical (volume of yearly export) and my explanatory variables are under the form of yearly scores (from 0 to 10). Could it be this mixed type of variables that causes such high coefficients.

@@belfqihhamza1632 Most likely. Can't say precisely.

@@CrunchEconometrix thank you very much

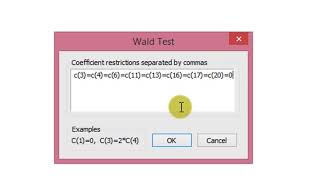

Hi, thanks a lot for these videos, they are extremely useful, but in my research, I have a problem in Wald Test especially in the comma-separated coefficient restrictions box help me please

Hi Maaroufi, thanks for the positive feedback on my videos. Deeply appreciated! But I don't quite understand your query which is not related to this video. Better to use the appropriate video thread. May I know from where (location) you are reaching me?

From Tunisia

@@maaroufiahmed4982 Awesome Maaroufi...kindly share my RUclips Channel link with your students and academic community in Tunisia 🇹🇳! 💕 😊

Hello, thank you for your videos they are very helpful, i have one question for this one, during bounds test if my F-statistic is between I(0) and I(1) for 5% significance what should i do?

Hi Giorgi, thanks for the positive feedback on my videos. Deeply appreciated! 💕 It means inconclusive. Estimate the short run model. May I know from where (location) you are reaching me?

@@CrunchEconometrix thank you for your answer. From France.

@@giorgikiladze4805 No worries, Giorgi...I'll appreciate it if you can help share my link with your friends, students and academic community in France 🇫🇷 and on social media for awareness. They'll learn some useful tips and skills too. Merci! 💕

Dear Madam, I have two questions. 1. Why you use max lag 1 in both dependent and independent variable?? 2. Why you consider unrestricted constant and no trend??

Hi Tauhidur, I explained why I did that: I only have 30 years data. Option 3 is the most flexible and that's why I use it. U can seek more online information regarding the different options and when to use them. May I know from where (location) you are reaching me?

@@CrunchEconometrix thanks

@@tauhidurrahman3686 U're welcome 😊. May I know from where (location) you are reaching me?

@@CrunchEconometrix I'm from Bangladesh

@@CrunchEconometrix dependent variable max lags 1, regressors max lags 1. It is subjective to set 1, 1 lag?? sorry madam I m not clear about this.

Hi, thank you so much for these videos they are extremely helpful. I was wondering if you could kindly answer my urgent question which I would be very grateful for. I was wondering when we estimate the first stage ARDL (min 3:36 of your video), and find significant lags, can we interpret them as anything useful?? e.g. the lag of exchange has a positive effect on lnmva (given that I have checked lack of serial correlation and heteroscedasticy). Or does the first stage ARDL not give us anything useful? Additionally, if I dont find cointegration, for short term dynamics, is it completely necessary to take differnces? I thank you in advance for your time, your help would be greately appreciated.

Hi Atousa, thanks for the kind remarks on my videos, they are humbly appreciated. On your queries, yes you can interpret the ARDL results (these are short-run estimates). And if there is no cointegration, estimate only the ARDL model. The issue of differencing does not arise. Thanks.

Thank you so so much for your respond, I will be recommending this channel to everyone I know! Just to confirm, using AIC and just estimating the normal ARDL as you do in min 3.36 (without taking differences) is giving us the short term dynamics?

Im sorry if this is a silly question, it is just something Im very confused about as everyone seems to take differences even for short-term dynamics (as you do in the next video as well)

Thank you so so much again.

There's no silly question Atousa and believe me, I don't have all answers to econometrics queries. My knowledge is limited to the stuffs I know. If you had closely followed the procedures, you'll see that ARDL (1,0,0) was automatically chosen by EViews not me which shows that you can estimates variables in levels and not only in 1st difference when using the ARDL model.

CrunchEconometrix hello professor

So why do u use the first difference of the variables and don't use them in levels in the video of ARDL and ecm to estimate the short run model, I can say I've been watching your videos 100 times and every time I understand something new and find a new question

Could you please elaborate on this issue?

Thanks in advance

@@CrunchEconometrix Hi Madam, just to get more understanding that if I got no cointegration in the bound test, does it means I can just stop there and straight to the conclusion, no need to go for the. ARDL-ECM part?

I have read your research, namely Financial reforms and credit growth in Nigeria: empirical insights from ARDL and ECM techniques. In my case with no cointegration, is it means that I can just stop at the 4.2 Bound test and then proceed to the conclusion, no need to go for the 4.3 and 4.4?

Hi, i have issue in Eview 10, not find the bound test command bar.

Hi Muhd, follow my procedure to see how to locate "bound test" program. Thanks.

HI!

if the optimal lag is 5 for the dependent variable and there is a long-run relationship using the f-bounds test, what will be the number of lags for the ECM? i mean is "1" is constant or i will use "5" lags as well? thanks a lot.

Hi Heman, the ECT is always with 1 lag irrespective of the number of lags of the depvar....and thanks for watching my videos. Please share with your friends and students too! Gracias! 💕

or do i include ECM(-1) to ECM(-5) thanks a lot madam

@@CrunchEconometrix than you very much

@@CrunchEconometrix Another question madam: my DV has 5 lags. I have 4 independent vars. in the least square estimations, shall all the IVs have 1st to 5th lag? i appreciate your prompt replies. this is how it looks

Ln_prod c d(Ln_prod(-1)) d(Ln_prod(-2)) d(Ln_prod(-3)) d(Ln_prod(-4)) d(Ln_prod(-5)) D(ln_temp(-1)) D(ln_temp(-2)) D(ln_temp(-3)) D(ln_temp(-4)) D(ln_temp(-5)) D(ln_precip(-1)) D(ln_precip(-2)) D(ln_precip(-3)) D(ln_precip(-4)) D(ln_precip(-5)) D(ln_co2(-1)) D(ln_co2(-2)) D(ln_co2(-3)) D(ln_co2(-4)) D(ln_co2(-5)) D(ln_sst(-1)) D(ln_sst(-2)) D(ln_sst(-3)) D(ln_sst(-4)) D(ln_sst(-5)) D(ln_wwv(-1)) D(ln_wwv(-2)) D(ln_wwv(-3)) D(ln_wwv(-4)) D(ln_wwv(-5)) ecm(-1)

@@phg0922 Hi Heman, please I'll suggest you watch all the videos on ARDL. You MUST start with the video on "This is how to specify ARDL models". All the answers to your questions are not in one video but covered in others. So, please watch them and jot some points while doing so. You'll be more confident after that. Thanks.

Logged the variable price series have mandatory for running the ARDL method or not?

Hi Suresh, kindly rephrase question. I don't understand what you mean.

@@CrunchEconometrix For applying the ARDL test, the original price (time series) are converted into log or not?

@@CrunchEconometrix, we run the ARDL model on original price series or log price series?

@@SureshKumar-qq1yk You can use either to estimate the model.

@@SureshKumar-qq1yk Either is appropriate.