CFA Level 2 | Fixed Income: Pathwise Valuation

HTML-код

- Опубликовано: 13 сен 2024

- Visit www.noesis.edu.sg for more info on CFA prep courses in Malaysia, Singapore, or wherever you are.

☕ Like the content? Support this channel by buying me a coffee at www.buymeacoff...

CFA Level 2

Topic: Fixed Income

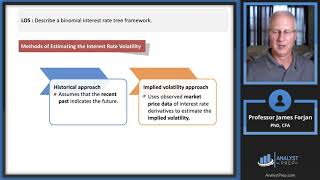

Reading: The Arbitrage-Free Valuation Framework

When given the interest rate path, draw the timeline and plot the cash flows and the 1-period interest rates. Then discount each cash flow individually to get the present value. The Texas BA II Plus's STO and RCL functions provide an easy way of computing the value of the bond using the pathwise valuation.

sir good to hear from you after a longg time. pls upload cfa content more often

hi, is there a practical application for this method or is this just a mathematical exercise? I can't think of practical application of this method in terms of bond investments and trading...

More for valuation purposed or simulation/scenario analysis

@@FabianMoa hi, why not just use spot rates and discount the 1yr cashflow using 1 yr spot rate, 2 yr cashflow using 2 yr spot rate and so on...they're basically the same with the method above and they are readily available instead of using implied forward rates which are derived from spot rates? Is there a problem like this that will be encountered in the real world where the forward rates are given instead of spot rates?

I would like to ask number of path for n year is (2^(n -1)) eg. 3 yr is 2^2 =4 path correct ?

Yes

for year 2, it should be $5/sq.(1.052) ?

5.2% is a 1 period fwd rate in one year. It's not the 2-year spot rate