SIr, your ability to explain such concepts, in such a beautifully intuitive manner, to a rather slow retired Banker (e.g. 3 year old child) is something to behold! Thank you (my happy hour today will be a little happier).

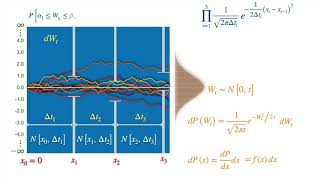

Thank you for your explanation, it is very intuitive to understand the logic. Can I ask one question? At time 20:32, what is the meaning of x0, x1, ... here? Is my following understanding correct? For example, if I bet 1$ on the green, if I win, I will get 4$. But right now I can get extra some money, so I may get 4$ plus say 10$ = 14$. Now I standardize the price, it will be 1/14, which means I pay 1/14$ on green and if the green comes, I get 1$. So the 1/14 = 1/5*x0.

I think that it makes sense that m_i =D z_i. Mathematically we have the definition of the r-n derivative: z_i = q_i/p_i the definition of state price per unit probability m_i = v_i/p_i and we have obtained the risk neutral probabilities q_i=v_i/D Intuitively it makes sense that the state price per unit probability is equal to the q probability per unit probability (z) multiplied by the price of a unit of q probability, which is by definition D. It also makes sense that if we take an expectation value, because E[z]=1, we would have E[m]=D. So the average state price of a unit probability is the value of a risk free dollar return. Is this correct?

Many thanks for the detailed explanation! The risk free asset is traditionally defined slightly differently (though not massively differently!) as the asset that pays the same amount in all future states. The return on this asset (with payoff of 1, and current price) is then the risk free return.

mi/D=vi/(pi*D)=(vi/D)/pi=qi/pi=Zi, So we can get mi=D*Zi these videos are amazing thank you very much. While I get confused about that risk free security idea in Casino example, if I bid 31/30 money by vi weights in each category, the money I get back should times the Pay odds right? For example, the green wins, 4* 1/5 is not equal to 1. Can you please help me with that confusion?

this is probably too late for you but maybe it helps somebody else. 4:1 betting odds actually mean you get payed 5$ in case you win and nothing in case you lose. So 5 * 1/5 = 1. So the price to get 1$ if green comes is 1/5$. If you add those prices for every number (0,1,2,3,4,5,6) you get 31/30$. For a payment of 31/30$ you get 1$ for sure, because 1 of your bets will hit.

![Gunna - HIM ALL ALONG [Official Visualizer]](http://i.ytimg.com/vi/HiCxoDeo0hc/mqdefault.jpg)

SIr, your ability to explain such concepts, in such a beautifully intuitive manner, to a rather slow retired Banker (e.g. 3 year old child) is something to behold! Thank you (my happy hour today will be a little happier).

Very nice, best intuitive explanation of a quintessential math finance topic..

Thanks Brian!!

This channel is god sent.

Thank you! Glad you found to useful!

This channel is like a hidden gem. xD

Thanks for the kind words!!

ok... just for the record. You are amaizing explaining things!!! Thanks!

Thank you very much, you deserve more views!!!

stunning explanation

Many thanks!!

Fantastic !!! Keep posting more videos

thank you!! Very kind of you!

Thank you for your explanation, it is very intuitive to understand the logic. Can I ask one question? At time 20:32, what is the meaning of x0, x1, ... here? Is my following understanding correct? For example, if I bet 1$ on the green, if I win, I will get 4$. But right now I can get extra some money, so I may get 4$ plus say 10$ = 14$. Now I standardize the price, it will be 1/14, which means I pay 1/14$ on green and if the green comes, I get 1$. So the 1/14 = 1/5*x0.

Wow this channel is Just Fantastic

many many thanks!!

What's your accademic background ? This video-lessons are just brillant .

I think that it makes sense that m_i =D z_i. Mathematically we have

the definition of the r-n derivative: z_i = q_i/p_i

the definition of state price per unit probability m_i = v_i/p_i

and we have obtained the risk neutral probabilities q_i=v_i/D

Intuitively it makes sense that the state price per unit probability is equal to the q probability per unit probability (z) multiplied by the price of a unit of q probability, which is by definition D.

It also makes sense that if we take an expectation value, because E[z]=1, we would have E[m]=D. So the average state price of a unit probability is the value of a risk free dollar return.

Is this correct?

Many thanks for the detailed explanation! The risk free asset is traditionally defined slightly differently (though not massively differently!) as the asset that pays the same amount in all future states. The return on this asset (with payoff of 1, and current price) is then the risk free return.

Thanks! how do you make the animations?

soz a bit basic, but improving over time! We don't use any fancy softwares, just plain animation, you shall see when we go backstage at some point!

Awesome

Thank you ❤️

Many thanks!!

Amazing.

Thank you!!

mi/D=vi/(pi*D)=(vi/D)/pi=qi/pi=Zi, So we can get mi=D*Zi these videos are amazing thank you very much. While I get confused about that risk free security idea in Casino example, if I bid 31/30 money by vi weights in each category, the money I get back should times the Pay odds right? For example, the green wins, 4* 1/5 is not equal to 1. Can you please help me with that confusion?

this is probably too late for you but maybe it helps somebody else. 4:1 betting odds actually mean you get payed 5$ in case you win and nothing in case you lose. So 5 * 1/5 = 1. So the price to get 1$ if green comes is 1/5$. If you add those prices for every number (0,1,2,3,4,5,6) you get 31/30$. For a payment of 31/30$ you get 1$ for sure, because 1 of your bets will hit.

Finally I have a good excuse to get rid of my maths books which only cause confusion.

Thanks Cong!! Nah won’t throw them away, books are precious- but I know what you mean- good books are like gems, so hard to find!!

Gold piece

Thanks! Glad it was useful!